Lenders in Europe could need to raise another $148 billion to meet the latest tranche of regulations introduced in the wake of the financial crisis

By Rochelle Toplensky

Share buybacks worth a total of $4 billion offer a rare reason to get excited about Europe’s beleaguered banking sector right now. Investors should enjoy the boost while it lasts.

In their most recent quarterly results, Swiss banks UBSand Credit Suisseand Anglo-Asian lenders HSBCand Standard Chartered reaffirmed plans to repurchase $1 billion of stock each this year.

In a tough environment, the four banks want to return excess capital to shareholders while keeping their regular dividends at a sustainable level, and offset the dilution effect of dividends paid in stock.

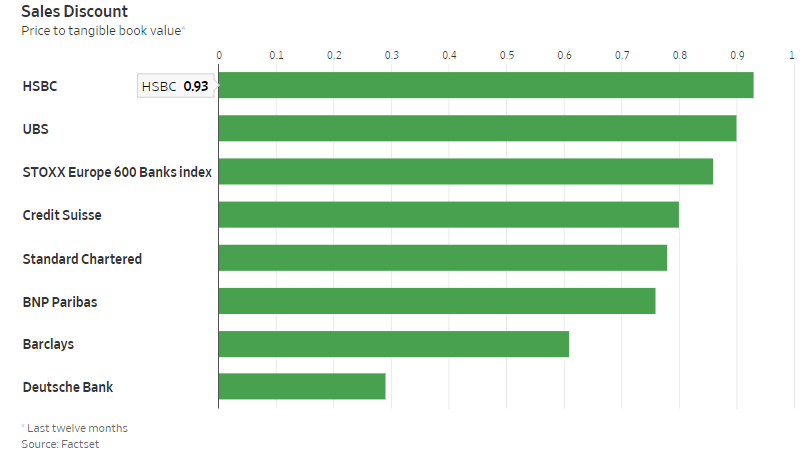

With their shares trading below book value, bankers also see buybacks as a good deal.

Within a couple of years, however, new rules could force big European banks to find a total of €134 billion ($147.6 billion) in additional capital, according to the local regulator’s estimates.

Buybacks are a luxury that Europe’s large lenders probably won’t be able to afford for much longer.

Most European bank results for the third quarter beat analysts’ low expectations, as a harsh climate of negative interest rates and slowing economic growth eased slightly.

Bank shares in the region are up 17% over the past three months.

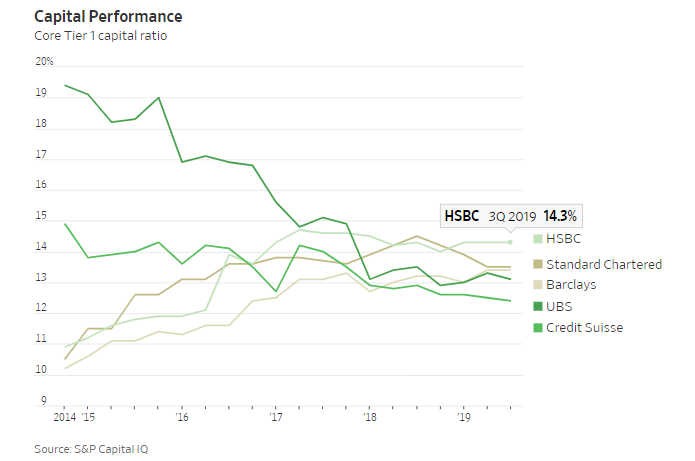

The four lenders with buyback plans delivered solid core Tier 1 capital ratios of around 13% and returns on tangible equity between 8% to 10% in the first three quarters—respectable by European standards.

Barclays has also hinted at share buybacks, but last quarter £1.4 billion ($1.79 billion) of its excess capital was soaked up by a historical insurance-selling scandal.

European banks have been doing plenty of restructuring in recent years to boost returns, but with the realization that subzero rates are here to stay, possibly for years, most are looking to reduce expenses and reshape their businesses even further.

Deutsche Bank started its latest overhaul in July, with a forecast 18,000 job cuts; HSBC has promised to deliver a new plan to remodel its business alongside its year-end results in February.

The need for more capital will add to the challenges.

The European Banking Authority, the regional regulator, calculates that the region’s large banks will have to increase their capital by a quarter, assuming they maintain their current business model.

The majority of the changes are effective from Jan. 1, 2022, though some won’t be fully phased in until 2027. While many in the industry hoped the EBA would delay or water down the regulations, it has instead fully supported the new standards—though it does still have time to reconsider that decision.

European banks have been doing plenty of restructuring in recent years to boost returns. Photo: miguel medina/Agence France-Presse/Getty Images

The incoming rules are the final tranche of Basel regulations agreed after the global financial crisis in an effort to strengthen the financial system. This batch determines the level of risk a bank can assign to different asset types, with riskier assets requiring the bank to hold more reserves.

European banks need to meet the new capital requirements even as they compete against larger, richer U.S. rivals that are benefiting from higher domestic interest rates and returns—and who won’t have to find new capital. U.S. regulators, in contrast to the EBA, are expected to implement the new Basel regulations in a way that doesn’t require additional capital. They are also considering easing some existing banking rules.

With such a huge capital call on the horizon, the spending spree on share buybacks will likely have to end.

Third-quarter results offered a glimmer of light for investors in European banks, but the skies ahead are darkening.

0 comments:

Publicar un comentario