To halt money-market volatility the Fed flooded markets with cash—and it accumulated assets. But at year’s end some banks may limit lending.

By Nick Timiraos

The Federal Reserve has pumped hundreds of billions of dollars into money markets to avoid volatility. Fed Chairman Jerome Powell. Photo: ERIC BARADAT/Agence France-Presse/Getty Images

The Federal Reserve over the last three months has flooded money markets with hundreds of billions of dollars in cash to avoid a repeat of volatility that roiled cash markets in September.

The success of the moves—which reversed roughly half of the Fed’s shrinkage of its asset portfolio over the prior two years—will encounter a test around Dec. 31. That is when some financial institutions could face incentives from regulations to limit their lending, which could cause supply and demand imbalances for cash.

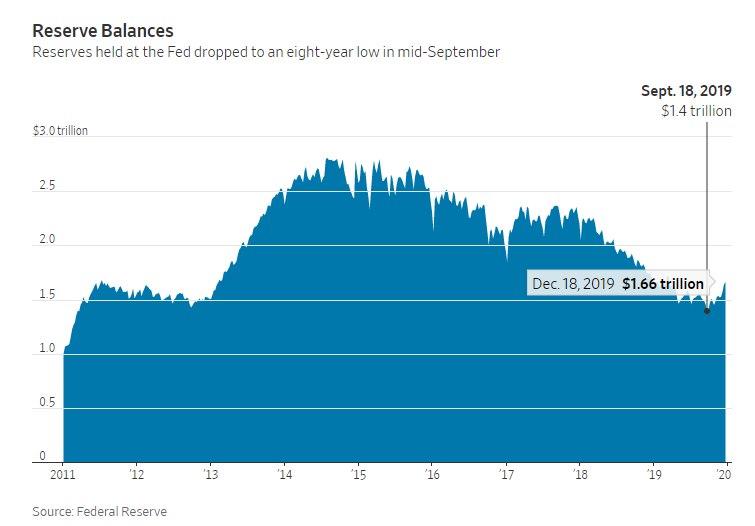

Fed officials have said they believe deposits by banks held at the Fed, called reserves, grew scarce enough in mid-September to put pressure on an obscure but important lending rate in the market for repurchase agreements, or repos. Banks and other firms use repos as a way to borrow cash for short periods, pledging government securities as collateral.

“You can flood the markets with reserves but are the reserves going to be redistributed to the corners of the markets that need it? That’s the big question,” saidWard McCarthy,chief financial economist at financial-services company Jefferies LLC.

To prevent a squeeze from happening again, Fed officials have been buying short-term Treasury bills from financial institutions to put more reserves back into the financial system.

They also have conducted daily injections of liquidity into markets.

Altogether, those operations could add nearly $500 billion in net liquidity to markets around Dec. 31.

The end of the year is an important date because large banks could limit lending activities in derivatives and repo markets to guard against extra regulatory burdens.

For these banks, their lending profile on Dec. 31 is used to determine how much equity capital they must raise against their liabilities.

In the last few years, repo rates have typically been no more than a 10th of a percentage point above or below the Fed’s benchmark rate, but on Dec. 31, 2018, they widened by 2.75 percentage points.

This spread grew again on Sept. 17 after large payments of corporate taxes and Treasury auction settlements the day before resulted in a major transfer to the government of cash held in the banking system. This flow of payments reduced reserves.

“The markets acted as though reserves had become scarce,” Fed ChairmanJerome Powellsaid at a Dec. 11 news conference.

The September episode prompted the Fed to intervene in markets to prevent reserves from declining further. The central bank announced plans to provide overnight and 14-day loans in the repo market, and by mid-October had agreed on a scheme to keep reserves from declining further by purchasing $60 billion a month in Treasury bills.

“Their response has been very effective,” said Priya Misra, head of interest-rate strategy at TD Securities.

“They were quick to acknowledge reserves dropped too low. They were very humble, and that level of humility is good to see.”

The September market stress may have also focused financial institutions that rely on repo funding to lock in financing ahead of the end of the year.

“There is some evidence that people are getting their ducks in a row,” saidSeth Carpenter, chief U.S. economist at UBS Group AG and a former official at the Fed and the Treasury Department. He said he sees a one-in-three chance of repo-market issues at year-end.

If there were going to be destabilizing money-market pressures on Dec. 31 they should be cropping up now, saidMark Cabana,head of short-term interest-rate strategy research at Bank of America. “The concerns in my own mind have cooled significantly,” he said.

The Fed added hundreds of billions of dollars in reserves to the banking system earlier this decade when it purchased Treasury and mortgage securities to stimulate the economy when short-term interest rates were near zero. It began draining these reserves in 2017 by allowing more of those assets to mature without replacing them.

It stopped doing so in July, after cutting short-term rates in response to worries about the global growth outlook.

Reserves are a liability against assets on the Fed’s balance sheet, and they can decline when the Fed holds its balance sheet steady if other liabilities rise.

This is precisely what happened in August and early September, after the Treasury Department began rebuilding its general account—maintained at the Fed—after Congress suspended the federal borrowing limit. This cash balance is one of several liabilities on the Fed’s balance sheet that had been growing, further squeezing reserves out of the system.

Fed officials are also trying to determine whether postcrisis rules meant to assure major banks have a sufficient cash cushion to weather a crisis have led banks to hoard reserves, aggravating the September market tumult.

The episode caught Fed officials by surprise in part because they didn’t think reserves had grown especially scarce.

As the Fed fine-tunes its response to money-market volatility, its officials face a broader tension. They want to avoid spikes in the repo market—such as those related to the year-end funding pressures—that could interfere with their ability to set short-term interest rates.

But they don’t necessarily see their job as to eliminate volatility entirely from short-term lending markets. One risk: Stamping out volatility during normal times could yield more volatility when shocks hit.

“You do want to create room for repo rates to vary again, and create a margin where normal market forces can play out,” saidLou Crandall,chief economist at financial-research firm Wrightson ICAP.

What the Fed is doing right now, he said, appears designed to provide a guardrail for markets as the central bank and Wall Street learn more about any unexpected side effects from changes in market structure and regulation after years in which the Fed maintained a larger asset portfolio.

“We are going to be in an era for the next couple of years in which…money markets can experience severe distortions that are just inefficient,” Mr. Crandall said.

0 comments:

Publicar un comentario