Some of the factors lifting markets in recent days aren’t quite what they seem

By Nathaniel Taplin

A worker installs steel rebars on a construction site of a highway in China. Photo: china stringer network/Reuters

Lower trade tensions: check. Global manufacturing rebound: check. No inverted yield curve: check. What could go wrong?

Actually, a fair amount. Signs of renewed vigor in the global economy are real, but some of the factors lifting markets in recent days aren’t quite what they seem. Sharp surges in commodity prices and mining stocks, in particular, may be difficult to sustain. Copper is up about 5% since early December, while shares in miner Rio Tinto have risen about 7%.

First, the good news: Key parts of the global manufacturing complex, after a terrible 2019, are doing better. Although most analysts missed it, signs of stabilization in China’s export-oriented electronics sector have been evident for months. After a brutal crash in late 2018, global semiconductor sales have begun rising again. So have global smartphone sales, according to tech advisory firm Canalys.

Chinese data—from both official and other sources—backs this up. Operating profits of listed Chinese information technology firms were up 9.7% on the year in the third quarter, the best results since early 2018. After steep declines for most of late 2018 and 2019, Chinese mobile phone production was up on the year for the third month in a row in November.

Auto production rose for the first time since June 2018. Overall profit growth at listed Chinese firms also appears to have stabilized—good news for global consumer goods, since profit growth tends to lead the labor market.

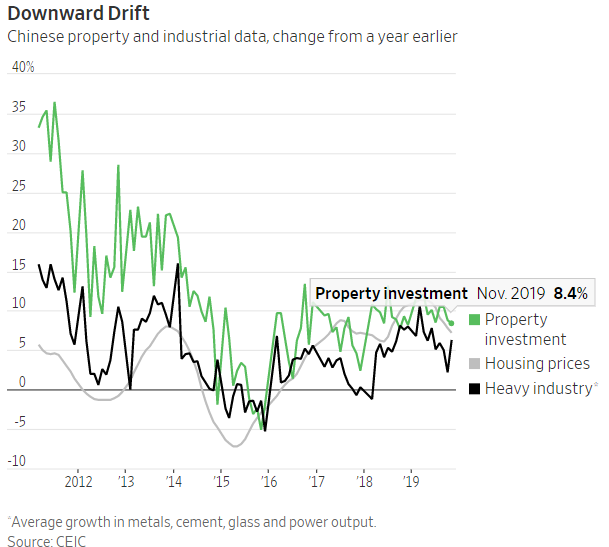

There is, however, one problem with this rosy picture. One of the things lifting Chinese industrial growth to a five-month high in November—and global markets to record levels Monday—was strong production of heavy industrial products such as steel and cement. This looks unlikely to last.

The industrial surge—year-over-year growth in steel-product output more than doubled to 10%—appears to stem from a jump in electricity and utility project investment, up sharply since September. The value of infrastructure projects approved by China’s economic planning agency jumped in the second and third quarters, but has cratered since September as fiscal constraints bite.

Strong infrastructure-driven demand for materials could last a few more months as that effect feeds through with a lag, but probably no more. China’s power sector is already heavily over-invested: Power plants in 2018 ran an average of only about 3,900 hours a year, compared with more than 4,700 hours in 2011.

China’s housing market—the most important driver of global metal demand—is also starting to look shaky again. Property investment growth slowed for the second month in a row to 8.4% on the year in November, the weakest reading since December 2018. New home prices rose half as fast in November as they did midyear.

Add plateauing Chinese credit growth to the mix and the current bounce in metal prices and mining stocks seems at risk of a reversal in the coming months.

Investors can ride the rally for now, but would be wise to take profits before too long.

0 comments:

Publicar un comentario