Rise in negative-yielding debt accelerates over summer

Robin Wigglesworth

© AP

Fears over recession are once again stalking markets, but many investors and analysts are more worried about a deeper, more structural shift: that the world economy is succumbing to a phenomenon dubbed “Japanification”.

Japanification, or Japanisation, is the term economists use to describe the country’s nearly 30-year battle against deflation and anaemic growth, characterised by extraordinary but ineffective monetary stimulus propelling bond yields lower even as debt burdens balloon.

Analysts have long been concerned that Europe is succumbing to a similar malaise, but were hopeful that the US — with its better demographics, more dynamic economy and stronger post-crisis recovery — would avoid that fate.

But with US inflation stubbornly low, the tax-cut stimulus fading and the Federal Reserve now having cut interest rates for the first time since the financial crisis, even America is starting to look a little Japanese. Throw in the debilitating effect of ongoing trade tensions and some fear that Japanification could go global.

“You can get addicted to low or negative rates,” said Lisa Shalett, chief investment officer of Morgan Stanley Wealth Management in New York. “It’s very scary. Japan still hasn’t gotten away from it . . . The world is in a very precarious spot.”

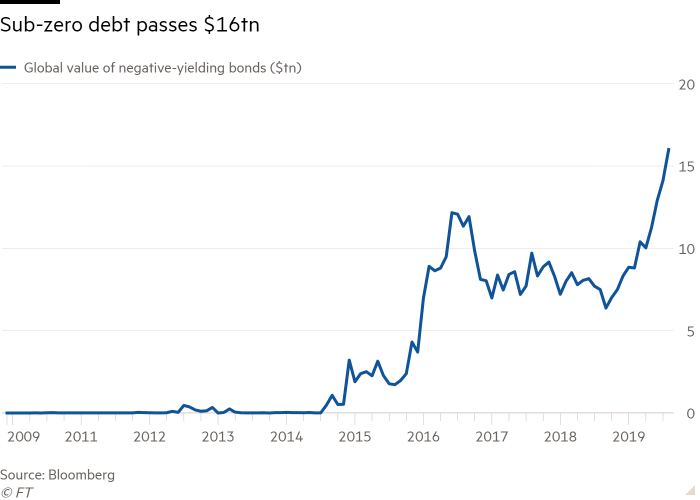

The primary symptom of spreading Japanification: the rise of negative-yielding debt, which has accelerated over the summer. There is now more than $16tn worth of bonds trading with sub-zero yields, or more than 30 per cent of the global total.

Japan is the biggest contributor to that pool, accounting for nearly half the total, according to Deutsche Bank. But the entire German and Dutch government bond markets now have negative yields. Even Ireland, Portugal and Spain — which just a few years ago were battling rising borrowing costs triggered by fears they might fall out of the eurozone — have seen big parts of their bond markets submerged below zero.

As a result, the US bond market is no longer the best house in a bad neighbourhood: it is pretty much the only house still standing. US debt accounts for 95 per cent of the world’s available investment-grade yield, according to Bank of America.

The US economy continues to expand at a decent pace, with strong consumption offsetting a weaker manufacturing sector. Even inflation has ticked up a little. But some economists fret that a manufacturing contraction will inevitably affect spending, so forecasts have been slashed for this year and next. Some even fear a recession may be looming.

“Black-hole monetary economics — interest rates stuck at zero with no real prospect of escape — is now the confident market expectation in Europe and Japan, with essentially zero or negative yields over a generation,” Larry Summers, the former Treasury secretary, noted last weekend. “The United States is only one recession away from joining them.”

He added: “Call it the black-hole problem, secular stagnation, or Japanification, this set of issues should be what central banks are worrying about.”

The global economy’s darkening outlook was certainly a major topic at last week’s annual central bankers’ jamboree at Jackson Hole. There, mounting trade tensions and the harsh reality of the limited powers of monetary policy to boost growth cast a pall over discussions.

“Something is going on, and that’s causing . . . a total rethink of central banking and all our cherished notions about what we think we’re doing,” James Bullard, president of the St Louis Federal Reserve, told the Financial Times. “We just have to stop thinking that next year things are going to be normal.”

Most analysts and investors remain optimistic that a US recession can be averted, given that the Fed has shown its willingness to cut interest rates to support growth. Instead, a scenario something akin to Japan’s looks more likely, judging from still-elevated stock prices and interest rate futures. While this might appear more benign than a full-blown downturn, the implications are far from positive.

For one, it might mean that bond yields are going to stay lower for much longer. This might be good news for borrowers, but as Japan showed, persistently low rates do not necessarily invigorate economic growth.

And for long-term investors, such as pension funds and insurers that depend on a certain return from fixed-income instruments, low rates can present a lot of difficulties.

It is particularly problematic for “defined benefit” pension schemes, for example, which calculate the value of their long-term liabilities using high-grade average bond yields. When yields fall, pension providers’ expected returns dim, their funding status deteriorates and they have to set aside more money.

The pension deficit of companies in the S&P 1500 index rose by $14bn in July to $322bn largely because of falling bond yields, according to Mercer. In the UK it rose £2bn to £51bn for FTSE 350 companies. And that was even before August’s big tumbles in bond yields.

Nor is the prospect of Japanification an appetising one for investments outside the bond market, notes John Normand, a senior strategist at JPMorgan.

“The prospect of broader, sustainable Japanisation when growth, inflation and bond yields are already depressed shouldn't comfort anyone,” he said. “When Japanisation is shorthand for an anaemic business cycle, credit and equity investors should question the earnings outlook, recalling that Japanese equities underperformed bonds for most of the country's ‘lost decade’.”

0 comments:

Publicar un comentario