Recession + Deflation = Real Panic

by: Calafia Beach Pundit

Summary

- We're in the midst of a global pandemic that, apart from a handful of countries is spreading geometrically.

- The contagion curve is already beginning to flatten in Italy and Spain, and it can't be long before the U.S. also sees a slowing in the growth of new cases.

- The Treasury has plenty of room to sell loads of bonds and at a very low cost.

- The contagion curve is already beginning to flatten in Italy and Spain, and it can't be long before the U.S. also sees a slowing in the growth of new cases.

- The Treasury has plenty of room to sell loads of bonds and at a very low cost.

What's worse: a steep recession or falling prices? Answer: A steep recession AND falling prices.

That's is the underlying reality that is shaking markets to the core right now. There are three factors that are creating those conditions: the coronavirus, government-ordered shutdowns, and a war between Saudi Arabia and Russia over oil production, and they are all inter-connected.

We have to be getting very close to a resolution of this conflict because the level of panic is rapidly approaching an intolerable extreme.

The news could hardly be worse. We're in the midst of a global pandemic that, apart from a handful of countries (China, S. Korea, Singapore) is spreading geometrically. Governments everywhere are ordering quarantines and outright shutdowns of activity. Global travel has collapsed, potentially bankrupting nearly every cruise ship and airline company.

The entire restaurant industry is teetering on the edge of failure, and take-out is only a band-aid solution. Vaccines and therapeutics won't arrive for many months. Millions of people are being laid off. GDPs are sure to plunge at dizzying rates.

Bottom line: fear, uncertainty, and doubt have reached epic heights. The market cap of global equity markets has plunged by over $30 trillion in just the last month. Nearly every major equity market is down between 30% and 40% year to date, and some prices are plunging and surging at double-digit daily rates.

To continue on the present course - shutdowns, price wars - until the virus is vanquished is madness. Something has to give. Saudi and Russia need to declare a truce. Politicians need to call off the shutdowns: at some point, the economic damage caused by shutdowns will greatly exceed the possible damage from the virus, which is already losing intensity thanks to shutdowns, hand-washing, and social distancing.

The contagion curve is already beginning to flatten in Italy and Spain, and it can't be long before the U.S. also sees a slowing in the growth of new cases.

Yes, 8,000 people have died around the world as a result of the coronavirus in the past three months, but more than 20,000 people in the U.S. died last year of run-of-the-mill flu and no one sounded any alarm. Let's keep things in perspective, please.

When conditions become intolerable, as they are today, something's gotta break. And it will, soon.

Here's a look at the key variables impacting the markets today:

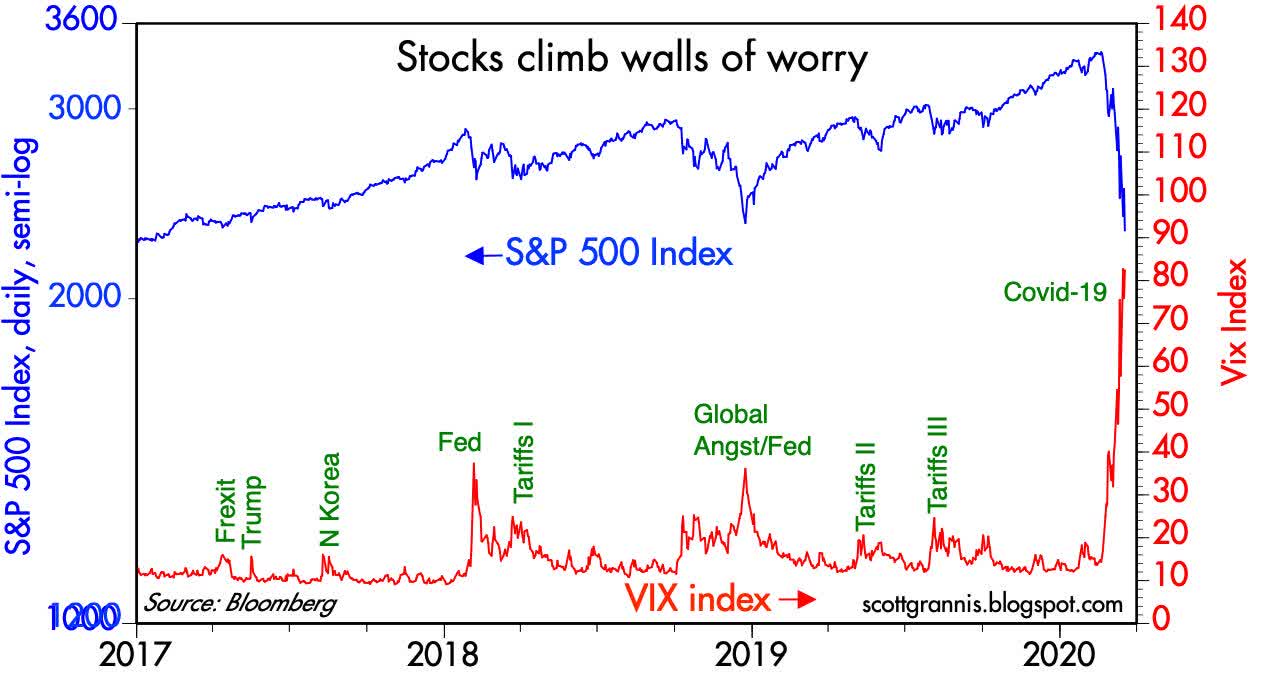

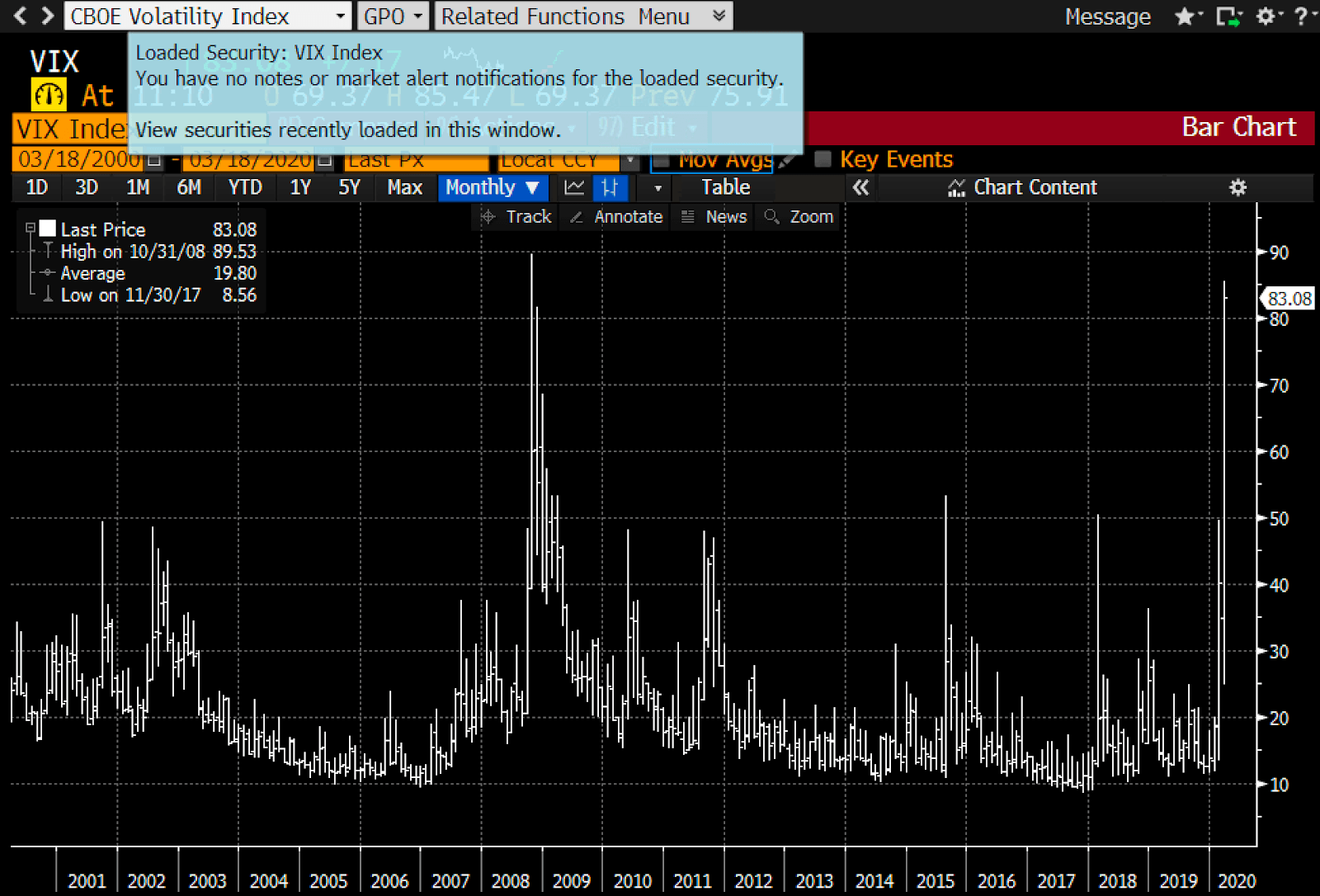

Chart #1

Chart #2

As Charts #1 and #2 show, fear has reached the same extreme as we saw at the height of the 2008 financial panic. Equity prices are down over 30%. It's a rout; everyone's headed for the exit.

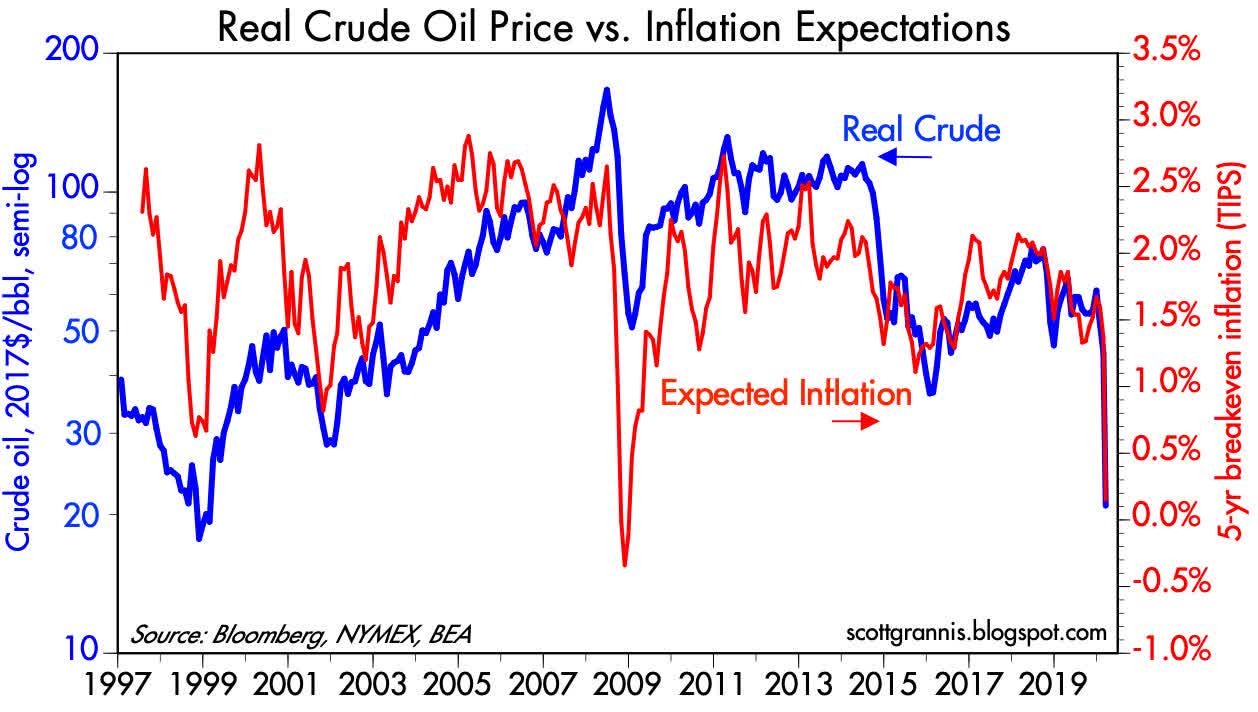

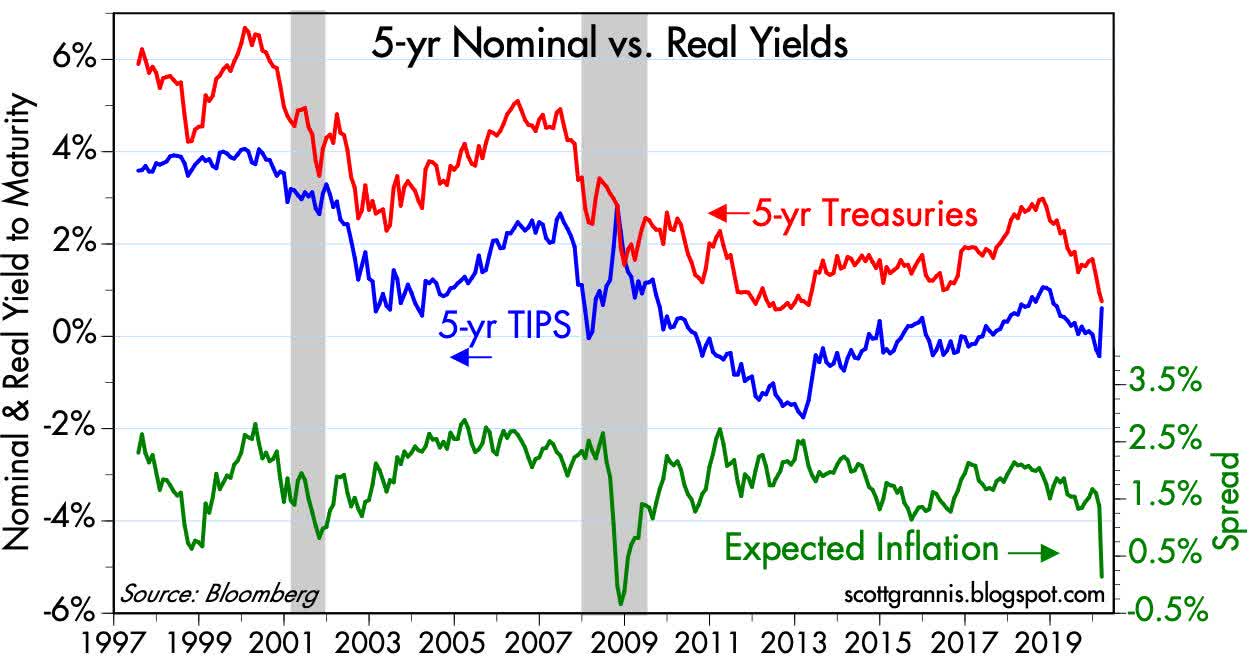

Chart #3

Chart #4

As Charts #3 and #4 show, plunging oil prices have caused inflation expectations to collapse.

We are very close to the deflationary expectations that existed at the height of the 2008 panic.

We are living in extreme times. No amount of QE will fix the virus threat, but QE will help the market cope with dislocations caused by extreme panic. The Fed needs to accommodate the market's need for safety and liquidity.

Inflation is NOT a problem.

Fiscal stimulus fueled by new Treasury issuance is NOT a problem and will directly help the consumer and small businesses to survive the (largely unnecessary in my opinion) government-mandated shutdowns.

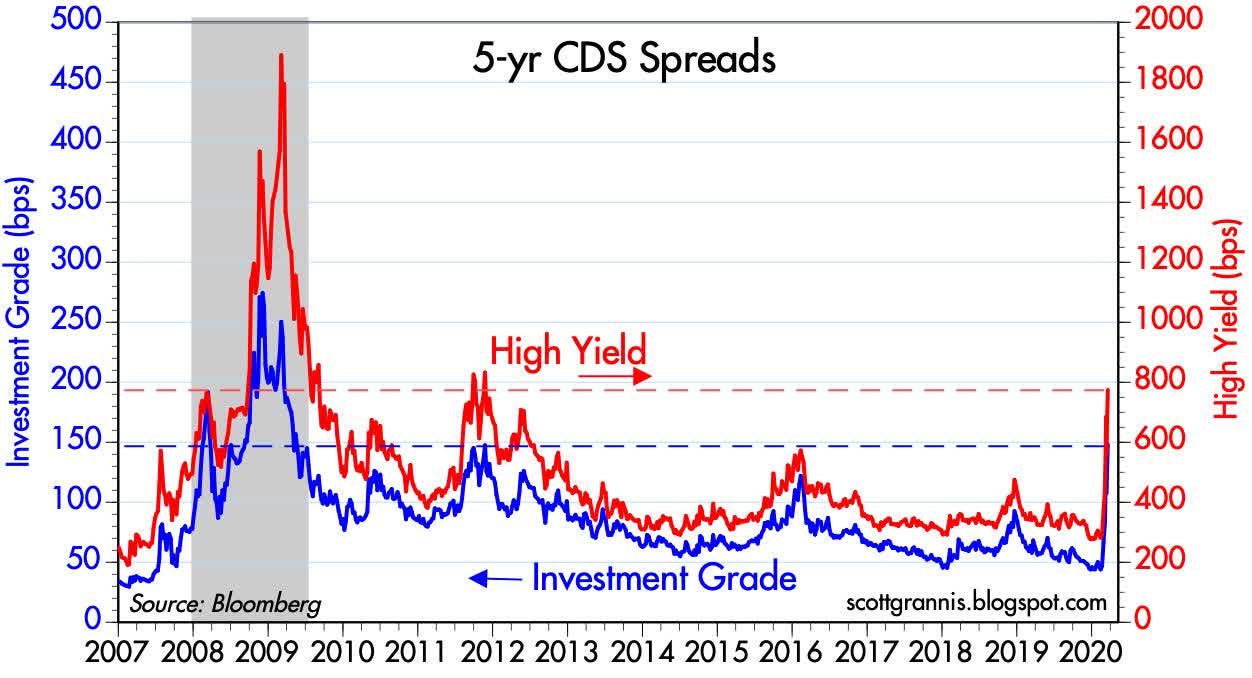

Chart #5

Recession is now likely, and credit spreads agree, as shown in Chart #5.

Chart #6

As Chart #6 shows, it's plunging oil prices that are at the root of the credit market's concerns.

High yield energy-related bond spreads (shown here as of yesterday) are most likely now at record-breaking levels, higher even than we saw at the height of the 2008 panic.

Oil prices MUST stop falling; Saudi and Russia MUST call a truce. Both need to cut production dramatically, and SOON.

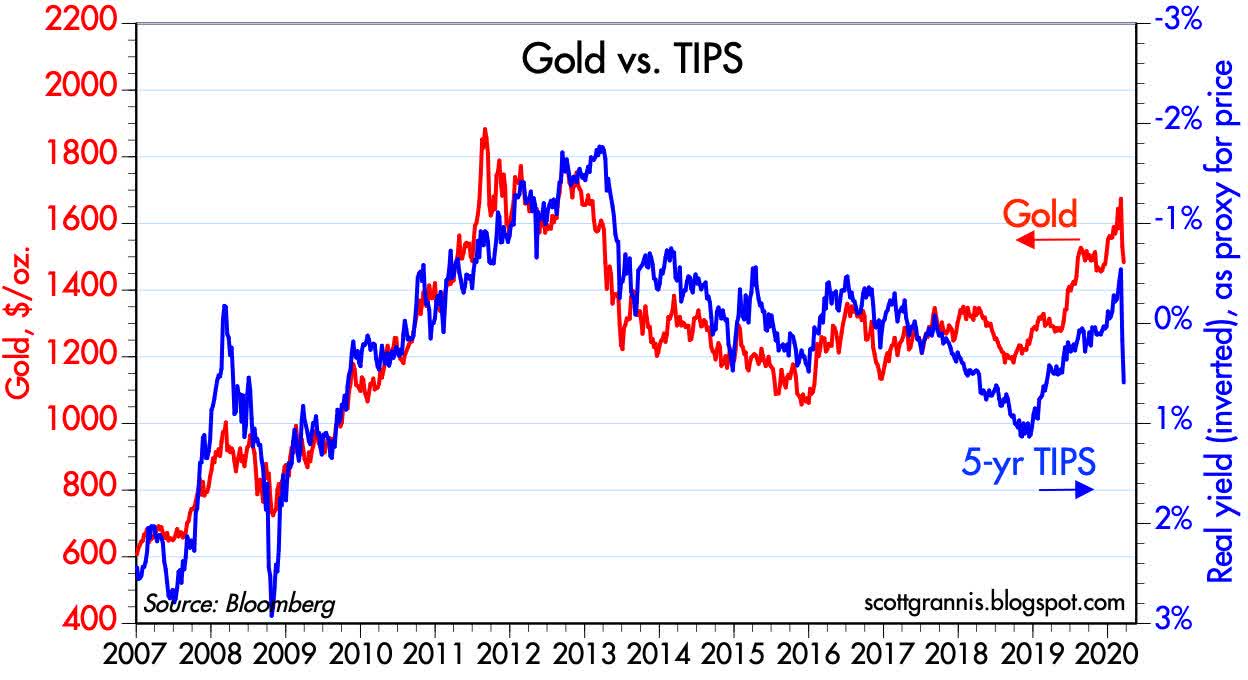

Chart #7

As Chart #7 shows, the prices of gold and TIPS are plunging. That's odd because both are safe-haven assets. The explanation for their decline can be found in mounting deflation fears: who needs inflation protection if prices are falling?

On the bright side, however, rising real yields on TIPS suggest that the market is beginning to look to the future and beginning to expect that fiscal and monetary stimulus - combined with a cessation of the oil price wars - will lead to a much stronger economy tomorrow.

There IS light at the end of this dismal tunnel!

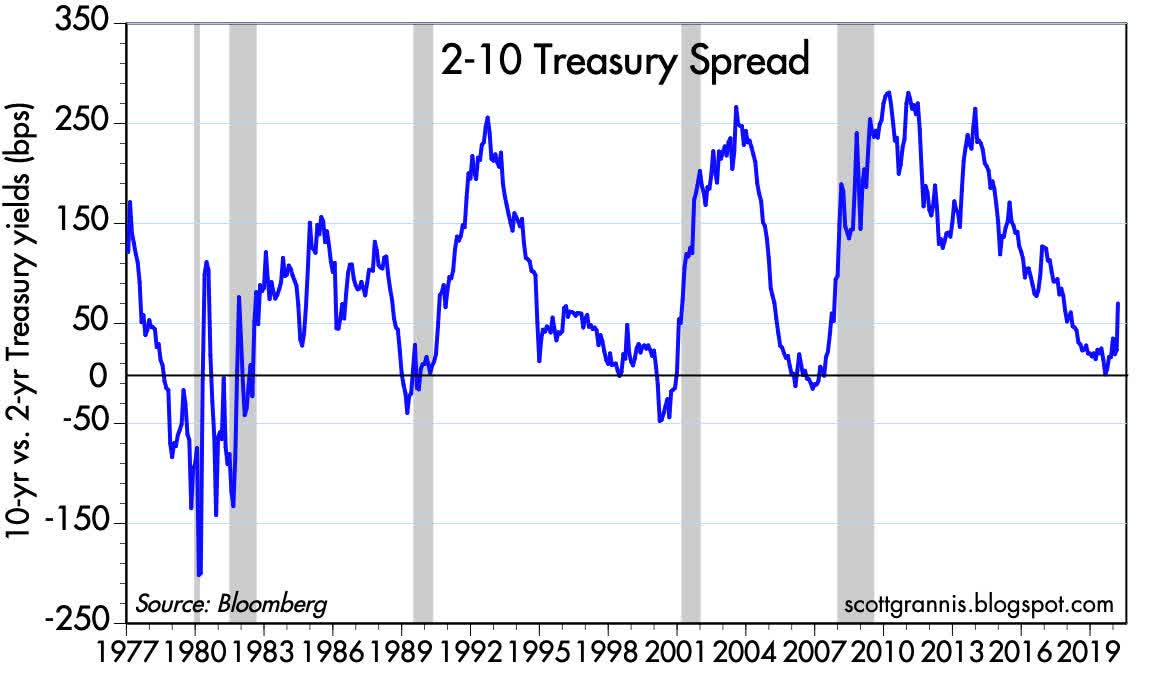

Chart #8

A marked steepening of the Treasury yield curve is also good news. The curve is steepening not because the Fed is easing, but because the market sees better times ahead.

And anyway, 10-yr yields are ONLY 1.25%, hardly a level to worry about. The Treasury has plenty of room to sell loads of bonds and at a very low cost. And they should.

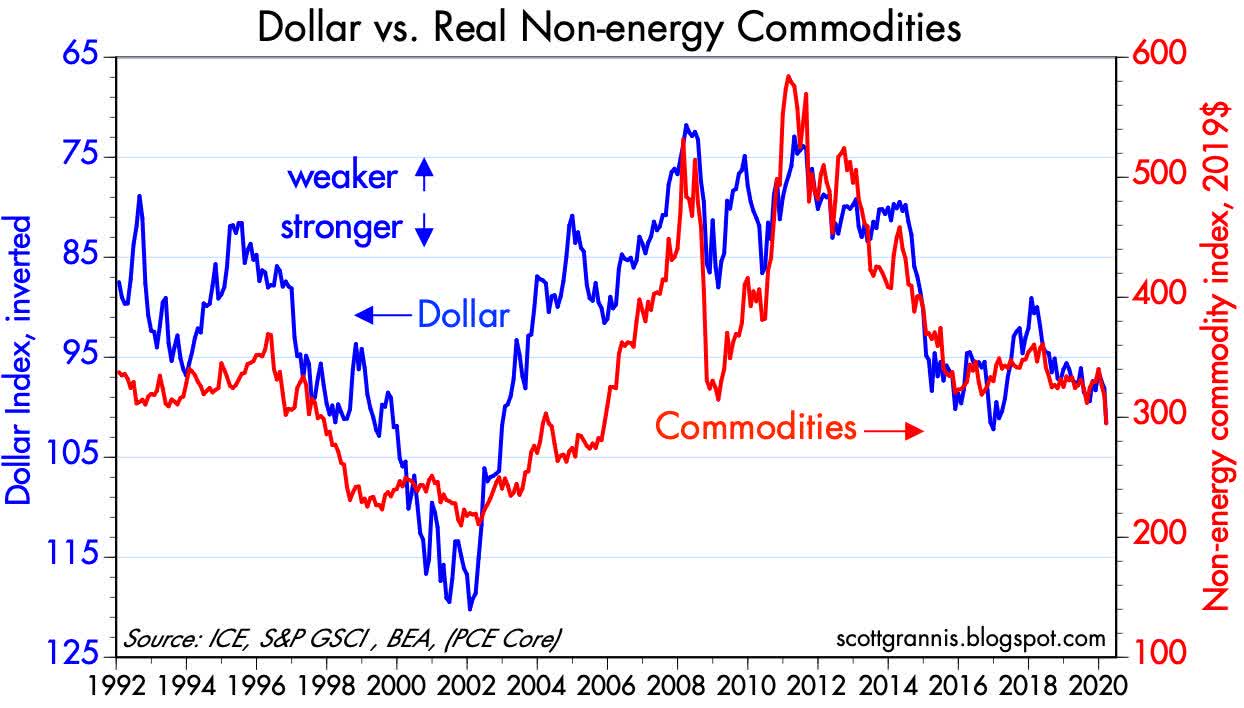

Chart #9

Chart #9 shows one other problem that is plaguing markets today: a strong dollar (blue line). A strong dollar is the result of global panic, and it is also one source of deflationary pressure on all commodity prices. More QE, please, because the world wants and needs more dollars.

0 comments:

Publicar un comentario