by: The Heisenberg

Summary

- Thanks to a seizure in funding markets, many desks were forced to reassess their expectations for the September FOMC meeting at the last minute.

- The only thing that mattered on Wednesday was what Jerome Powell said about the squeeze and how the Fed planned to address it.

- He was characteristically unconvincing on that score, but did manage to stumble into the "correct" answer when prodded by CNBC's Steve Liesman.

- Forget any other Fed takes you might have read. This is the real story.

You may not know (or even care to know) the specifics, but most investors are probably aware of the fact that funding markets suffered something of a seizure earlier this week.

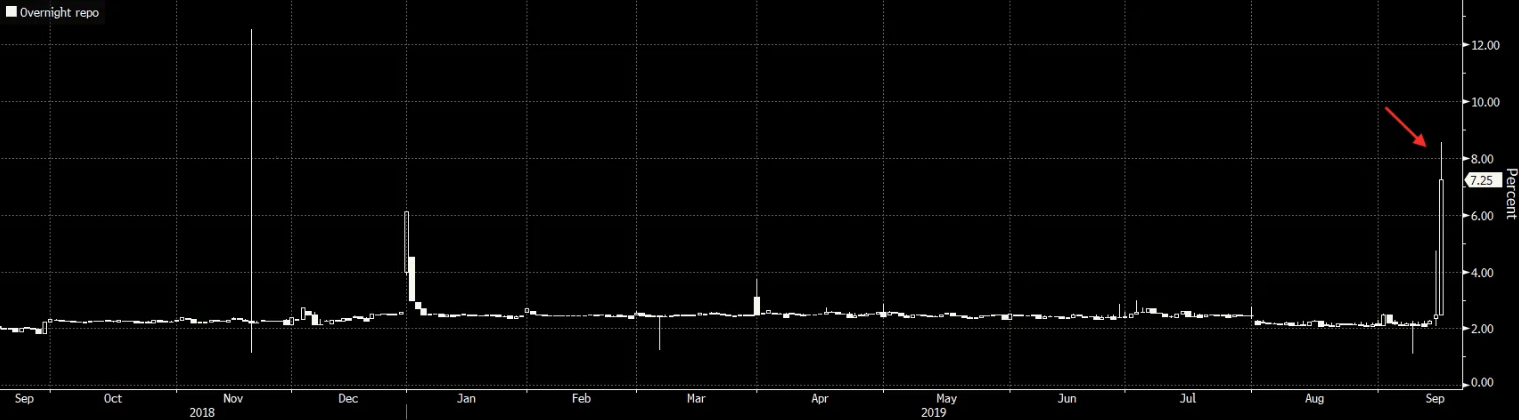

The squeeze, which saw GC repo surge (visual below), was attributable to the collision of structural/legacy issues (e.g., Fed balance sheet runoff, Treasury supply to finance the deficit and bloated dealer balance sheets), and idiosyncratic factors (e.g., corporate tax payments, coupon settlements and last week's bond rout, the worst since the election).

(Bloomberg)

(Bloomberg)

The New York Fed was forced to intervene on Tuesday for the first time in a decade, after the effective funds rate was dragged through the upper end of the target range. The visual below, for those who still haven't come to terms with what happened, represents the Fed quite literally losing control of rates - albeit temporarily.

.

(Heisenberg)

(Heisenberg)

On Thursday morning, the New York Fed injected liquidity for a third consecutive day.

As I was writing this post, they announced they'd conduct a fourth operation on Friday.

The insanity (and it truly was chaotic, as detailed in Bloomberg's dramatic retelling) forced Wall Street to reassess their expectations for the September FOMC meeting at the last minute.

For the uninitiated, this can be an intimidating subject, but stick with me, because this is important - I'll keep it as brief as posible.

On Tuesday, some desks suggested the Fed might be compelled to announce its intention to expand the balance sheet imminently and/or launch a long-rumored standing repo facility.

Some high profile names got in on the act. Jeff Gundlach, for instance, said in a webcast (and also in an interview with Reuters) that the Fed would launch "QE-Lite" "pretty soon" to address the pressures that contributed to this week's funding squeeze.

The idiosyncratic factors cited above notwithstanding, the overarching issue is reserve scarcity.

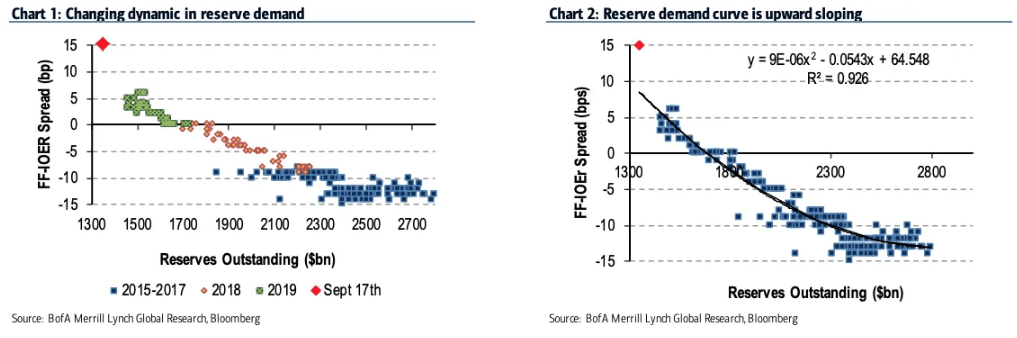

BofA's Mark Cabana has been one of the most persistent voices in documenting this in near real-time over the past several months. There are people who will take you as far down into the "plumbing" as you want to go (with Zoltan Pozsar being perhaps the best example), but Cabana's cadence is relatively user-friendly as this discussion goes.

"The increase in funding pressure as reserves declined to ~$1.35tn likely suggests that the market is on the upward sloping part of the reserve demand curve, below the minimum amount of reserves needed for an ‘abundant reserve regime'," he wrote on Monday evening, as it became apparent that this week would be all about the funding squeeze. Here are two key visuals (note the X-axis is the FF-IOER spread, which you can put in the context of the second chart above):

(BofA)

(BofA)

Here is Goldman saying the same thing in a Wednesday note out prior to the Fed decision:

Until last week the relationship between FF-IOER and aggregate reserves largely seemed to track the curve imputed from the Fed’s Senior Financial Officer Survey, which suggested a substantial buffer (i.e., the “steep” part of the curve was probably at reserve levels below $1.2tn). However, at current levels of aggregate reserves (which we estimate had dropped to about $1.34tn this week), the realized FF-IOER spread, at 15bp on Monday and 20bp on Tuesday, is nearly 7bp to 12bp above where we would have anticipated it to be based on the survey.

That is what CNBC's Steve Liesman was referring to in the press conference on Wednesday when he asked Jerome Powell if the Fed might have "underestimated the amount of reserves necessary for the banking system." Powell's response was lengthy, but here's the abridged version:

We try to assess what that is. We’ve tried to combine that all together, we’ve put it out so the public can react to it. But yes, there’s real uncertainty and it’s certainly possible that we will need to resume the organic growth of the balance sheet earlier than we thought. That’s always been a possibility and it certainly is now. Again, we’ll be looking at this carefully in coming days and taking it up at the next meeting.

Powell's remarks amounted to an acknowledgement that the Fed will need to expand the balance sheet imminently, but the nuance (i.e., the "organic" bit) is crucial and I'll get to that below.

As far as the amount goes, BofA's Cabana on Tuesday estimated that the Fed probably needs to buy $250bn in assets in the secondary market in order to get back to an "abundant" reserve regime with a buffer. Going forward, the Fed would need to persist in outright purchases of around $150bn/year to maintain that level. That gives you an idea of the scope.

It's not a coincidence that stocks turned around as Powell discussed this during the press conference. And indeed, Nomura's Charlie McElligott suggested ahead of time that because the nuance around this isn't well understand, many market participants would rely on "muscle memory" conditioned over the post-crisis years to buy on any headlines around balance sheet expansion. "If we get a 'Fed balance sheet expansion' headline, the equities market risks an overly-bullish interpretation," he wrote, in a Wednesday morning note.

Although we did not, in fact, get an announcement of balance sheet expansion, Powell's discussion during the press conference was seen as confirmation that it's coming, and probably son.

And yet, it's crucial that investors understand that this isn't really "QE", per se. One commenter elsewhere claimed that Powell had left "QE Easter eggs" in his remarks at the presser. That is indicative of the general investing public not understanding the dynamic.

Here's McElligott again (from a Thursday note):

The danger near-term however is that so many in markets equate “balance sheet expansion” to a resumption of “outright QE” and LSAPs…despite a much more nuanced “organic growth” / “QE-Lite” message from Chair Powell at this juncture to “offset +” further Reserve depletion—thus a risk of a near-term bullish sentiment overshoot surrounding this misnomer of “balance sheet expansion = QE.

So, again, you have to understand this in the context of this week's funding squeeze which itself has to be couched in terms of reserve scarcity and an apparent miscalculation of what level of reserves count as "ample."

The September FOMC statement and the dots betrayed a divided committee. Frankly, it doesn't even make sense to speak of "forward guidance" when it comes to the Powell Fed. One is lucky to be able to divine anything about what went into this meeting's decision, let alone what's coming next. The dissents (Rosengren and George in favor of staying on hold, Bullard in favor of a larger cut) don't help.

But really, that was beside the point on Wednesday. What mattered was that the Fed definitively address the funding squeeze or, barring the announcement of balance sheet expansion or a standing repo facility, that Powell demonstrate during the press conference that he takes the situation seriously.

Instead, we got another IOER tweak, the promise of ad hoc, "as needed" liquidity injections (i.e., the operations the New York Fed conducted on Tuesday, Wednesday, Thursday and will conduct on Friday) and remarks from Powell that were anything but forceful.

The IOER tweak and the overnight repo operations are Band-Aids, almost by definition. They buy time, that's all. To address the issue sustainably requires balance sheet expansion, one way or another.

As far as Powell goes, here is another excerpt from his response to Liesman (you can watch the exchange here):

Of course, we were well aware of the tax payments and also of the settlement of the large bond purchases. And we were very much waiting for that. But we didn’t expect … The response to that was stronger than we expected. And by the way, our sense is that it surprised market participants a lot too. I mean, people were writing about this and publishing stories about it weeks ago. It wasn’t a surprise, but it was a stronger response than, certainly than we expected. So, no, I’m not concerned about that, to answer your question.

He elaborated further, but his response was wholly insufficient in my judgement, and I'm hardly alone in that assessment.

Irrespective of whether you think Powell managed to come out unscathed thanks to the reference to balance sheet expansion (and, again, equities' response to that was likely a reflection of market participants not fully understanding the situation) please note that if you read any account of Wednesday's press conference that suggests the Fed chair threaded any needles or otherwise navigated these choppy waters deftly, those accounts are not accurate.

Here, for instance, is what TD rates strategist Priya Misra said as Powell spoke (this was carried on the Bloomberg terminal):

This is disappointing. He is not addressing the structural issues at all. He is not acknowledging the reserve scarcity point and in fact says that we are operating at an ample reserve regime. I expect repo vol to stay high and then rise again at quarter end and year end.

Not every account was as critical as that one, but the fact is, there were no needles threaded on Wednesday. There was just Powell stumbling his way through another somewhat painful press conference, dodging questions when the going got tough and coming across as insufficiently concerned about the only thing that really mattered this week - the funding squeeze.

All of that said, you should also be wary of accounts that suggest this week's turmoil in funding markets represents some kind of 2008-style freeze-up. That isn't the case for a variety of reasons.

Here's a simple assessment from a much longer Credit Suisse note:

What we have seen this week is not a crisis but a symptom that we have reentered an old regime for Fed policy operations. To answer the question, is the Fed losing control, we say no it isn’t, but it must now move to allowing its balance sheet to grow in order to maintain its interest rate target.

And therein lies the problem. What the market got on Wednesday was an IOER tweak and a promise of ad hoc liquidity injections in perpetuity. They're putting duct tape over an earthquake fissure.

That characterization isn't meant to suggest that temporary measures can't close the fissure for a spell, or that the fissure is going to widen out and swallow us all. Rather, it's just to say that the issue at the heart of this week's funding squeeze wasn't addressed in a sustainable way at the September Fed meeting.

Going forward, the important thing will be for the Fed to communicate effectively ahead of the inevitable announcement of balance sheet expansión.

This is a subject that is poorly understood by most, and understood down to the granular details by a relative handful of rates strategists and those active in money markets. That means the Fed is walking a (very) fine line between educating the 99% of people who don't understand (so as to avoid accidentally creating the impression that "QE 4" is about to be launched), and convincing the 1% of people who do understand that the Fed isn't asleep at the wheel and appreciates the urgency of addressing reserve scarcity.

I wish them the best of luck in that endeavor and I wish you the best of luck in re-reading this post from the beginning so that you can be sure you're a well-informed investor.

0 comments:

Publicar un comentario