The Relentless Road To Recession Continued

by: David Haggith

Summary

- While the stock market has continued to rise, earnings have gone down quarter after quarter,

- Earnings would be much further down if not boosted by tax cuts, and earnings per share would be down even more if not boosted by massive share buybacks.

- What's driving stocks up besides buybacks?

Consider this a travelogue in pictures (graphs and charts really) that presents a rather striking and comprehensive image of a nation journeying into recession. Our decline is steeper now than it was even in my retelling of economic turns during the summer and early fall.

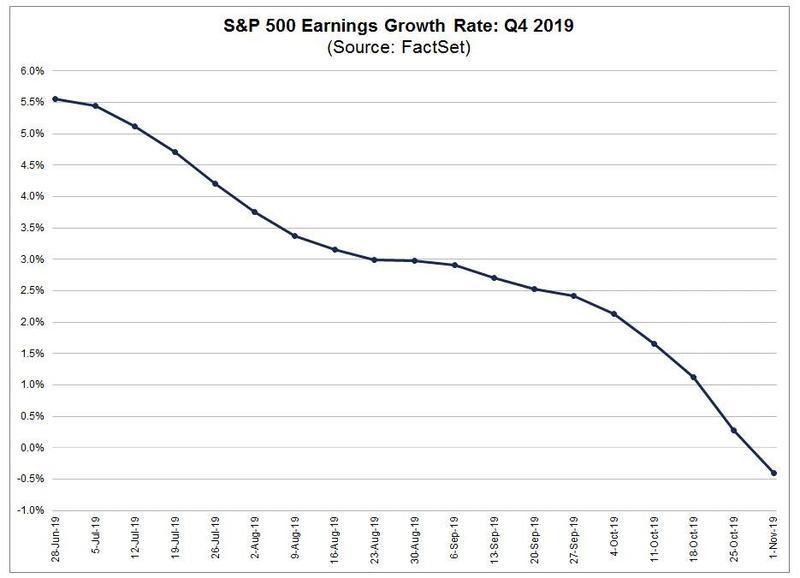

While the stock market has continued to rise (and I never said it wouldn't rise this year until and unless recession begins and takes it down), earnings - upon which stock valuations used to be based in times long ago - have gone down quarter after quarter - both actual earnings and projected.

Earnings would be much further down if not boosted by tax cuts, and earnings per share (down on average 2.3% YoY) would be down even more if not boosted by massive share buybacks because business revenue is generally down (lowest since the Obama years).

Sales are generally down. Fourth-quarter revenue and earnings are projected to be lower still on a broader basis that includes services.

These downshifts in revenue are likely to result in further cost-cutting in order to keep earnings from sinking as much, and those cost-cutting measures could include labor, thus slowing consumer capacity, which has been the only thing left holding the economy's head above water.

What's driving stocks up besides buybacks?

Could it be the new QE where a quarter of a trillion dollars is working its way back up through markets?

If so, the market may be getting a little ahead of itself:

It looks like the market has priced in a lot more QE4 than the Fed has promised. In fact, it looks like it has already priced in QE4ever. While I believe QE4ever is the course we are now on, the market might be a bit premature to price it all in at once.

While the Fed's QE may push stocks up more, we've seen years of proof that almost none of it trickles down to consumer capacity, so QE will not do much to boost the general economy as it sinks into recession due to consumers pulling back, which you'll see below consumers now appear to be doing.

If the market goes up due to the Fed's new QE4ever, it will be all the more out of sync with the underlying economy, which is likely to continue going down, in spite of the Fed's QE, since Main Street and Joe and Joline Average are not QE participants.

This, however, is not an article about what will happen to the stock market this year. I merely have to take the incongruity of its rise in a failing economy into consideration.

Whether we are now in a melt-up toward a blow-off top in stocks or not remains to be seen, but what doesn't remain to be seen is whether or not the US economy (and global economy) is still moving relentlessly into recession at an even faster clip.

Yes, it does remain to be seen whether or not the economy has already entered recession as I said it would by this time this year, but what doesn't remain to be seen is whether or not all economic movements have continued to devolve toward recession.

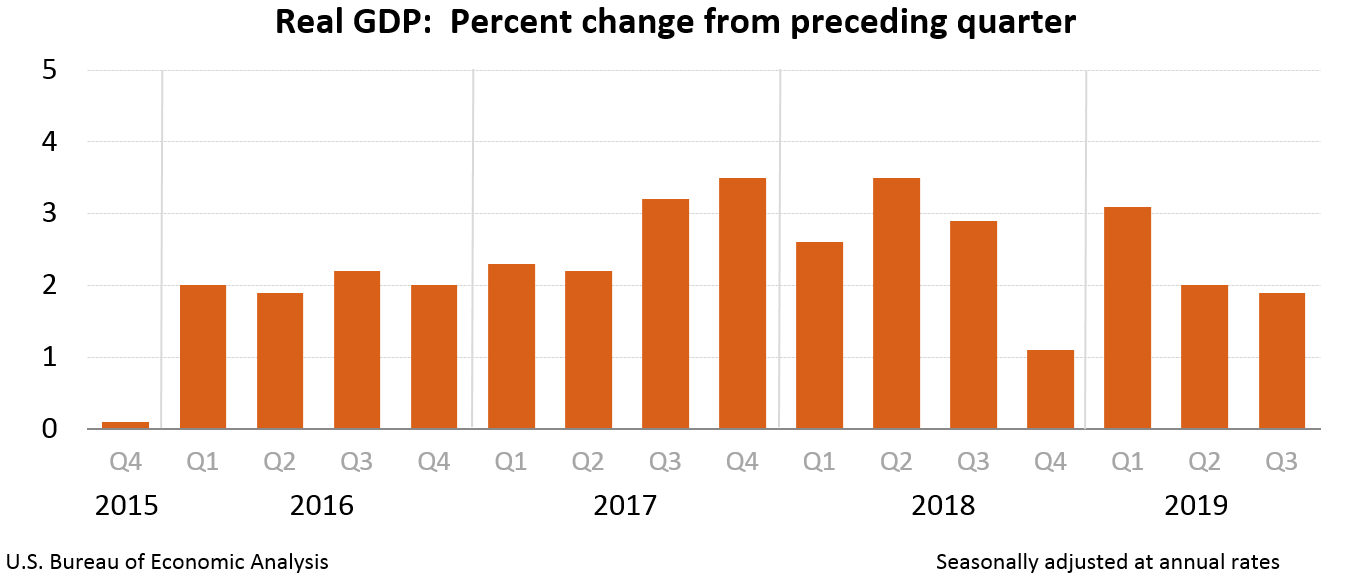

GDP ain't what it used to be

Admittedly, I thought GDP growth would be close to flat in the third quarter and would go negative in the fourth, but the third-quarter turned out better than I thought it would at 1.9% and appears to be contrary to my recession prediction:

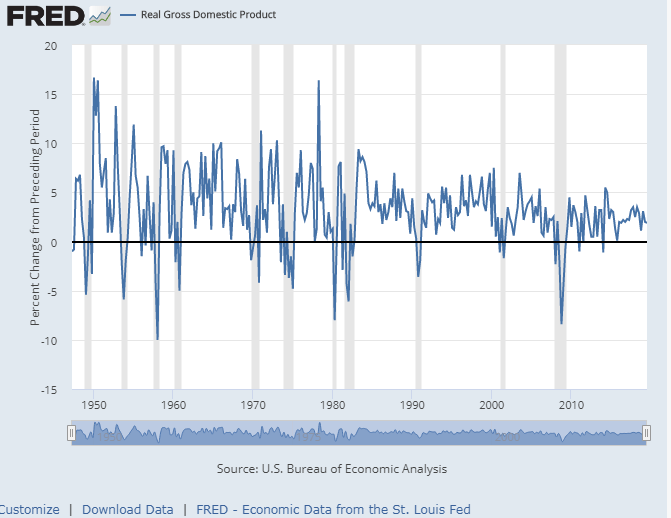

As you can see below, however, real GDP growth, which factors in inflation, often plunged from higher levels than today's GDP growth number straight into recession in a single quarter:

It would not be at all unusual for it to do so now.

In fact, we saw GDP growth drop by much more than that in the quarter going into each of the last two recessions.

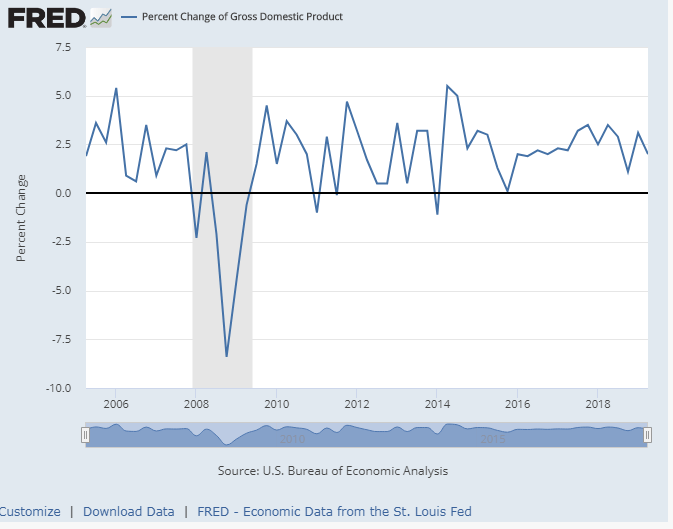

Notice how, going into the Great Recession, GDP growth dropped in the starting quarter of that recession from a positive 2.5% to negative 2.3%:

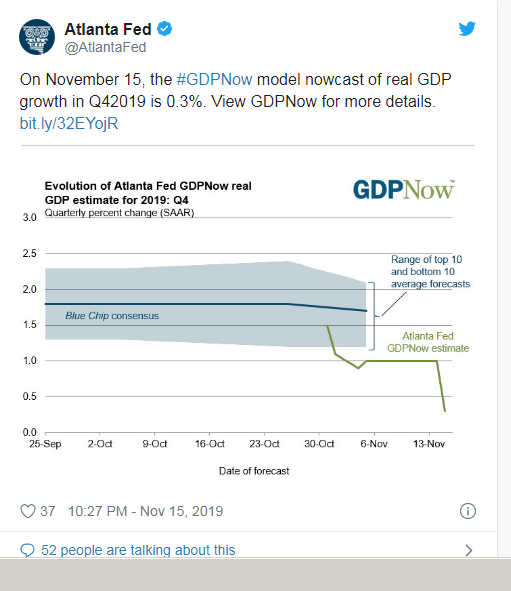

It appears GDP may be making such a large quarterly drop again. Already, fourth-quarter GDP growth has been revised down to a projected 0.3% by the Atlanta Fed and 0.39% by the New York Fed, and I should note that the Atlanta Fed's number was 1.0% only two weeks ago. So, the revisions are coming in fast and furious.

The green line in the graph below shows how quickly the Atlanta Fed has been revising its estimate of the fourth quarter downward:

So, maybe, just maybe, the stock market is a little disjoined from the kinds of business metrics that for decades drove the valuation of stocks and particularly from the general economy.

Regardless of what is happening in the Wonderland of stocks, recession in the real economy is rolling downhill quickly. The following is a round-up of economic statistics since the last time I reported on the recession's progress:

Moreover, the official determination of the start of a recession is not always based just on GDP and can sometimes peg the start of a recession a month or two earlier than the first quarter that goes negative:

A recession is when the economy declines significantly for at least six months.

There's a drop in the following five economic indicators: real gross domestic product, income, employment, manufacturing, and retail sales. People often say a recession is when the GDP growth rate is negative for two consecutive quarters or more. But a recession can quietly begin before the quarterly gross domestic product reports are out.

That's why the National Bureau of Economic Research measures the other four factors. That data comes out monthly. When these economic indicators decline, so will GDP. The National Bureau of Economic Research defines a recession as "a period of falling economic activity spread across the economy, lasting more than a few months."

The NBER is the private non-profit that announces when recessions start and stop. It is the national source for measuring the stages of the business cycle. - The Balance

To the extent GDP did grow last quarter, most growth was considered to be largely driven by continued strong consumer spending.

In fact, growth in consumer spending was equal to 100% of the overall growth seen in GDP.

The only other positive contribution to growth was government spending. In other words, had consumer spending gone down the tiniest fraction, instead of rising, GDP growth would have been negative:

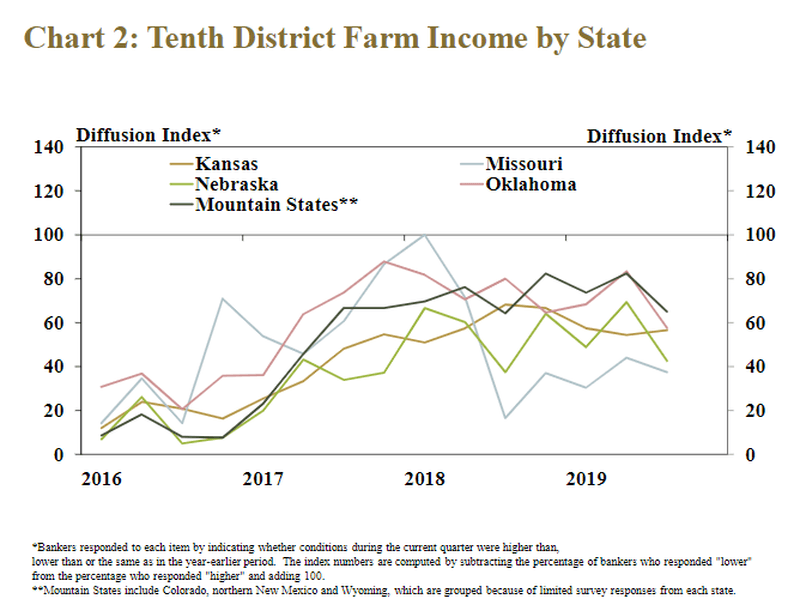

Kansas City Federal Reserve Bank

Kansas City Federal Reserve Bank

The upper midwest, however, has been hit severely. Wisconsin reports that it is losing two dairy farms every day! That is a lot of loss for one state.

As farm bankruptcies soar, it is possible that nearly 10% of Wisconsin dairy farmers may go out of business in 2019. "You look at the weather, you look at the crops you can't get off the field, you look at the bills you can't pay," Edelburg, told Yahoo Finance. "Bankruptcies are up … 24% from last year already." - SHTFplan

And "up 24%" is not 24% of a small number. Wisconsin lost almost 1,200 dairy farms between 2016 and 2018! People might be crowing about how nice it is in Florida, but Florida isn't the whole US, and the pain in Wisconsin is severe. Suicide rates, particularly among farmers, have soared:

The USDA farm agency trains its farm loan officers on how to look for warning signs as part of suicide prevention. "The bankers are the first and the forefront to see a lot of these things," Edelburg said. "They're delivering the bad news, and these farmers are dealing with it on that level." - SHTFplan

Calls to the Wisconsin Farm Center, which helps distressed farmers, were up last year, including a 33 percent increase in November and December compared to the same two months the previous year. - Wisconsin State Journal

Farmers have really been taking it on the lam this year because of the 1-2-3 blow of droughts, floods, and the Trump Trade Wars. Over half of US states are experiencing rising farm bankruptcies, again reaching their highest level since the end of the Great Recession.

Transportation rolling downhill

It's not surprising, when farms are going out of production and buying less equipment and manufacturing is declining, to find that shipping would also be in decline.

The whole picture is in agreement about what is happening.

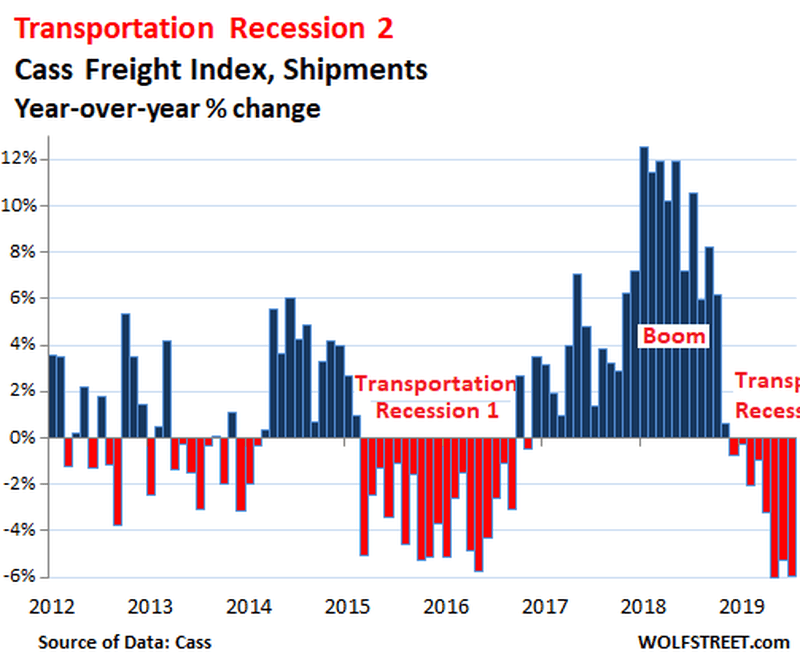

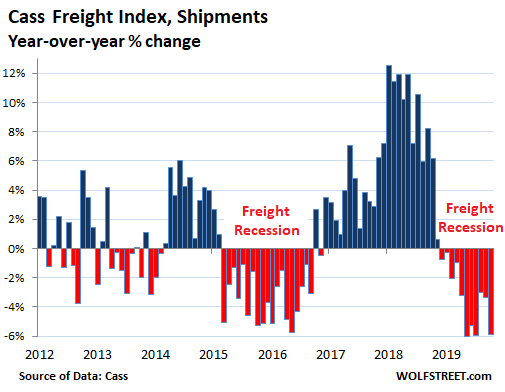

The last time I presented the Cass Freight Index, it looked like this:

Now, it looks like this:

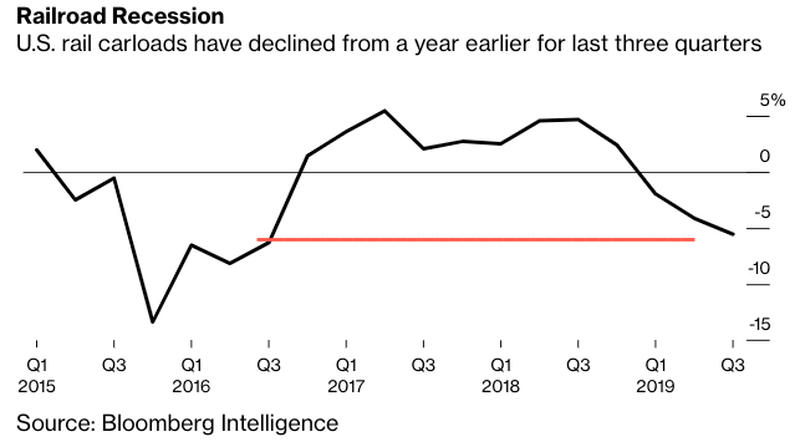

That includes what is now being called a "railroad recession."

The American Association of Railroads reported that rail traffic and intermodal container usage has gone … well, off the rails:

"There are no pockets of growth," said Bloomberg Intelligence analyst Lee Klaskow…. "There's really nothing that's tapping me on the shoulder saying, 'Hey look at me. I'm going to be your next growth engine.'" - Zero Hedge

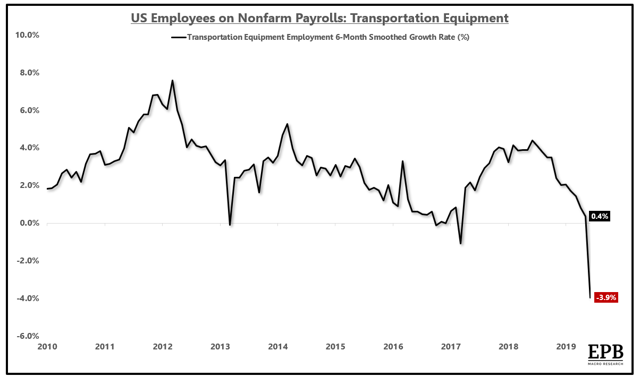

Need I say more about transportation? I'll only note that as the freight recession (so many things being called a "recession" now) goes on, so go orders of new transportation equipment, creating a feedback loop into automotive production and other manufacturing, which has taken production of all transportation equipment right over a cliff:

Seeking Alpha

Seeking AlphaHousing keeps collapsing

Home pricing has continued to slide with sales, as has competition between buyers.

According to Redfin, competition continued to fall away nationally both on a year-on-year basis and a month-on-month basis:

Nationally, just 10 percent of offers written by Redfin agents on behalf of their homebuying customers faced a bidding war in October, down from 39 percent a year earlier and now at a 10-year low. - Redfin

Some regions were up on a month-on-month basis, but all regions were way down year-on-year.

Home Depot (NYSE:HD) is a solid bellwether business for gauging the home construction and remodeling business, and it just reported its worst quarter since the Great Recession:

"Home Depot earnings the most disappointing for investors since the financial crisis"

Shares of Home Depot Inc … sank 4.9% in morning trading Tuesday, which puts them on track to suffer the biggest one-day post-earnings decline in over 10 years. Earlier, the home improvement retailer beat fiscal third-quarter profit expectations but missed on total and same-store sales, and lowered its full-year outlook. The last time the stock fell as much on the day after earnings was May 19, 2009. - MarketWatch

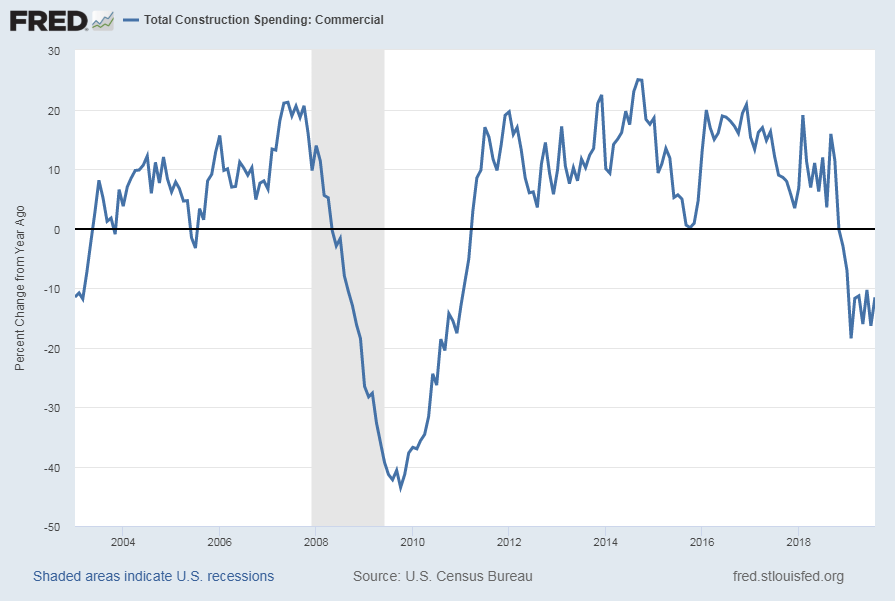

Those stated expectations don't sound like Home Depot is expecting home construction to pick up anytime soon, but the decline in construction is not limited to housing; commercial construction has been in recession for some time now:

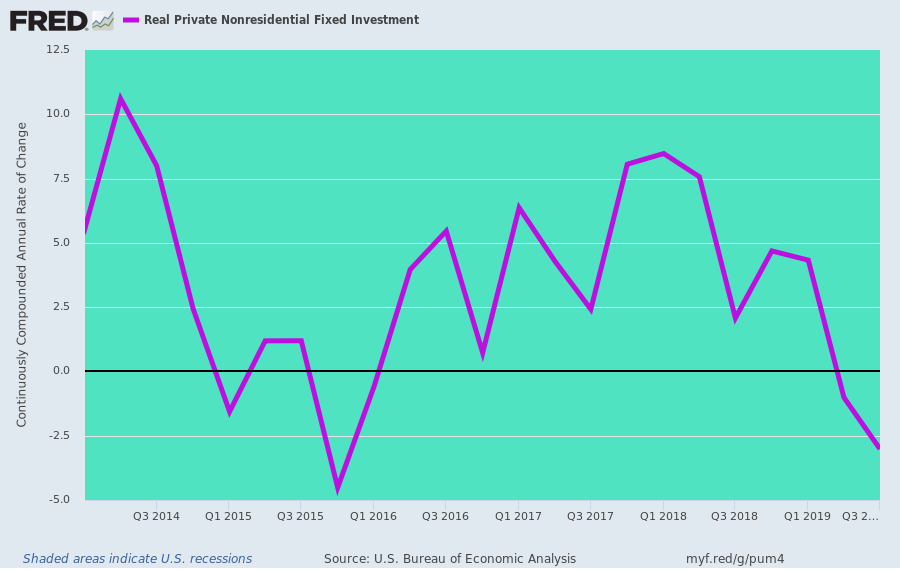

Capital investments and business sentiment no longer so capital

With manufacturing in recession, freight in recession, new orders of vehicles in recession, farms falling left and right, housing in decline and commercial construction in recession, it is no wonder that investment in fixed assets is falling off a cliff, too:

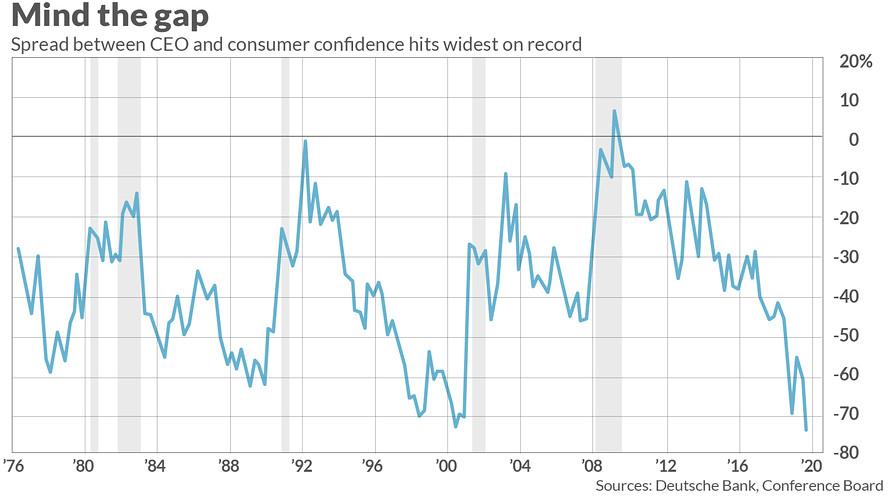

Thus, we shouldn't be surprised either to see that business sentiment tumbling down a long hill with two out of three measures hitting their lowest low since the Great Recession:

Thus, it should also not be a surprise that CEOs who are a lot closer to business sentiment than consumers feel much worse about things than consumers who have only just begun to catch on:

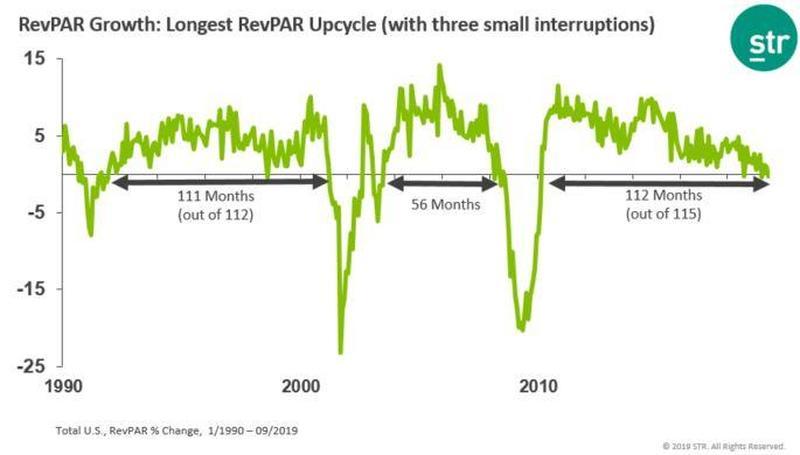

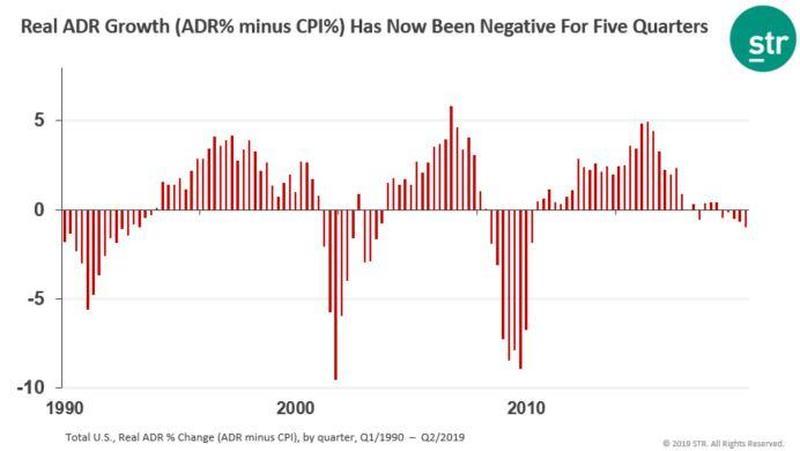

And, coming close to Donald's own heart, the US hotel industry is also entering recession … at least, as measured by revenue per available room.

Certainly travel is one area consumers cut first when they start tightening their belts.

Again the trend hasn't sunk this low since the Great Recession:

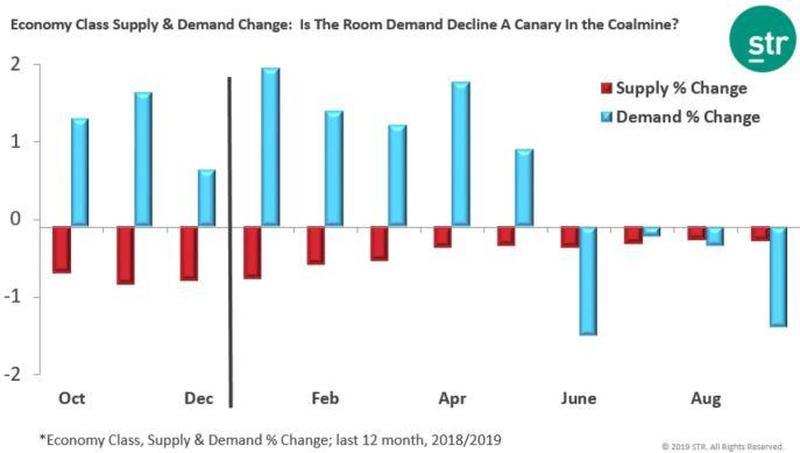

Of course, when measured "per available room," the decline could be as much due to overbuilding as due to receding travel.

However, that does not appear to be the case - at least in economy rooms - where supply has been shrinking for some time, while demand is also now shrinking:

Average daily rates (pricing) are even receding in a way not seen since the last two recessions:

Not-so-gainful employment

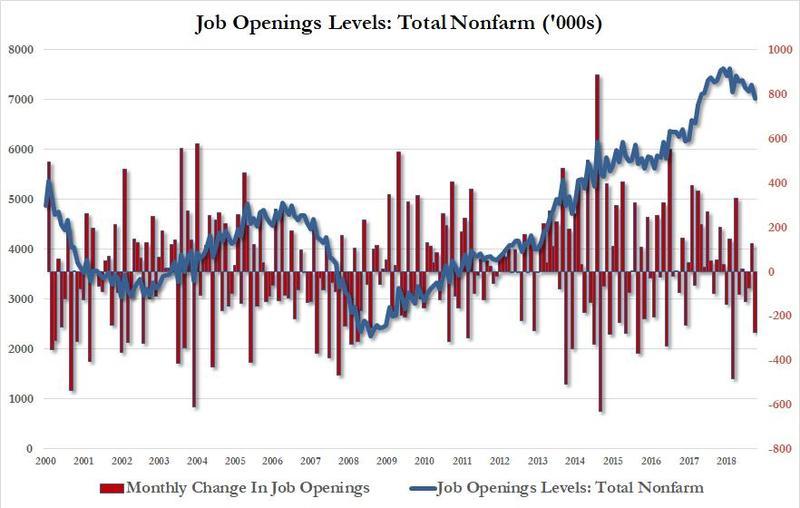

With all of that, it's not surprising that employment - the most critical factor in determining recessions - is also starting to turn south.

The latest JOLTS report released by the Bureau of Labor Statistics showed the total number of job openings is now trending even more sharply downward:

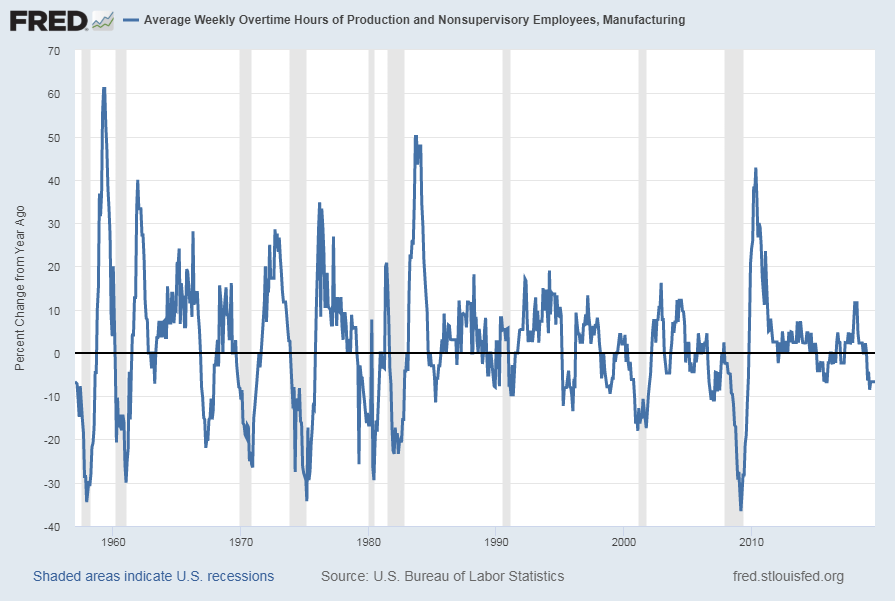

Of course, the first place companies cut back before firing employees is in overtime hours.

As would be expected from the information above about manufacturing orders and production, those hours have already been cut way back in manufacturing to a degree not seen since … the Great Recession:

While the unemployment rate has appeared in my past reports to be putting in a bottom, it hasn't turned significantly upward yet.

However, with new jobs on such a consistent decline, a significant rise in unemployment cannot be far off. The hiring rate of US companies has fallen to a seven-year low:

Just one-fifth of the economists surveyed by the National Association for Business Economics said their companies have added to their workforces in the past three months. That is down from one-third in July…. A broad measure of job gains in the survey fell to its lowest level since October 2012…. "The U.S. economy appears to be slowing, and respondents expect still slower growth over the next 12 months…." The hiring slowdown comes as more businesses are reporting slower growth of sales and profits…. Government data shows that companies are posting fewer available jobs, suggesting that demand for labor is weakening…. Companies are also cutting back on their investments in machinery, computers, and other equipment. The proportion of firms increasing their spending on such goods is at its lowest level in five years, the survey found. - AP

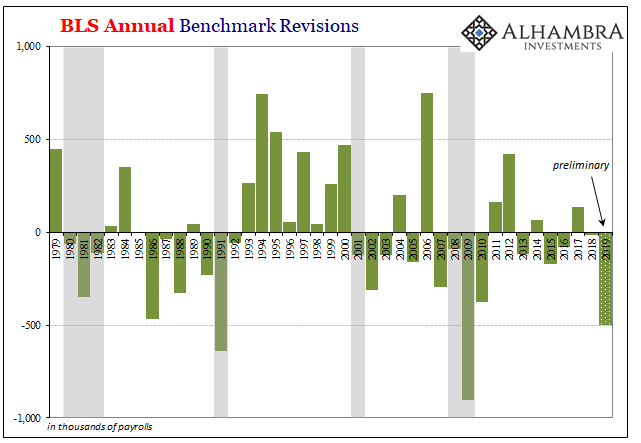

Finally, remember that, when the Bureau of Labor Statistics reconciled its books this year, it found that its monthly new jobs reports had in aggregate overstated the number of new jobs for the past year by half a million.

I've pointed out before that this scale of downward revision only happens in the middle of recessions when apparently their methods of surveying new jobs are hugely biased toward the positive:

Finance

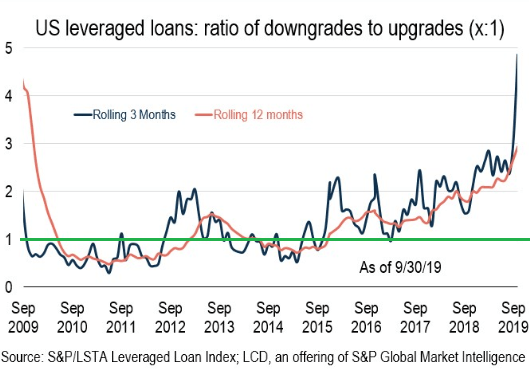

As tightness in all of these areas of the economy continues to press in, it is adversely affecting the world of finance. In 2017, 13 leveraged loans in the S&P/LSTA Index were downgraded.

In 2018, the number of downgrades shot up to 244.

In 2019, the number rose even more to 282 with two and a half months of a steepening trend still to come in.

The trend of rising downgrades has put in its hockey-stick curve now like this, and you'll see, again, you have to go all the way back to the Great Recession to find a time that looks as bad:

With that, let me leave you with something to think about from a conservative businessman, Oaktree Capital Management's Co-Chairman Howard Marks, talking about our inverted bond world, bubbles, and his belief that we're in a high-risk period:

0 comments:

Publicar un comentario