The Most Crowded Trade

by: Lyn Alden Schwartzer

Summary

- Being long the dollar and dollar-related assets (especially Treasuries at the moment) has been the most popular trade this year and for most of the past decade.

- We may be reaching a tipping point for the dollar, where a multi-year bullish trend reaches its apex and sets up for a reversal.

- Look for a weaker dollar in 2020. Nothing is for certain, but that's how the math seems to converge.

- We may be reaching a tipping point for the dollar, where a multi-year bullish trend reaches its apex and sets up for a reversal.

- Look for a weaker dollar in 2020. Nothing is for certain, but that's how the math seems to converge.

According to Bank of America Merrill Lynch, being long U.S. treasuries (TLT) has been the most crowded trade over the past four months into September.

This is a good cyclical play. When growth is slowing, back-tests show that going into the dollar and treasuries makes sense as a safe-haven trade.

However, that cyclical play is starting to run into a structural trend, where rising U.S. deficits are starting to matter. This is likely going to require a weaker dollar to fix, and the market is inherently self-correcting. It's largely a question of timing at this point.

I find very few investors that are bearish on the strength of the dollar (UUP) or bullish on anti-dollar bets like emerging markets (EEM). Being long the dollar and viewing dollar-denominated assets as a safe haven is today's most-crowded trade.

Deficit-Driven Liquidity Shortage

A significant chunk of U.S. economic outperformance over the past five years has been about fiscal stimulus.

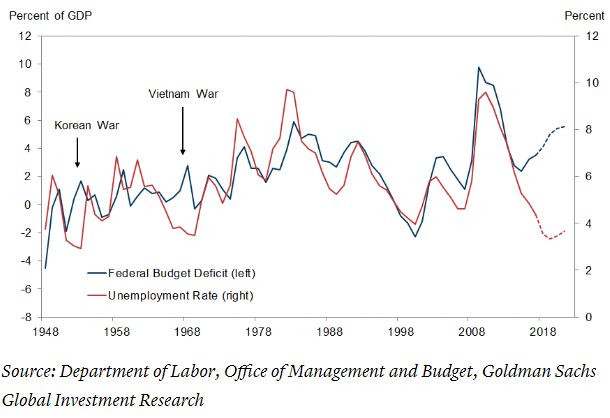

In my opinion, this next chart is one of the most important visuals to be aware of over the next few years and I've included it in a few recent articles, because this isn't going away. The blue line is the U.S. federal budget deficit as a percentage of GDP. The red line is the unemployment rate. For the first time in modern history, the U.S. deficit is widening to a large deficit during a non-wartime non-recessionary period:

Chart Source: Goldman Sachs, Retrieved from CNBC

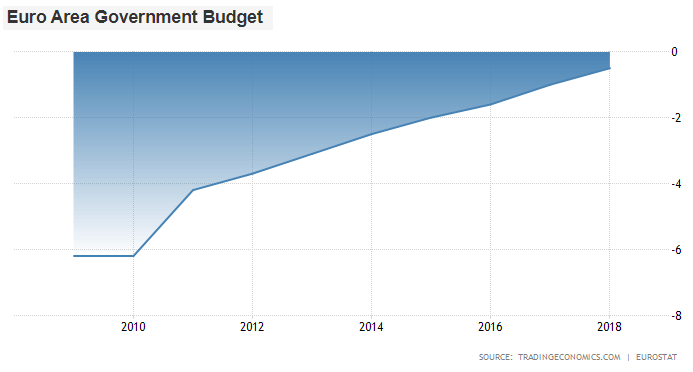

Meanwhile, the Euro Area has focused on austerity. As a group, they have consistently reduced their budget deficits each year so that now, at under 1%, their debts are growing more slowly than nominal GDP.

Chart Source: Trading Economics

Chart Source: Trading Economics

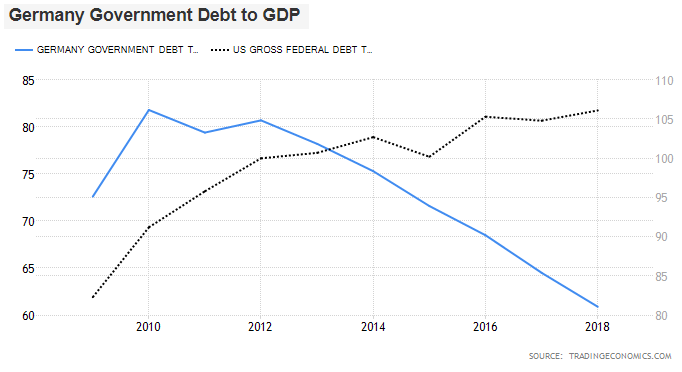

For example, the United States (black dotted line, right axis below) grew its debt as a percentage of GDP from 62% to 106% over the past decade while Germany (blue line, left axis) decreased its debt as a percentage of GDP from 73% to 61%:

Chart Source: Trading Economics

Chart Source: Trading Economics

So, not only does the U.S. have massive unprecedented fiscal stimulus equal to about 5% of GDP during non-recession peacetime, but we're doing so from the highest base of debt-to-GDP that the U.S. has had since World War II.

On the other hand, U.S. monetary policy has been the reverse of its fiscal policy. The Bank of Japan and European Central Bank have locked rates at zero and performed quantitative easing at a far larger scale relative to GDP than the U.S. Federal Reserve. The Federal Reserve stopped quantitative easing in 2014, performed quantitative tightening for a brief time, and raised rates about 2.5% higher than its peers. On that front, the U.S. has been by far the most hawkish one. However, the big fiscal stimulus is what gave the Fed ability to be hawkish.

The result of looser fiscal policy and tighter monetary policy than its peers over the past five years has been stronger U.S. economic growth than the rest of the developed world while simultaneously having a strong dollar, but such a situation is temporary and likely getting close to its apex.

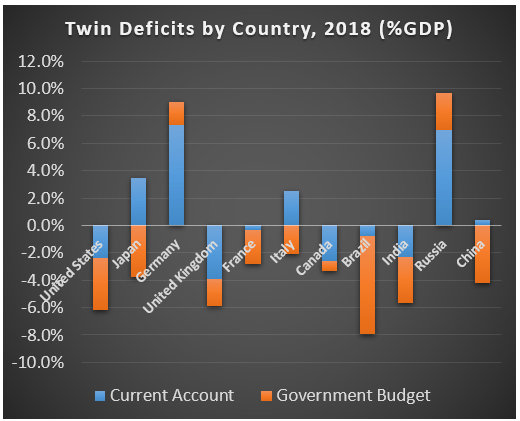

The United States has the largest twin deficit (government deficit/surplus + current account deficit/surplus) out of its developed peers, and higher than many of the BRIC nations:

Data Source: Trading Economics

This twin deficit doesn't matter in the short-term, but it matters significantly in the long-term.

As I'll describe below, the United States appears to be reaching a point where its debts and deficits are starting to matter, causing its monetary policy to reverse, and there are some specific catalysts to look for as it relates to timing.

The Market is Usually Self-Correcting

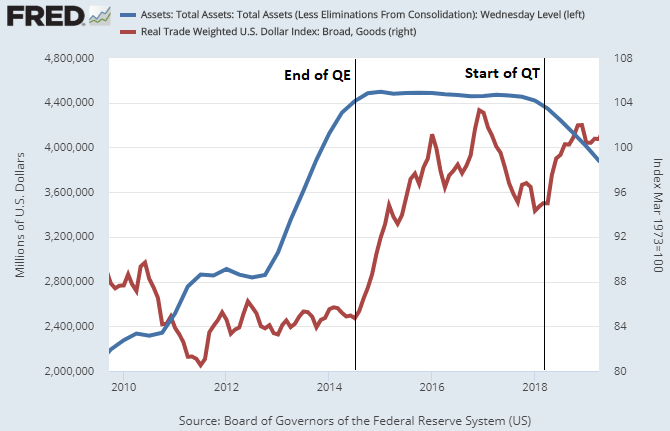

In late 2014, the Federal Reserve finished its third and final round of quantitative easing (QE), meaning they stopped "printing money" to buy U.S. government debt from institutions. This removed a significant source of liquidity and left the U.S. economy to stand on its own two feet.

Dollar liquidity is a tricky thing, because as the world reserve currency, it's the primary currency for lending to emerging markets, buying commodities, and has all sorts of offshore uses.

The dollar quickly rose higher relative to many other currencies as that round of quantitative easing ended. The blue line in the chart below is the Fed's balance sheet (when it's going higher, that's quantitative easing), and the red line is the trade-weighted dollar index. Once QE ended, the dollar shot up. It was then choppy for a while, but the beginning of QT gave it another kick back up:

Chart Source: St. Louis Fed

Chart Source: St. Louis Fed

A country can't have growing deficits and growing debt vs GDP forever without QE, but they can do it for quite a while until a catalyst brings them to a halt.

Ironically for the United States, a strong dollar tends to be that catalyst.

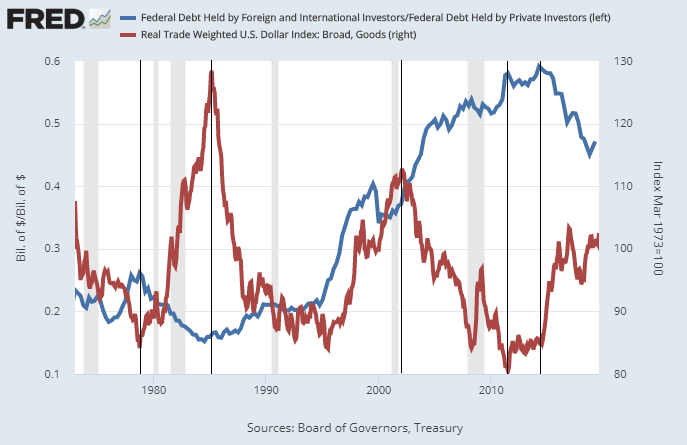

The following chart shows the percentage of U.S. privately-owned debt that is held by foreigners (blue line) compared to the trade-weighted dollar index (red line), with a few inflection points marked:

Chart Source: St. Louis Fed

Chart Source: St. Louis Fed

As the chart shows, there's a historical inverse correlation between dollar strength and the percentage of U.S. debt that foreign sources hold. Whenever the dollar grows stronger, the U.S. private sector ends up having to fund more of its own government's deficits. Foreigners stop buying, and may even begin selling to stabilize their own currencies.

The major exception on the chart where the inverse correlation broke down was in the 1990's. There was a three-decade trend from the mid-1980's to 2014 where foreigners were funding an increasing portion of U.S. deficits. They went from holding about 15% of privately-held U.S. debt to 60% of it.

This was during a rise of globalization, and particularly the rise of China. That foreign buying reversed course in late 2014, and they are now down to about 45% ownership of privately-held U.S. debt.

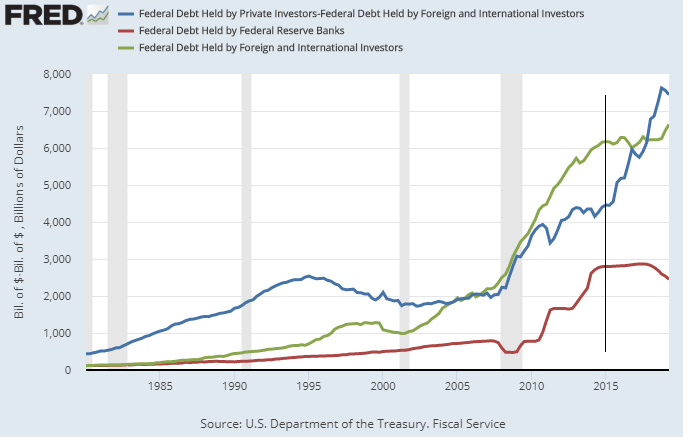

Starting in 2015, right after QE ended in the U.S. and the dollar became strong, foreigners stopped buying U.S. treasuries. Almost all new U.S. debt issued in the past five years (about $3 trillion worth) has been bought by domestic sources (blue line below). Foreigners (green line) and the Fed (red) have not been buying at significant scale:

Chart Source: St. Louis Fed

Chart Source: St. Louis Fed

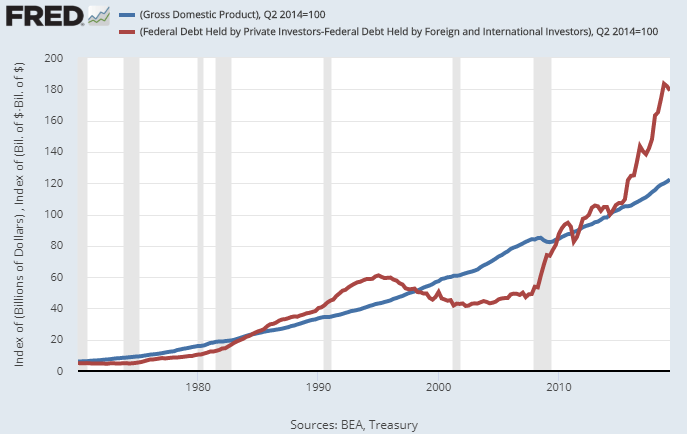

This is quite a lot of debt for domestic balance sheets to hold. The next chart shows the amount of U.S. government debt held domestically compared to U.S. GDP, indexed to 100 five years ago:

Chart Source: St. Louis Fed

Chart Source: St. Louis Fed

Basically, various institutions have increased their U.S. treasury holdings by 12.3% per year over the past five years compared to 4.1% annual nominal GDP growth over that time period.

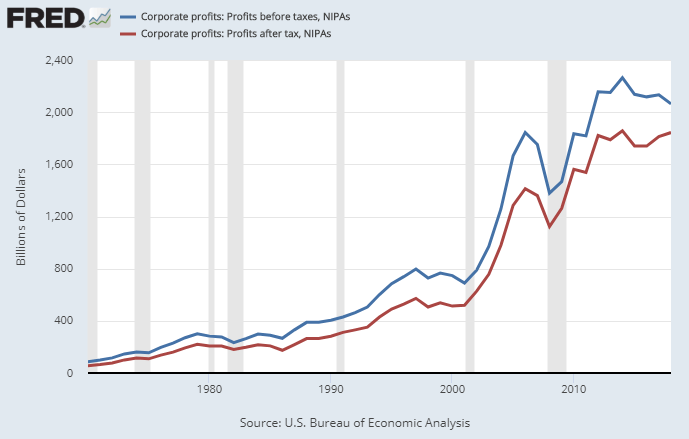

Additionally, U.S. corporate profits peaked in 2014 right when the dollar index shot up at the end of QE. Pre-tax profits are down since then, and after-tax profits have gone sideways thanks to tax cuts.

Chart Source: St. Louis Fed

Chart Source: St. Louis Fed

This shouldn't be a big surprise, considering that the S&P 500 is a large component of this and as an index they get over 40% of their revenue from foreign sources. All of those foreign income sources translate into fewer dollars when the dollar is strong.

This dollar strength has put a lot of pressure on the global economy. Many emerging markets have high dollar-denominated debts, so a stronger dollar effectively raises their debts and puts financial pressure on them, which has caused some of the weaker ones (i.e. Argentina and Turkey this time around) to fall into a currency crisis, and to slow the growth of others.

In addition, dollar strength puts a lot of pressure on the United States. Total corporate profits are down, so a combination of tax cuts, share buybacks, and valuation improvements have contributed to continued equity growth. And as previously mentioned, the U.S. has been forced to fund its own deficits.

In other words, the combination of loose U.S. fiscal policy and tight U.S. monetary policy is starting to strain the global system. Argentina and Turkey popped first, everyone has been strained, and now some leaks are starting to show up in the United States.

Repo Issues

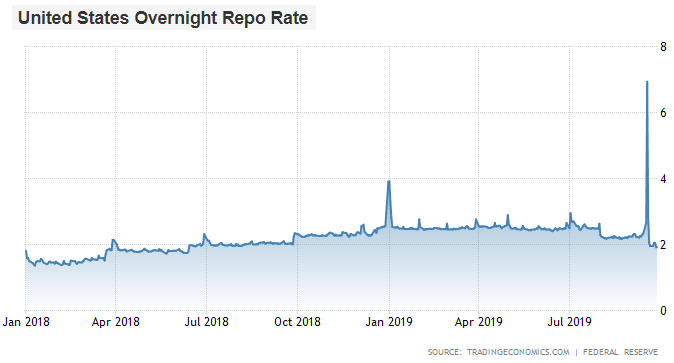

Most investors are aware that the overnight repo market has required Federal Reserve intervention every night for the past two weeks. Starting in mid-September, repo rates spiked, implying that banks don't have cash to lend to each other, and it required ongoing liquidity injections from the Fed to push back down:

Chart Source: Trading Economics

Chart Source: Trading Economics

Some commentators in financial media were freaking out because the last time the repo market was this bad was in September 2008 when U.S. banks were afraid to lend to each other overnight due to the risk that one of them would announce bankruptcy the next morning. That was an acute liquidity crisis due to an insolvent banking system.

Other commentators were saying the repo spike was nothing, just temporary timing issues. Quarterly corporate taxes were due mid-month. The U.S. Treasury is sucking up a couple hundred billion dollars in extra debt issuance to refill its cash reserves following this summer's debt ceiling issue that forced the Treasury to draw down its cash levels.

Evidence shows pretty clearly that the issue is somewhere in the middle. It was not and is not an imminent bank collapse liquidity crisis, nor was it purely a one-time thing. Instead, five years of domestic institutions fully-funding U.S. deficits basically saturated the banks with treasuries and they have trouble holding more. Their cash reserves have run low.

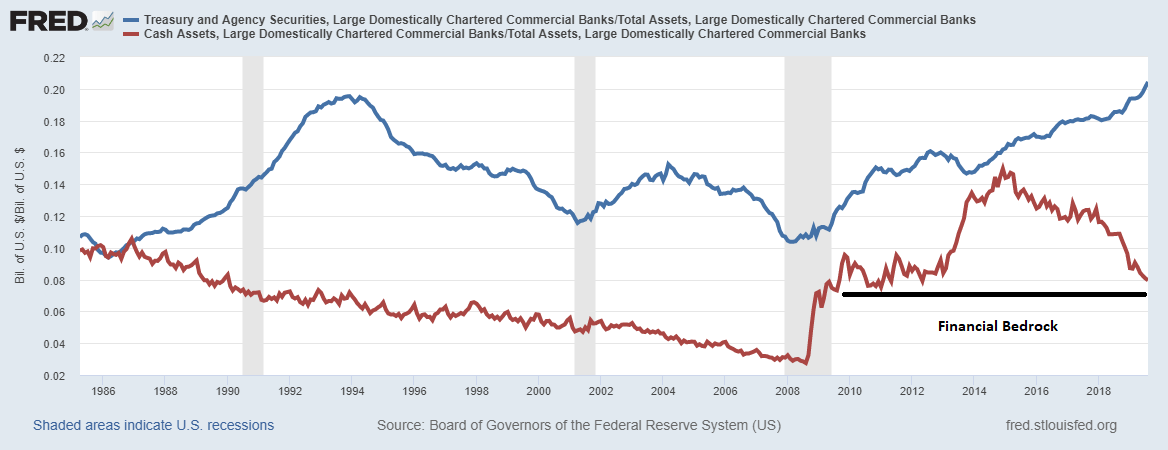

In particular, large U.S. banks that serve as primary dealers have been filling up with treasuries and drawing down their cash levels ever since QE ended. This chart shows the percentage of assets at large U.S. banks that consist of treasuries (blue line) vs the percentage of assets that consist of cash (red line):

Chart Source: St. Louis Fed

Chart Source: St. Louis Fed

Primary dealers are the market makers for treasuries. They don't really have a choice but to buy the supply as it comes, and supply is starting to turn into a fire hose and foreigners aren't buying much of it.

The percentage of total assets held as treasuries at large U.S. banks is now over 20%, which is the highest on record.

Cash as a percentage of assets at those institutions is now down to 8%, which is right at post-Dodd Frank post-Basel 3 lows. They're pretty much at the bedrock; they can no longer continue drawing down cash and using it to buy treasuries. Cash levels can't (and shouldn't) go lower like they did in the 2000's because that's the type of leverage that led to the financial crisis back then and current regulations require banks to have more cash.

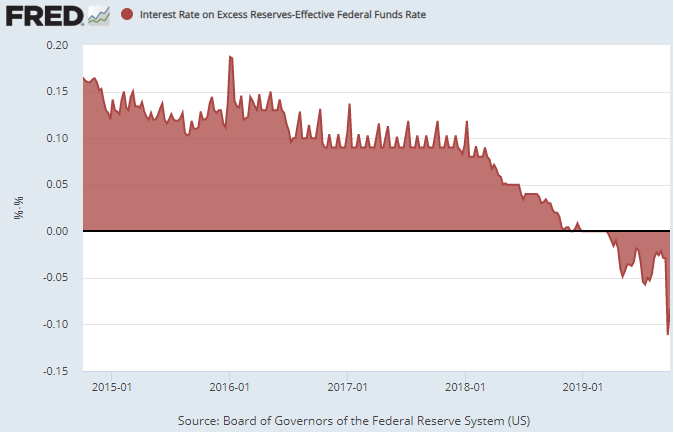

A lot of people are confused at how there can be too much supply of treasuries, because there is clearly investor demand for treasuries, especially long-duration treasuries that have performed very well this year.

However, most U.S. debt is short-term, and that sheer quantity of short-term debt has been pressuring the banks all year. Over the past few years, bid-to-cover ratios have been declining leading to some messy treasury auctions this year, and starting this spring, the federal funds rate has gone over the interest rate on excess reserves:

Chart Source: St. Louis Fed

Chart Source: St. Louis Fed

Clearly, this issue has been building for years and has accelerated throughout 2019, and September just happened to be when a couple extra pressures finally caused the system to reach its limit. It doesn't take a repo expert to see that it's not a repo-specific problem. It's a sovereign debt problem.

The Dollar's Apex is in Sight

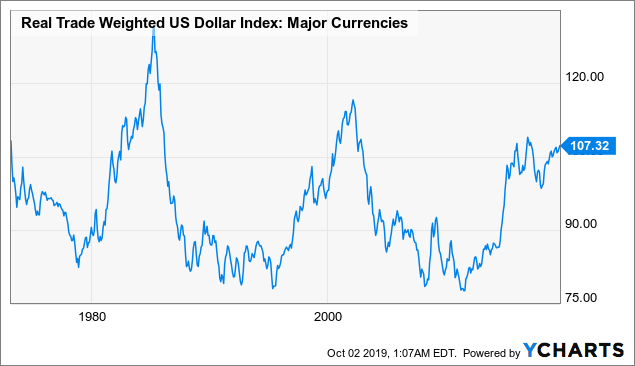

As this liquidity squeeze plays out and global economic growth continues to slow, the dollar is still in an upward trend, but these trends historically can reverse very quickly:

Data by YCharts

Data by YCharts

Unless the dollar weakens, foreigners are unlikely to resume buying U.S. treasuries at scale.

Even though U.S. treasuries pay higher rates than European or Japanese sovereign bonds, currency hedging eliminates that difference, so only investors daring enough to hold un-hedged U.S. treasuries can take advantage of that rate differential. This means that domestic institutions likely have to keep funding most the deficits of over $1 trillion per year, and primary dealers already clearly have a liquidity problem and are already holding a record amount of treasuries as a percentage of assets.

There are a few ways this can play out. The most likely outcome is that the Federal Reserve will begin expanding its balance sheet again by 2020 (or perhaps in this fourth quarter 2019) to relieve pressure from domestic balance sheets, which means that the Fed would essentially be monetizing U.S. government deficits. This would inject liquidity into the system, take some of the burden off of domestic institutions for absorbing all of those treasuries, and is likely to weaken the dollar which could allow foreign investors to step in and buy some more treasuries as well.

However, timing and details will be interesting.

Scenario 1) No U.S. Recession

If the Federal Reserve shifts from temporary open market operations "TOMO" to permanent open market operations "POMO" to permanent organic balance sheet expansion (QE by another name), it could address the issue for now.

Many investors assume that we would need a crisis scenario for the Fed to re-start QE, but as I showed with bank liquidity hitting bedrock and no end to U.S. debt issuance in sight, the Fed is likely to expand its balance sheet gradually simply due to liquidity pressures. They used to expand their balance sheet gradually prior to the global financial crisis anyway, so this would be a resumption of that but from a much higher starting point.

In a mild scenario, we could see the dollar leveling off and then weakening due to Fed easing, which could help some emerging markets show signs of life. It would give U.S. corporations some currency tailwinds for once rather than headwinds like they've had. In this case, I'd want to be positioned in emerging markets.

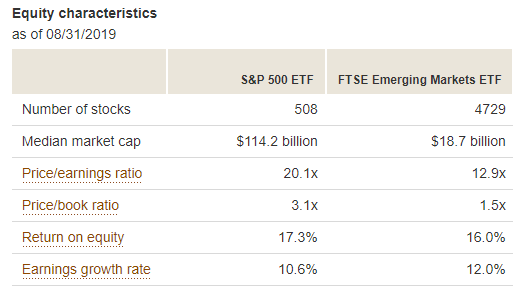

Vanguard has a good valuation/growth breakdown of the S&P 500 (VOO) and emerging markets (VWO) via their ETFs:

Table Source: Vanguard

Emerging markets have higher 5-year growth rates and much lower valuations. They would be my top choice in a weakening dollar environment.

As a recent data point, when the DXY dollar index dropped from about 100 to 90 in 2017, the MSCI emerging markets index soared over 37% in dollar terms. Lower debt burdens gave them a burst of earnings growth and then strengthening currencies added onto it for dollar-based investors.

However, I don't particularly like just owning an emerging market index due to how heavily weighted they are in China. I prefer analyzing individual markets based on growth, valuations, sector composition, stability, currency fundamentals, and debt levels. I'm optimistic about forward equity returns for Chile, Russia, India, South Korea, Taiwan, and a few others, especially if we get further sell-offs this quarter. I don't have a strong conviction either way on China at this time.

One of my favorite emerging market stocks at the moment is Sberbank (OTCPK:SBRCY) as a small position as part of a diversified portfolio. Many investors underestimate how resilient the company is, it has a single-digit P/E ratio, and it offers a very high dividend yield with a modest payout ratio.

I would have a moderate outlook on gold (GLD) in dollar terms in this scenario. It would benefit from a weaker dollar and lower U.S. interest rates, but without a recession it wouldn't get a fear trade. I'd be a buyer at current levels.

Scenario 2) U.S. Recession

In a more severe scenario, Fed dovishness and liquidity injections aren't enough to keep things going and the U.S. begins encountering recessionary conditions in 2020. We could have some rough earnings numbers for these last two quarters of 2019 (the one that just ended, and the next one), leading into ongoing weakness in 2020.

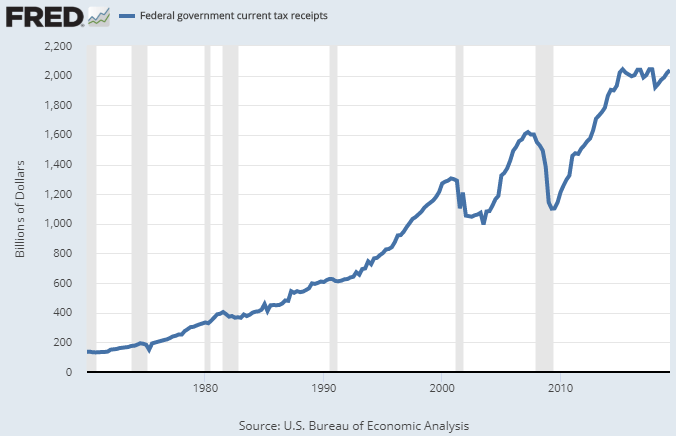

Recessions significantly reduce U.S. tax revenue:

Chart Source: St. Louis Fed

Chart Source: St. Louis Fed

If we have a recession in the coming year, it'll be the first one where the government is already running an annual deficit at 5% of GDP before the recession even begins, which could make for some very interesting situations. We could easily blow a $500 billion hole in the budget as a low-end estimate, and depending on any stimulus measures the government takes, the range of numbers goes up from there. Annual deficits could balloon from over $1 trillion to over $1.5 trillion or upwards of $2 trillion.

The amount of QE by the Fed to monetize U.S. deficits would likely be larger than many investors realize, just looking at it mathematically. I'd expect at least 20% dollar devaluation in the coming years, if not more.

In this scenario, I consider it highly probable that gold would do especially well. I also think emerging markets, while they would likely be in for a volatile time, would do better than most investors assume at these valuation levels and with a weaker dollar, and would come out strong on the other side of any sell-offs. The night is darkest just before the dawn, in other words.

Most investors have it in their minds that emerging markets necessarily do bad when the U.S. has a recession. The sample size for this, however, is just three. There have been only three U.S. recessions since the MSCI emerging markets index was created in the late 1980's. During the "big one" in 2007-2009, emerging markets were a bloodbath but for context, they went into that global crisis with record high valuations and high expectations, not low valuations and low expectations like we have now.

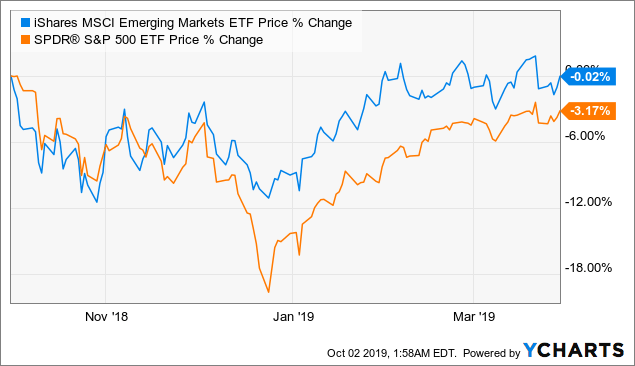

Look how emerging markets held up during the two quarters surrounding the flash crash of 4Q2018 compared to the S&P 500, even without a weaker dollar:

Data by YCharts

Data by YCharts

At these valuations, although I'd expect to see an emerging market draw down in a U.S. recession scenario, I'm optimistic about emerging markets coming out strong on the other side and would be a buyer of corrections, and particularly of select countries. Especially because, this time around, a weaker dollar is on the table and that would relieve some of their debt pressures like they enjoyed in 2017.

Final Thoughts

Summing this all together, there are multiple ways this can play out, but mathematically they all seem to require a lower dollar, one way or another.

It has been a longstanding belief that U.S. government debt and deficits are a far-off problem and don't really matter, but we are starting to run into tangible effects from treasury bill oversupply and in the coming years this will be a factor to work around. I classify U.S. debt/deficits as one of my four economic bubbles to be aware of.

The dollar has positive momentum at the moment, so it could trend higher in the short-term, but the higher it goes, the more it dooms itself by increasing the likelihood and timeline of a large U.S. recession and the associated debt monetization. Diversification is the safest way to play it. Traders may want to watch it for now, and be prepared to take advantage when/if the dollar strength turns over.

As far as I can tell, most of the dollar bulls who expect a much higher breakout in the dollar underestimate the damage that a strong dollar self-inflicts on the United States economy, which would then likely self-correct via a recession and major deficit monetization. The strong dollar reduces foreign corporate income and forces U.S. institutions to fund the U.S. government deficit, and after five years of doing this they are nearly tapped out and with flat dollar-denominated profits. Any major dollar breakout would likely be brief, self-correcting, and unpleasant.

I am including gold and emerging markets (with an emphasis on certain countries) in my portfolio, and which asset class will do better between the two will depend on how events unfold. I also have dry powder in the form of cash-equivalents and short-term bonds to add to my foreign or domestic equity allocation should we get a big equity sell-off later this year or in 2020.

0 comments:

Publicar un comentario