After years of calm, the financial regulator under chief John Williams must show it can tamp down unexpected turbulence

By Nick Timiraos

.

The Federal Reserve Bank of New York on Sept. 17, when the short-term ‘repo’ rate spiked as high as 10%. Claudio Papapietro for The Wall Street Journal

John Williams, a Ph.D. economist and Federal Reserve lifer, made his mark inside the central bank with his deep knowledge of interest-rate theory and a solid record as a policy maker and communicator.

When Mr. Williams won a big promotion to Federal Reserve Bank of New York president last year, senior officials didn’t see his lack of financial-markets experience as a liability. He was so new to the markets side of the job that, in his first month in New York, he received an hourlong tutorial on using a Bloomberg data terminal, Wall Street’s ubiquitous trading-desk tool.

Now his market savvy is being put to the test.

After years of calm, the New York Fed is tamping down an unexpected bout of turbulence in money markets that caught officials and investors off guard this month. A sudden shortage of cash caused interest rates to spike unexpectedly on very short-term loans banks make to each other overnight, called repurchase or “repo” agreements.

“There is a serious question about why they didn’t foresee it,” saidNathan Sheets,chief economist at investment-advisory firm PGIM Fixed Income, who previously held senior Fed and Treasury Department posts. “Why were they surprised? What did they miss? And was that a reflection of something not happening at the New York Fed on the desk or elsewhere?”

In an interview, Mr. Williams rejected the idea that the central bank was behind the curve in responding to the market volatility. The New York Fed followed a “consistent approach of assessment, coming up very quickly with an appropriate plan, and executing that,” he said. “This is really the Fed at its best.

The Fed’s approach will be tested Monday, when the third quarter ends and banks may refrain from overnight lending in order to show strong balance sheets. Reduced lending could put pressure on the repo market and create more volatility.

The New York Fed said it plans to keep injecting funds through Oct. 10 and has increased the sizes of these injections in recent days.

Mr. Williams and his colleagues must also solve the mystery behind the money-market dysfunction: Why did banks, seemingly flush with reserves, choose not to lend as rising repo rates created a quick profit opportunity? Officials are studying the role of new regulations and other postcrisis market structure issues. Regardless of the cause, such volatility isn’t good—in stressed conditions, it could force hedge funds and others that rely heavily on short-term loans to dump assets, disrupting markets and impairing the flow of credit to the economy.

The New York Fed, in a castle-like fortress two blocks from Wall Street, serves as the central bank’s nexus between the financial markets and the economy. It provides the U.S. government’s real-time eyes and ears on trillions of dollars that flow through global markets daily. Its staff played critical roles designing rescue programs and monitoring banks when broken credit markets sent the financial system to the brink of collapse between 2007 and 2009.

‘This is really the Fed at its best,’ says New York Fed chief John Williams, here in August, about its response to the money-market volatility. Photo: David Paul Morris/Bloomberg News

‘This is really the Fed at its best,’ says New York Fed chief John Williams, here in August, about its response to the money-market volatility. Photo: David Paul Morris/Bloomberg News Mr. Williams took the helm in June 2018 after a career as an economist at the Washington-based board of governors and then the San Francisco Fed, where he became president in 2011. His predecessor in New York,William Dudley, had overseen markets operations after serving as chief economist at Goldman Sachs .

Mr. Williams co-wrote seminal research on policy-setting rules and models to estimate a theoretical neutral level of interest that neither spurs nor slows growth, something economists call “r-star.”

A punk and classic-rock music aficionado, he sprinkled speeches with lyrical references to Led Zeppelin and The Clash. When he left San Francisco, staffers presented him with an “R-Star” T-shirt with the gothic lettering of the rock band AC/DC’s logo.

.

Funding pressure

This month’s trouble bubbled up Monday, Sept. 16. Mr. Williams and Lorie Logan, the executive who is interim manager of the Fed’s portfolio, had traveled to Washington with other senior staffers ahead of the central bank’s two-day rate-setting policy meeting.

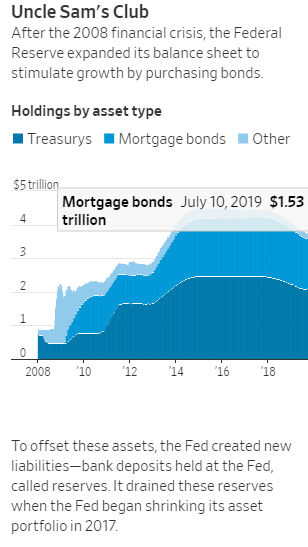

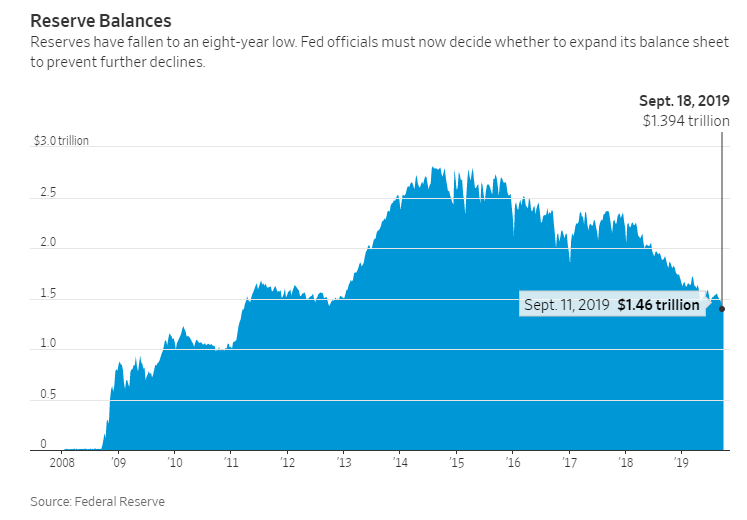

Potential for funding pressures in money markets had been building for months due to regulatory changes, rising Treasury bond issuance and steady declines in deposits banks hold at the Fed—known as reserves—the result of the Fed’s 2017 decision to shrink its balance sheet.

The Fed had been surveying banks for months about their demand for reserves but didn’t think they were near this point that would lead to funding pressures.

Officials knew some large payments of corporate taxes and Treasury auction settlements on Sept. 16 would result in a large transfer of cash from banks to the government. But they believed money markets could digest them because similar payment dates in April and June hadn’t roiled markets.

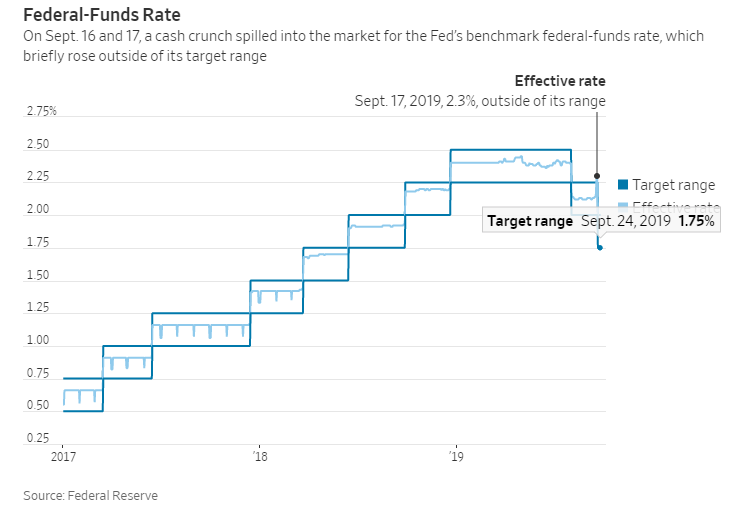

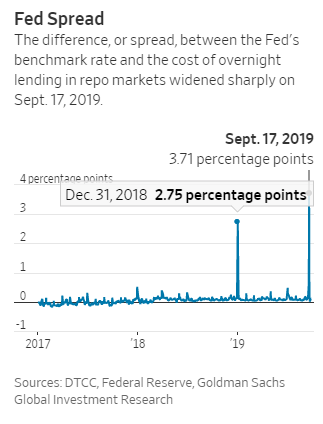

A cash crunch began building that afternoon in repo rates. This year, rates on repurchase agreements usually have been no more than a 10th of a percentage point above the effective fed-funds rate, or around 2.2% in August and early September. They reached 5% on Sept. 16.

Pressure intensified when repo desks began rolling over loans early Tuesday, Sept. 17, with the repo rate rising as high as 10%. Even then banks refused to lend, passing up big profits to hold on to their cash.

The dysfunction led the Fed’s benchmark federal-funds rate to rise to 2.3%—above its 2%-to-2.25% target range—going outside of the target range for the first time since the central bank began setting a range during the 2008 crisis.

From temporary offices at Fed headquarters in Washington, Mr. Williams, Ms. Logan and their team assessed what was roiling markets and what operations were needed to restore liquidity. They decided to inject $75 billion in cash into money markets, the first such move since the crisis.

Traders didn’t hear anything from the Fed until 9:15 that morning, several hours after rates began spiking, minutes before the U.S. stock market opened and an hour before the Fed’s policy meeting would start.

“Market confidence in the New York Fed markets desk is critical, and a series of events here have, let’s say, dinged confidence in the operations,” saidWard McCarthy,chief financial economist at financial-services company JefferiesLLC. “It’s important that the confidence issue be addressed before it becomes a more significant problem.”

Mr. Williams in the interview defended the bank’s response, saying, “We diagnosed it right, and Lorie and her team worked with others to get that done and get it done quickly.”

Some analysts said that the Fed ultimately made the right calls but that the incident showed officials had miscalculated the quantity of reserves needed in the system and how tight funding markets would get as a result.

“The lack of response on Monday was unnerving,” saidMark Cabana,head of short-term interest-rate strategy research at Bank of America Merrill Lynch. “They came in on Tuesday, but they came in too late.”

Mr. Williams’s team was making its moves without key leadership after he ousted two veterans. In late May, Mr. Williams announced the departure ofSimon Potter,head of the markets desk since 2012, andRichard Dzina,head of financial services. They had joined the New York Fed in 1998 and 1991, respectively. People familiar with the matter said the exits had less to do with particular policy disputes than with tension over day-to-day management issues.

The way Mr. Williams executed the abrupt departures rattled upper management and sank staff morale, current and former staffers said. Mr. Potter learned of the decision from Mr. Williams shortly before he was to deliver a keynote address in Hong Kong that had already been announced.

At a going-away party at the New York Fed’s headquarters, Messrs. Potter and Dzina received an extended ovation that kept Mr. Williams waiting offstage to address attendees. “It was maybe three minutes,” said one attendee. “It is hard to describe how awkward the air felt.”

Last month, the New York Fed said Mr. Williams planned to break the top job of overseeing markets into two positions—one to oversee the central bank’s securities portfolio and implement monetary-policy decisions, another to handle market operations, outreach and technology.

Federal Reserve Bank of New York in Lower Manhattan. Photo: Claudio Papapietro for The Wall Street Journal

Mr. Williams, in the interview, said the leadership vacancies were “in no way interfering with the work we’re doing, and our ability to do our very best.”

Mr. Williams himself had previously roiled markets, unintentionally, in a July 18 public speech on the eve of the central bank’s quiet period before its July policy meeting. He expounded on 20 years of research that called for more aggressive and pre-emptive action to shore up the economy at any sign of weakness.

He had delivered similar comments before. But the context of these remarks—from a top lieutenant to Fed ChairmanJerome Powelljust before the Fed’s first rate cut in a decade—led markets to change their expectations about what the Fed would do. Markets began anticipating the Fed would cut interest rates by a half-percentage-point, instead of a quarter point, at the July 30-31 meeting.

Hours later, the New York Fed issued a rare clarification that markets had misunderstood the speech. Mr. Williams hadn’t meant to send a signal about the size of the coming rate cut.

Mr. Williams and Mr. Powell must now lead their colleagues through a series of decisions, including:

• when to let the Fed’s asset portfolio begin growing again;

• whether to add additional reserves, which would require larger purchases of Treasurys;

• what mix of Treasury securities to add;

• whether to replace the Fed’s benchmark rate with something more widely traded;

• whether to launch a new tool that could alleviate cash crunches without daily ad hoc injections, and how to design it.

“Where the Fed left itself vulnerable,” saidJim Vogel,a rates strategist at fixed-income broker FTN Financial, “was to postpone all of those decisions, and to do it so publicly.”

—Liz Hoffman and Akane Otani contributed to this article.

0 comments:

Publicar un comentario