Here Comes The Deluge Of Meaningless “Good News”

by

Today’s relief rally is brought to you by chastened US and Chinese trade negotiators who are now working on a “mini” trade deal that will apparently include a reduction in US tariffs in return for some minor Chinese concessions on things like mandatory joint venture partners for foreign companies wanting to set up shop in China. In other words, it’s a face-saving exercise.

Yet stocks are soaring as investors focus on the above while ignoring the potentially much bigger deal of last night’s missile attack on an Iranian oil tanker.

But wait, there’s more. The Fed just promised to start buying Treasury bills at the rate of $60 billion a month and will keep it up through mid-2020. Just don’t call it QE – though in every mathematical way it is exactly QE.

And Brexit, that thing you stopped paying attention to last year, is suddenly looking like a non-catastrophe. From today’s Wall Street Journal:

It’s also worth noting that the markets’ ultimatum – and policymakers’ capitulation – are happening during a time of already extraordinarily easy money. Interest rates, of course, are at historically low levels (most sovereign bonds – including those of Greece – now trade with negative yields) and most major central banks are committed to even lower rates in the year ahead. In addition:

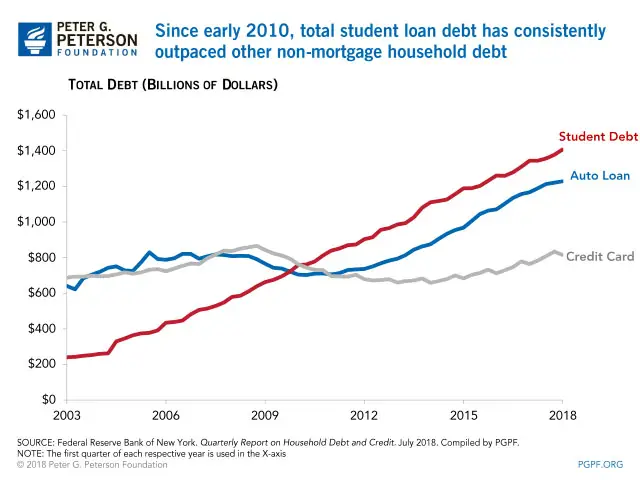

US government spending is rising twice as fast as tax revenues (7% versus 3.4% currently), which is another way of saying Washington is pumping hundreds of billions of new dollars into the economy each year. The Japanese central bank is talking about overshooting its inflation targets while both the outgoing and incoming heads of the European Central Bank are promising all kinds of exotic new QE to go with even more steeply negative rates. US corporate and student debt are both breaking records with each new update. The list of late cycle credit excesses just keeps going.

Yet this torrent of new credit isn’t enough to keep Germany out of recession (see German August export slump amplifies recession alarm), or the US from slowing down (see Second-quarter U.S. GDP left at 2%, slower economic growth seen persisting).

The implication?

The current batch of tepidly positive announcements will not do the trick and will therefore be followed by ever bigger and better ones, until easy money, massive government deficits, and soaring private sector credit stop working.

Then the only news that will matter is the fact that “good” news no longer matters.

Yet stocks are soaring as investors focus on the above while ignoring the potentially much bigger deal of last night’s missile attack on an Iranian oil tanker.

But wait, there’s more. The Fed just promised to start buying Treasury bills at the rate of $60 billion a month and will keep it up through mid-2020. Just don’t call it QE – though in every mathematical way it is exactly QE.

And Brexit, that thing you stopped paying attention to last year, is suddenly looking like a non-catastrophe. From today’s Wall Street Journal:

“Yesterday the Irish Taoiseach and the U.K. Prime Minister both saw – for the first time – a pathway to a deal,” said European Council President Donald Tusk during a news conference in Cyprus on Friday morning, using the Irish moniker for the leader. “I have received promising signals from the Taoiseach that a deal is still possible.”What do these seemingly-unrelated pieces of modestly positive news have in common? They all indicate that policy makers have gotten the markets’ message, which is that easy money is mandatory and anything that gets in its way will be met with a financial meltdown.

On Friday, [UK Prime Minister] Johnson also sounded cautiously optimistic. “There is a joint feeling that there is a way forward that we can see a pathway to a deal” Mr. Johnson said to reporters.

It’s also worth noting that the markets’ ultimatum – and policymakers’ capitulation – are happening during a time of already extraordinarily easy money. Interest rates, of course, are at historically low levels (most sovereign bonds – including those of Greece – now trade with negative yields) and most major central banks are committed to even lower rates in the year ahead. In addition:

US government spending is rising twice as fast as tax revenues (7% versus 3.4% currently), which is another way of saying Washington is pumping hundreds of billions of new dollars into the economy each year. The Japanese central bank is talking about overshooting its inflation targets while both the outgoing and incoming heads of the European Central Bank are promising all kinds of exotic new QE to go with even more steeply negative rates. US corporate and student debt are both breaking records with each new update. The list of late cycle credit excesses just keeps going.

Yet this torrent of new credit isn’t enough to keep Germany out of recession (see German August export slump amplifies recession alarm), or the US from slowing down (see Second-quarter U.S. GDP left at 2%, slower economic growth seen persisting).

The implication?

The current batch of tepidly positive announcements will not do the trick and will therefore be followed by ever bigger and better ones, until easy money, massive government deficits, and soaring private sector credit stop working.

Then the only news that will matter is the fact that “good” news no longer matters.

0 comments:

Publicar un comentario