Monetary authorities are reacting to faltering growth

Steve Johnson

Emerging market central banks have turned more dovish than at any point since at least the global financial crisis, according to analysis of the language in 4,000 monetary policy publications.

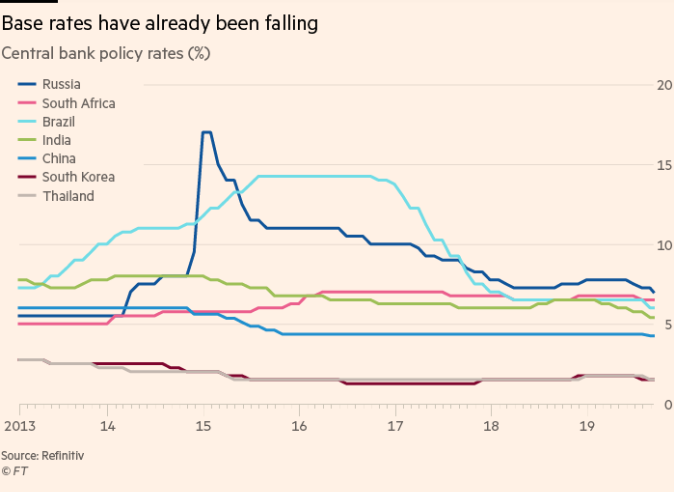

The extreme pro-easing bias is remarkable given that banks, including those of Brazil, Russia, India, China, South Africa and Turkey, have already cut rates this year, suggesting the scope for further policy loosening should be narrowing.

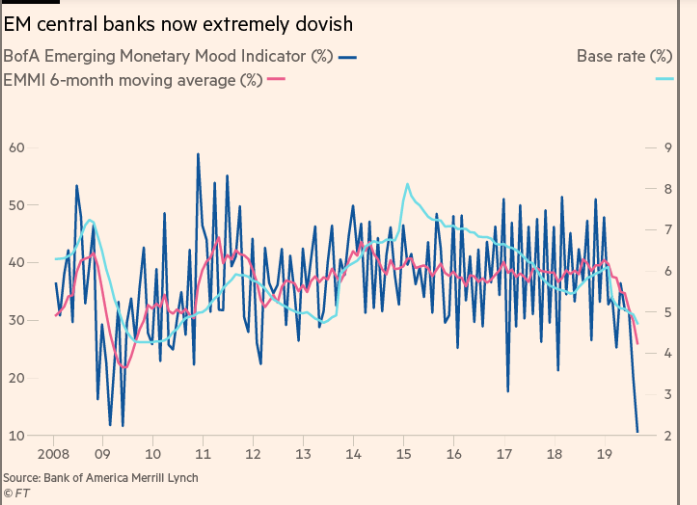

Bank of America Merrill Lynch’s Emerging Monetary Mood Indicator, based on robotic scanning of keywords used in the publications of 11 big EM central banks, is at its more dovish extreme since the height of the crisis in 2009, based on a six-month moving average.

Based on single-month figures, the August reading — the latest available — was the most extreme since the depths of the dotcom crash in 2000.

“There are quite a few emerging markets where we are comfortable saying we think [central banks] will cut more than the market is expecting,” said David Hauner, head of EM cross-asset strategy and economics at BofA, who cited Russia, Brazil, China and the Czech Republic as examples.

“We don’t think the market is aggressively pricing in rate cuts. There is plenty of firepower out there. Real rates in emerging markets are still quite high,” he added.

Turkey has led the way among big EM central banks this year, slashing base rates by 750 basis points to 16.5 per cent, while India has cut by 110bp to 5.4 per cent. Since the start of 2017, Brazil has eased by 775bp to 6 per cent and Russia by 300bp to 7 per cent.

Monetary authorities are reacting to faltering growth, with the IMF forecasting that EM-wide growth will slow to a post-global financial crisis low of 4.1 per cent this year.

Tame inflation (outside of Turkey and Argentina) has given central banks headroom to ease. Mr Hauner said many countries “have got rid of the current account deficits that have constrained policy in the past, so they have more room to cut without their currencies exploding”. He argued the extreme dovishness should be supportive for EM equities and bonds, but be a potential drag on currencies.

0 comments:

Publicar un comentario