by: Hebba Investments

Summary

- The Fed rate cut is only the beginning for the easing necessary to counter the coronavirus downturn.

- The U.S. fiscal situation is worsening significantly and the expectation of more deficit spending will only make that worse for the U.S. dollar.

- GDX is trading at a 7% discount to NAV, making for an excellent entry point.

- Gold and gold equities have been hammered over the past week and now present a significant buying opportunity.

- The U.S. fiscal situation is worsening significantly and the expectation of more deficit spending will only make that worse for the U.S. dollar.

- GDX is trading at a 7% discount to NAV, making for an excellent entry point.

- Gold and gold equities have been hammered over the past week and now present a significant buying opportunity.

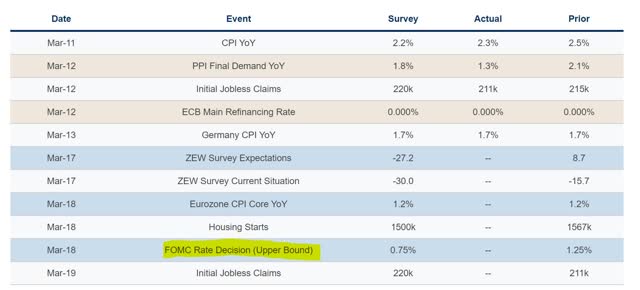

Gold investors need to be prepared for this upcoming week as it has the potential to change gold market sentiment significantly.

Source: US Global Investors

While we were writing this article, the Federal Reserve made an emergency rate cut and introduced QE5 to try and add liquidity to markets.

While we expected the rate cut, the QE was a surprise and despite that move markets are down significantly.

Despite all of this it is important that investors don’t miss the forest for the trees.

Despite the recent plunge in gold (and all assets) these events are actually extremely bullish.

One Chart to Rule Them All

With the fall in gold we wanted to share one chart from a presentation we did earlier in the week - one that pretty sums up the case for gold.

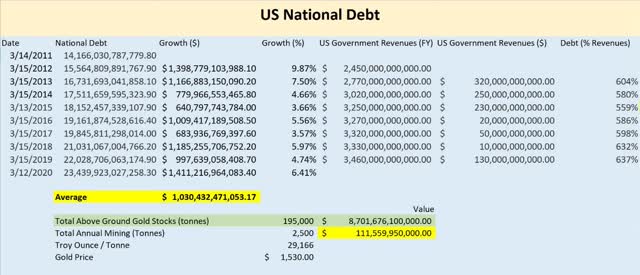

Source: Hebba Investments, Congressional Budget Office

We have discussed this before, but with the expectations of even more Fed easing and increased federal spending to provide the economy additional stimulus, investors need to remember the current budget situation of the world’s reserve currency – and the primary competitor to gold.

In the table above, we have gathered the latest reported US debt numbers (we have not included the more than $100 trillion of unfunded liabilities) and examined the growth rate in the reported debt numbers since 2011.

As is apparent, the US has been growing its debt by an average of $1.03 trillion per year at an average of 5.8% per year with the US experiencing the largest growth in debt during the last annual period of more than $1.4 trillion.

While economists will say that our debt-to-GDP ratio is not the worst, we hate comparing debt with GDP because GDP is such a political number that it is subject to much manipulation.

Secondly, it is a very vague and inexact science to calculate GDP – nobody can calculate the amount of total production of an economy and that makes it a poor measuring stick for comparison.

In fact, the most logical measure of a country’s debt burden is the ratio of its debt to its government’s revenues – that’s exactly what we do with individuals pursuing mortgages.

In this case, we see that the US government’s revenues have been rising from $2.4 million to $3.4 trillion since 2012 – a total of around $1 trillion over the past eight years or a little under $150 billion per year. While it is of course good that it is rising, it’s completely dwarfed by the growth in the debt by over $800 billion per year.

Scarier still is that the growth in debt is accelerating and moving faster on both a percentage and nominal basis compared with the growth in the government revenues – and this despite record low interest rates.

Finally, as we mentioned earlier, not only is the Fed expected to cut rates this week, but the market is expecting the government to pass a massive stimulus package to counter the huge economic impact of the coronavirus.

The US deficits aren’t going to decrease – they are going to grow. We would not be surprised if we start seeing a $2 trillion deficit for 2020.

The Role of Gold

The last part of that table details the amount of total above-ground gold stocks and its valuation.

According to the World Gold Council, there are just under 200,000 tonnes of gold held across the globe (in public and private hands), and at a $1,530-per-ounce gold price that equates around $8.7 trillion worth of gold. While that number is big, it's nowhere near the amount of debt held by the US government (gold’s primary competitor as a reserve currency) and that debt is growing 10 times faster than the amount of gold being mined every year.

So on the one hand we have a currency backed by a government growing its debt at a much faster rate than its revenues, and the expectation is that that will be sped up as the government spends its way out of a crisis. On the other hand we have gold, which is going through a period in which discoveries and future production are expected to drop.

Which one would you rather own over the long term?

Conclusion for Investors

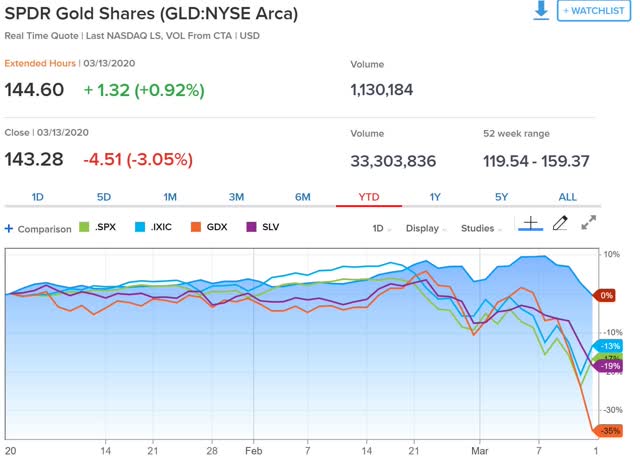

Despite the beating that gold took last week, using the SPDR Gold Shares (NYSEARCA:GLD) proxy it is actually still outperforming the S&P 500 (SPX) (-18%) and the NASDAQ (IXIC) (-13%). Gold is essentially unchanged on the year.

We wouldn’t be surprised to see some more downside as we are still going through a deflationary period until governments start to inflate stimulate the economy to counter the effects of the coronavirus. But this initial downside isn’t new to gold, and gold investors who made it through the 2007 crisis will recall that gold fell from its peak of around $1000 all the way to the $700 price level before the Fed announced QE1 – a 30% peak-to-trough drop.

With the bloodbath that has happened across markets (especially gold miners), now is the time for investors really to start allocating a good percentage of their portfolio to gold. Keep in mind the government playbook will be to combat any economic downturn with massive stimulus.

Our preferred conservative play is GLD or Aberdeen Standard Gold ETF Trust (SGOL). For those seeking a little more bang for their buck, we really like silver here under $15/oz. Keep in mind the 100:1 silver-gold ratio.

We feel if we needed a sleeper investment that we wouldn’t touch for a year it would be silver.

We recommend iShares Silver Trust (SLV) and Sprott Physical Gold and Silver Trust (CEF) for making the silver trade.

Finally, those investors with real kahunas may want to consider the gold miners. They have been absolutely hammered and many have thrown in the towel, yet some of the premier gold-mining ETFs like VanEck Vectors Gold Miners ETF (GDX) and VanEck Vectors Junior Gold Miners ETF (GDXJ) are trading at NAV discounts of more than 7% for GDX as twitter user Teddy Vallee (@TeddyVallee) points out.

The despair is there, but we think the worst is most likely behind us for the gold-mining ETFs, and investors need to remember that these ETFs are not very big.

GDX comes in around $11.67 billion and GDXJ at $4.42 billion – a few billion dollars can move these ETFs significantly as we’ve seen in the past week (up or down).

Opportunity knocks and gold investors should make sure they take advantage of some of the opportunities that this market is presenting to them.

0 comments:

Publicar un comentario