Fumbling Around In The Dark

by: The Heisenberg

Summary

- On Friday, a friend of mine (one of the precious few I've got left) asked how I would teach an entry-level finance course in light of upside down markets.

- I was immediately reminded of an October 17 memo from Howard Marks.

- The fact is, valuing companies is no longer straightforward. Nobody quite knows how to do it anymore.

- One key question that emerges is: Who needs equity anyway?

- And still another: Are liabilities now assets?

- I was immediately reminded of an October 17 memo from Howard Marks.

- The fact is, valuing companies is no longer straightforward. Nobody quite knows how to do it anymore.

- One key question that emerges is: Who needs equity anyway?

- And still another: Are liabilities now assets?

Last week, Howard Marks delivered his latest memo. In what he describes as a break with precedent, he chose the topic based not on "a series of events [that] can be interestingly juxtaposed," but on "a request."

According to Marks, a colleague (Ian Schapiro, who leads Oaktree’s Power Opportunities group) suggested Howard write something about negative rates.

Howard's knee-jerk reaction (which he calls "immediate and unequivocal") was that such a request wasn't doable because when it comes to negative rates, "I don’t know anything about them."

After thinking about it, Marks realized that was precisely the point. Nobody knows anything about negative rates - not really, anyway.

And so, Marks essentially set about expounding on a collection of quotables and media clippings he says he's been "saving up." There's nothing particularly profound about Howard's latest (dated October 17), but, again, he makes no claims to profundity.

I wasn't going to cover Marks's negative rates memo, but ultimately, I did in a note published elsewhere last weekend. Since then, I've found myself revisiting Howard's piece on a couple of occasions, most recently on Friday evening, when one of the few remaining friends I have left called to ask me how I would approach teaching an entry-level finance course to undergraduates in light of the post-crisis monetary policy regime.

My initial response was that you really can't. Not unless you want to divide things into two sections – the way things used to be versus the way things are now; pre-crisis versus post-crisis, B.C. and Anno Domini (to quote something I penned earlier this month).

My friend sent me a link to an open-source finance text she intended to use, and I quickly realized that every, single chapter would have to be totally rewritten, or amended with footnotes and caveats at every turn if she hoped to somehow bridge the gap between how things used to work and how things work now, after a decade of QE and the proliferation of negative rates and other adventures in monetary Wonderland.

Ultimately, I recommended teaching the course by the book, and then assigning a series of recent academic journal articles as addenda near the end of the semester. I also suggested Marks's memo might be a good way to help folks transition from the old way of thinking about things to the post-crisis reality which, in many respects, is simply a fun house mirror image - a distorted reflection of the old rules.

One of the starkest examples of a world flipped upside down is the proliferation of negative-yielding corporate bonds. This is something I've discussed in these pages on several occasions, and elsewhere ad nauseam. Marks brings it up in his October 17 memo.

"How will the markets value businesses that hold cash versus those that are deep in debt?" Howard wonders.

Another way to frame the question is: How do things change when negative rates effectively convert liabilities into assets? Or, to quote Marks again: "If having negative-yield debt outstanding becomes a source of income, will levered companies be considered more creditworthy?"

I'm going to quote/paraphrase myself a bit in the next couple of paragraphs, so if some of the language sounds familiar, that's why.

It's important to remember that negative-yielding corporate debt isn’t so "anomalous" anymore – at least not across the pond. In other words, Marks isn't idly speculating about some quaint curiosity. At one point in late August, when yields plunged across the globe, more than €1 trillion of European corporate bonds sported yields less than zero.

That, BofA marveled at the time, was half of the entire € investment grade corporate credit market.

At one point this summer, there were 100 different issuers in the € debt market whose entire curve was negative.

In a sense, those corporates can essentially mint assets. Naturally, that would incentivize issuance.

"The risk is that companies begin to view negative yielding debt more as an ‘asset’ going forward, rather than a ‘liability’ and hence issue more of it," BofA’s Barnaby Martin wrote over the summer.

Marks echoed that last week. "Traditionally, markets have penalized heavily levered companies and rewarded those that are cash-rich."

But what happens when debt is an asset and cash is a liability? After all, if negative rates end up being passed along to corporate cash piles, that cash has a negative carry. Either it "earns" a negative yield on deposit, or you pay to store it somewhere, which is, in effect, the same thing (the cost of storage is essentially a tax).

Obviously, companies with massive cash balances would, in many cases, be healthy businesses and those which are highly-levered, not so much, so it's not as simple as saying "the more debt the better" in a world where the old rules no longer apply. But, this is an important discussion to have, because it raises very real questions about how to value companies which fall somewhere in the middle.

That is, what about a situation where two generally healthy companies are juxtaposed, and one chooses to opportunistically take on debt in a hypothetical environment of deeply negative corporate bond yields, while the other insists on holding a lot of cash on deposit when rates are negative?

That is, what about a situation where two generally healthy companies are juxtaposed, and one chooses to opportunistically take on debt in a hypothetical environment of deeply negative corporate bond yields, while the other insists on holding a lot of cash on deposit when rates are negative?

The leveraged company isn't taking on the debt because they necessarily need to, but rather because in a world where the rules are upside down, it's the "right" thing to do.

If both businesses are thriving, which of those companies should command a premium? Or, as Marks puts it, "How will the market value businesses that hold a lot of cash and thus have to pay banks to keep it on deposit?"

Now you might be asking yourself: Ok, Heisenberg, but isn't this all just a thought experiment?

No. No, it is not. Because as noted above, this is the reality in Europe, and it's likely to become more "norm" than "exception" in other locales going forward, as central banks restart asset purchases and begin cutting rates anew.

The chart in the left pane below shows that policymakers are now cutting rates at an even faster clip than the trend in realized inflation dictates. The chart on the right shows that "peak" Quantitative Tightening has long since passed.

(BofA)

(BofA)

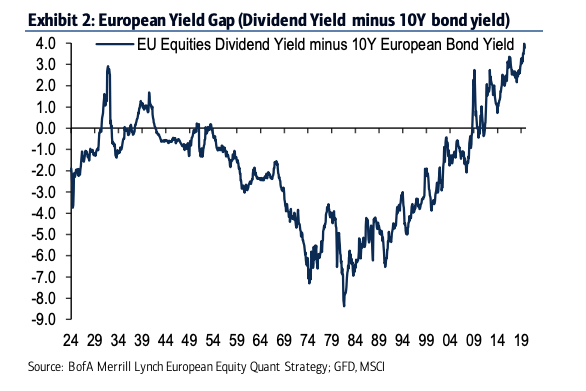

Take a minute to consider what this means for how corporates finance themselves. As the above-mentioned Barnaby Martin writes in a note dated Friday, "the gap between equity and debt costs in Europe is at a 100-year high."

(BofA)

(BofA)

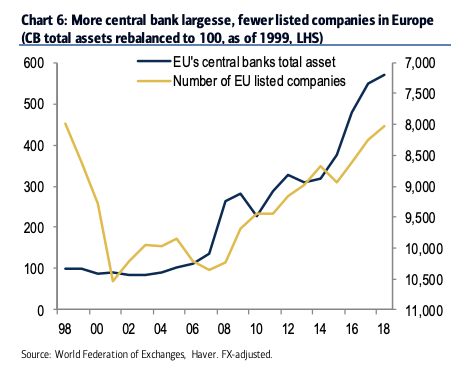

Clearly, that suggests that the trend of "de-equitization" is likely to continue. That is, the number of publicly-listed companies will almost surely shrink.

Indeed, over the post-crisis period, the number of EU-listed companies has collapsed by 25% from more than 10,000 to roughly 8,000 as EU central bank balance sheets have grown.

(BofA)

(BofA)

If you're wondering whether a similar relationship shows up if you plot the number of EU-listed companies with the average bank lending rate to non-financial corporates and the average effective yield on € IG credit, the answer is "yes."

At the same time, the global store of private capital "dry powder" has exploded to more than $2 trillion amid the hunt for yield. As BofA's Martin goes on to write in the same cited note, "while Private Equity accounted for a shrinking proportion of dry powder between 2006-2013, PE now accounts for almost 60% of available dry powder, the largest proportion observed since 2012." That could potentially accelerate the de-equitization process if management and shareholders decide to go the PE route.

All of this has two obvious consequences.

First, credit markets will continue to expand, and that brings risk. The more forgiving the debt market, the more tempting it will be, and as you might imagine, debut issuers across buckets within IG tend to be more highly-levered than their established counterparts.

First, credit markets will continue to expand, and that brings risk. The more forgiving the debt market, the more tempting it will be, and as you might imagine, debut issuers across buckets within IG tend to be more highly-levered than their established counterparts.

Perhaps even more importantly, BofA notes the following about the perils of a less "real-time" (as it were) market:

We think the long-term consequence of de-equitization is that markets will be less able to assess the real-time state of the economy. Fewer listed companies mean fewer disclosures about how earnings are faring, how business segments are performing, how geographical earnings splits are evolving… and ultimately, fewer disclosures about emerging risks. And if there is a less reliable pulse on the economy, then this could impart more volatility to the consensus trades of the future, as markets suddenly realize that the "facts have changed."

When you throw in the cross-asset trend of deteriorating liquidity, you're left to ponder a world where investors are increasingly forced to fumble around in the dark.

And that brings us back full circle to Marks's memo and my friend who is facing the unenviable task of trying to explain some of these upside down dynamics to undergraduates.

We're all fumbling around in the dark.

We're all fumbling around in the dark.

Or, as Howard puts it, "I’m convinced that no one should be categorical about how to deal with a mystery like this in such unprecedented and confusing circumstances."

0 comments:

Publicar un comentario