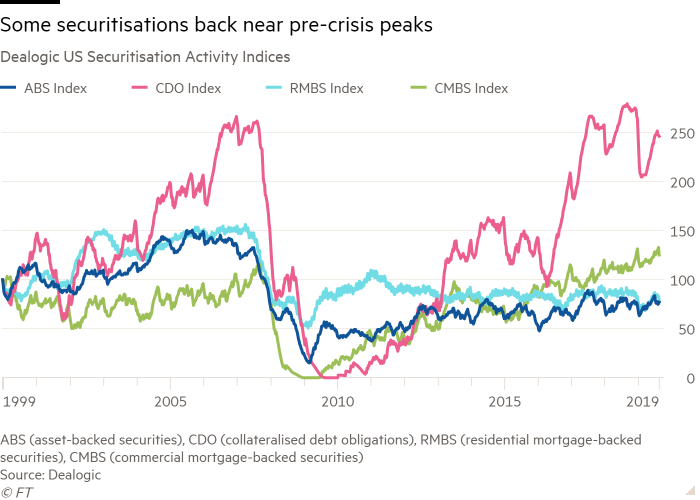

Commercial mortgage securities have bounced back — unlike the residential equivalent

Laurence Fletcher in London

Parts of Wall Street’s debt securitisation engine are back running at levels not seen since the pre-financial crisis boom.

Data group Dealogic’s indices of US securitisation activity show that issuance of collateralised debt obligations — structured products made up of bundles of bonds and loans — rose above its pre-crisis peak late last year and is currently back close to those levels this year.

The market for commercial mortgage-backed securities has also rebounded strongly since late 2008 and early 2009, when issuance completely seized up in the aftermath of the financial crisis. Activity in the asset class is now some way above its 2007 high.

In contrast, the data show little sign of a significant re-emergence of issuance of residential mortgage-backed securities — packages of US mortgages seen as helping precipitate the financial crisis — or asset-backed securities, both of which are fairly flat compared with 2008.

The data are based on the value of primary market transactions, the number of deals and their share relative to overall debt capital market issuance, equally weighted to form an index.

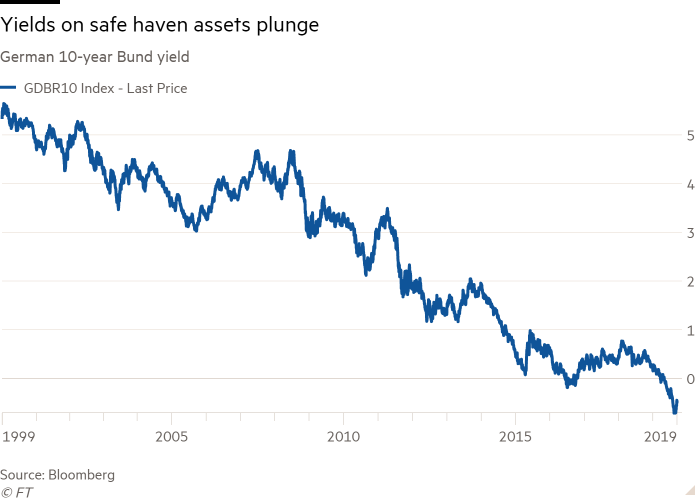

Tumbling yields on many traditional “safe haven” bonds to ultra-low or negative levels — supported by the European Central Bank’s renewed bond-buying programme announced last week — has forced income-hungry investors into other, riskier assets.

That has helped fuel a resurgence in some areas of securitisation, which involves packaging underlying debt instruments and selling it on to investors. But it has also raised questions as to whether some areas have become overinflated and could pose another threat to financial stability, if prices in the underlying markets start to fall.

As Dealogic’s global head of data science, Paul Sykes, puts it: “Are we in a world where lots of securitisation is fine, or is it a precursor to something worse?”

0 comments:

Publicar un comentario