Record High Stocks And The Tragicomedy Of Great Expectations

by: The Heisenberg

Summary

- US stocks surged to record highs on Monday on remarks from President Trump around the nebulous "Phase One" trade deal with China.

- Meanwhile, traders are set to be bombarded with critical data in the new week.

- The Fed's message on Wednesday could either be enhanced by the numbers or totally antiquated.

- Meanwhile, traders are set to be bombarded with critical data in the new week.

- The Fed's message on Wednesday could either be enhanced by the numbers or totally antiquated.

US equities reclaimed record highs on Monday morning, following brief remarks from Donald Trump on trade. "We’re a little bit ahead of schedule, probably a lot ahead of schedule," the President said, en route to Chicago.

It was the latest in an ongoing drip of upbeat soundbites around the still nebulous "Phase One" trade agreement that the market hopes to see signed by Trump and his Chinese counterpart at APEC in Chile next month.

(Heisenberg)

(Heisenberg)

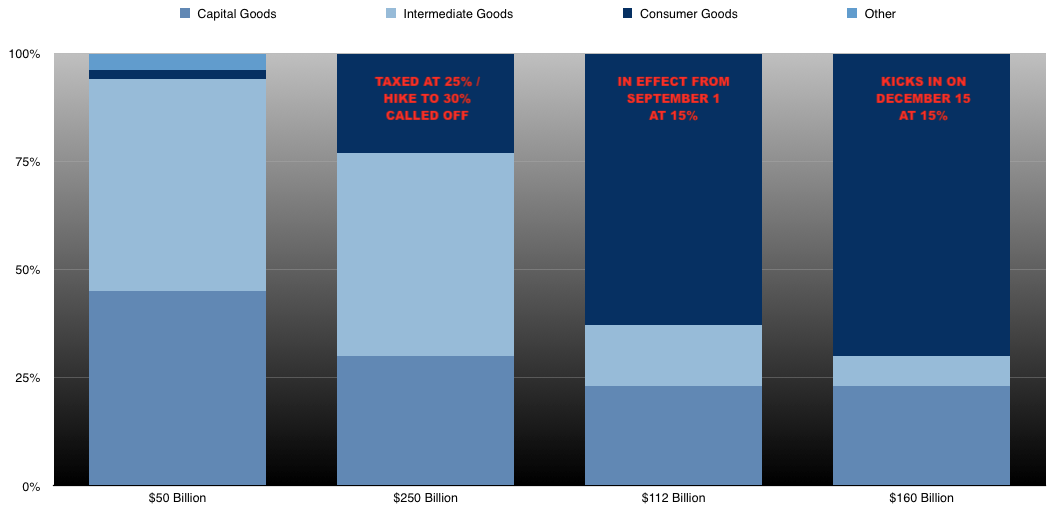

As a reminder (and this can't be emphasized enough) what markets really want to hear is that the tariff escalation set for December 15 is off the table.

There was no decision on that during principal-level trade negotiations in Washington earlier this month, and it is a source of continual consternation not only for market participants, but for Beijing.

(Heisenberg)

(Heisenberg)

I've run that chart on several occasions in these pages, but it's worth showing it again on Monday in light of the renewed trade optimism. The mix of goods targeted in the prospective December escalation skews heavily towards consumer items, which is a worry for a US economy that is leaning heavily on the consumer.

That makes for a nice segue into what will be a critical week of data. The advance read on Q3 GDP will almost surely show the US economy growing at a pace that isn't even close to the 3% "target" the administration set for itself. Most people gave up on juxtaposing the rhetoric from the President's advisors (notably Larry Kudlow) with the reality of the numbers a long time ago.

The fact is, the economy isn't going to grow at a 3% rate this year and, indeed, it didn't do so last year either (the Q4-to-Q4 number was revised lower over the summer). Ultimately, the BEA’s advance estimate of Q3 GDP will likely show growth of around 1.5% QoQ saar.

The fact is, the economy isn't going to grow at a 3% rate this year and, indeed, it didn't do so last year either (the Q4-to-Q4 number was revised lower over the summer). Ultimately, the BEA’s advance estimate of Q3 GDP will likely show growth of around 1.5% QoQ saar.

That would be the slowest pace this year, and it comes hot on the heels of Treasury's admission that the US budget deficit exploded 26% higher in FY2019 to $984 billion.

The cold, hard reality of this situation is that the tax cuts aren't paying for themselves and the economy, while still doing reasonably well, isn't performing anywhere near levels promised by the likes of Kudlow on too many occasions to count. Those are the facts and this outcome was entirely predictable. Trump's tax cuts have run into a classic Ricardian equivalence problem.

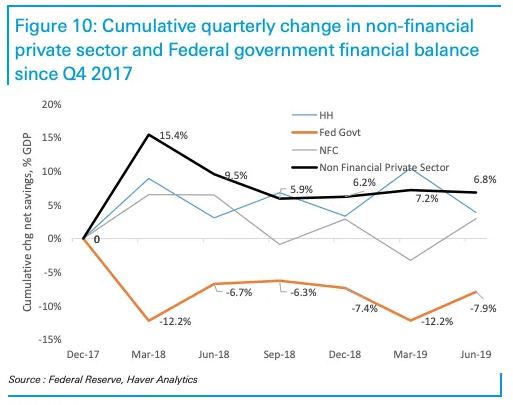

Have a look:

(Deutsche Bank)

(Deutsche Bank)

Through Q2 2019, the net economic stimulus from the tax cuts appears to have been almost entirely offset by private sector belt-tightening. Indeed, the chart above from Deutsche Bank's Stuart Sparks shows that in the two quarters immediately following the Trump tax cuts, the increase in private-sector net savings offset the fiscal belt-loosening – and then some. Through the first half of 2019, there was just a small net stimulative effect.

Simply put, the exploding deficit leaves no room for further stimulus lest the US should find itself on an even more perilous fiscal trajectory, the flood of Treasury supply to finance the deficit finally broke something in short-term funding markets in September and the tax cuts ran into a textbook stumbling block (as illustrated in the visual above).

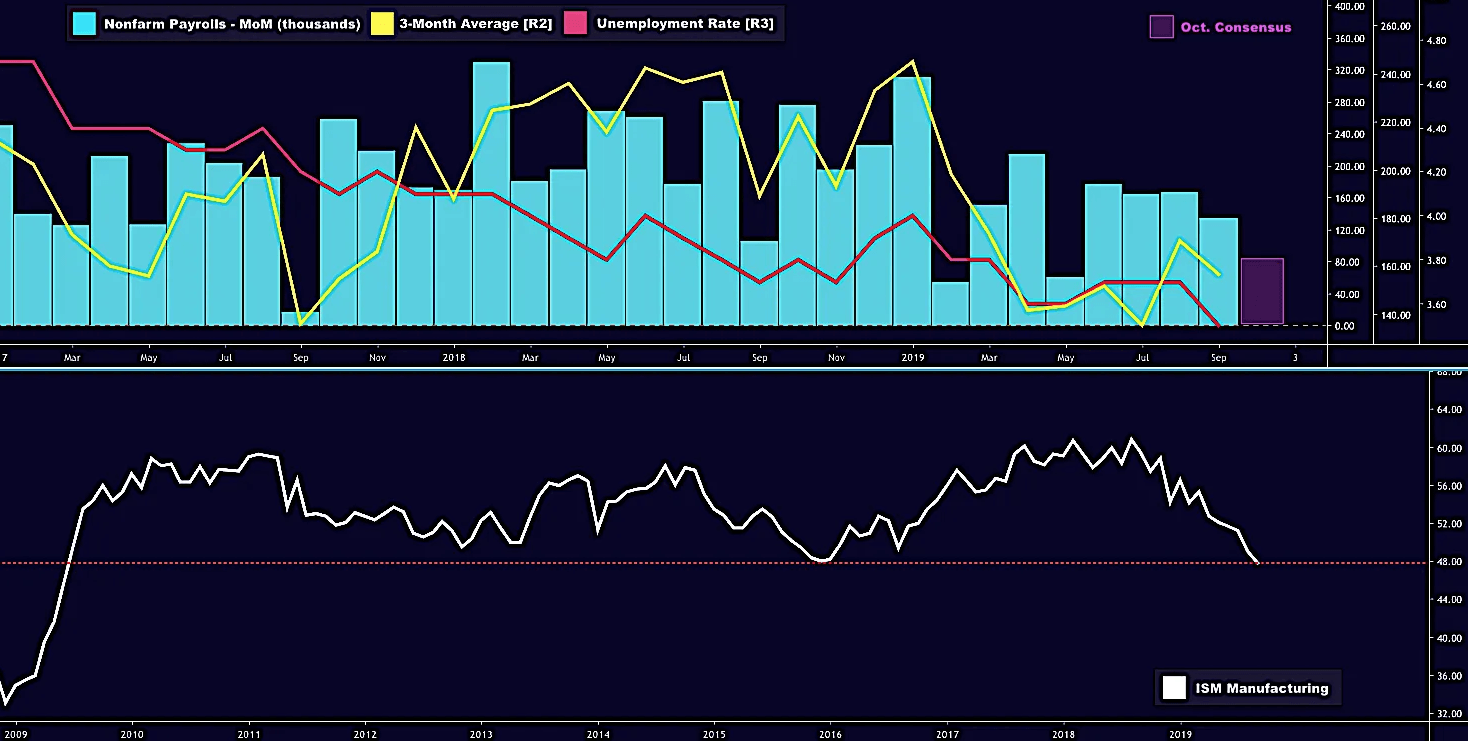

In addition to the first read on Q3 GDP, the market will get ISM manufacturing and the October payrolls report this week. On the former, the global factory malaise finally boomeranged back, making landfall stateside in August. We're now two months into a manufacturing downturn, and a rebound would be a welcome respite.

On the jobs report, the General Motors (NYSE:GM)-United Auto Workers strike will bite this month, and although the revisions that accompanied the September numbers made August and July look better, last month's headline (136k) was further evidence that even the labor market may be cooling. Consensus for the October headline is just 88k, which would represent one of the lowest prints of the Trump presidency.

(Heisenberg)

(Heisenberg)

Again, all of that is objective. That is a fact-based assessment of the current state of affairs, and what's important to keep in mind is that in most respects, it only seems "bad" by comparison to the unrealistic economic pronouncements and various Twitter balderdash that America has become accustomed to over the past two years.

That is (was and always will be) the sad irony: Until ISM dipped into contraction, there was nothing really "wrong" with the US economy and if we can get a bounce in the factory sector, that generally upbeat assessment will hold. The tragicomedy here is that simply describing a decent economy sounds like derision, because the bar was set so high that it was impossible to clear it. How does one expect to live up to expectations when those expectations are described in superlatives like "greatest in our country's history"?

Through it all, the Fed is attempting to walk a line between helping extend the longest expansion ever (and implicitly encouraging the pursuit of an impossible dream centered around achieving EM-like growth in the most advanced economy on the planet) and not chancing an overheat or the inflation of bubbles in financial assets.

Now that the data is starting to come in "weak" (and, again, "weak" is only an adjective that makes sense if you forget where we are in the cycle and benchmark everything against implausible expectations), Jerome Powell and company (sans Esther George and Eric Rosengren, who have never bought into the idea of rate cuts against the reality of decent data) have plausible deniability when it comes to cutting rates for a third time in three meetings, which they'll almost surely do on Wednesday.

This is where it gets tricky. Ideally, Powell would like to telegraph a pause, thereby "confirming" the characterization of rate cuts as a "mid-cycle adjustment." With stocks at record highs, and bonds having seemingly stabilized (yields had been rangebound for more than a week headed into Monday), this would be a good time to convey to the market that the job is done.

But that messaging risks tripping over the data as soon as it hits the tape. If the Fed tries to pull off a "hawkish cut" this week and the data doesn't play along, policymakers will immediately be behind the proverbial eight ball again, and you can be absolutely sure that President Trump will weigh in with his thoughts on Powell's press conference performance as judged by where the dollar and the S&P go on Wednesday afternoon.

Looking ahead, the problem with guiding markets towards a December cut is that four cuts since July would seriously undermine the characterization of this as a "technical" policy adjustment. It would be nearly impossible to say that four cuts in six months is merely an "adjustment," and in the event the data continues to deteriorate, it's hard to imagine how they (the Fed) stays off the lower bound.

Throw in the fact that cutting rates aggressively in 2020 would be seen as an overt political concession and you've got yourself a regular nightmare if you're Powell.

As far as the near-term outlook for US equities is concerned now that stocks have reclaimed the highs, Nomura's Charlie McElligott on Monday noted that "we are now seeing the grab into risk 'upside' begin to accelerate, particularly in the Equities complex."

He flags "monster strikes to the upside now at SPX 3050 ($7.5B) and 3100 ($6.1B)" and points to the "resumption of aggressive Vol selling from 'Yield Enhancement' and Systematic strategies."

Meanwhile, the Long/Short crowd is starting to gingerly re-leverage. Their beta to the S&P is up to the 10th percentile from just the 2nd over the past month amid the melt-up.

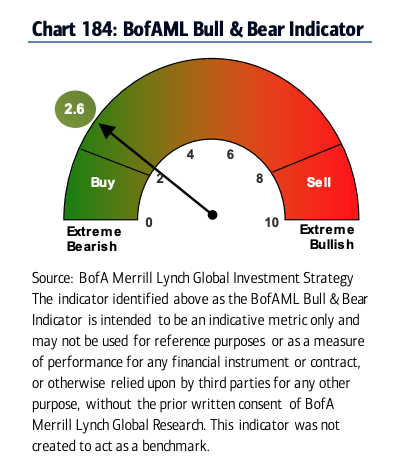

For what it's worth, BofA's Michael Hartnett sees the S&P climbing to 3,333 by March 2020. His famous "Bull & Bear" indicator is still near contrarian "buy" territory.

(BofA)

0 comments:

Publicar un comentario