Tepid results from multinationals don’t necessarily signal trouble at home

By Justin Lahart

The domestic economy is still solid, but the Federal Reserve’s beige book survey showed manufacturers continuing to worry about the uncertainty and costs associated with trade disputes. Photo: tim aeppel/Reuters

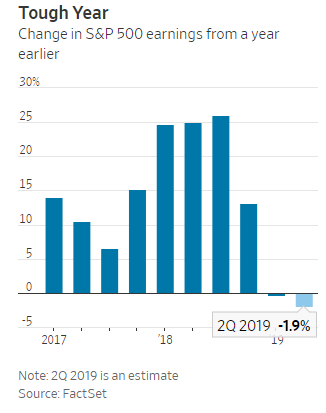

American companies are reporting second-quarter results, and the numbers so far have been nothing to write home about. Based on current estimates compiled by FactSet, earnings for companies in the S&P 500 will be down 1.9% from a year earlier. Actual results probably will be somewhat better given companies’ tendency to lower the bar and then clear it, but the final figures are unlikely to fit anyone’s definition of good.

It is tempting to hang earnings weakness on the domestic economy. Even though growth has moderated a bit, it is still solid. Macroeconomic Advisers estimates imply that final sales to domestic purchasers—a measure of underlying economic demand—was up 2.6% from a year earlier in the second quarter. That compares with a 2.9% gain in the second quarter of last year.

Outside the U.S., things aren’t looking so rosy, and that is a problem for many of the companies in the S&P 500, which conduct a substantial share of their business overseas. Paint maker PPG Industries ,for example, which generated more than half of its income outside the U.S. last year, highlighted weakness in the Chinese and European auto markets when it reported a 2.6% decline in second-quarter sales. The strength of the dollar compounds the problem: Industrial-equipment maker Dover said foreign exchange created a 2.6% headwind to sales.

Tariffs and trade tensions are another point of stress, particularly in the manufacturing sector.

The Federal Reserve’s beige book survey released Wednesday—a report of anecdotes drawn anonymously from business contacts around the country—showed manufacturers continuing to worry about the uncertainty and costs associated with the various trade disputes into which the U.S. has entered.

But trade counts as more of an issue for large public companies than for U.S. businesses at large. That isn’t just because of all the business they do overseas but also the kinds of companies they are. Some 190 of the 500 companies in the S&P 500—more than a third—are classified as manufacturers. Yet manufacturing jobs count for only 8% of U.S. employment.

Finally, companies are being confronted by rising labor costs and an inability to pass those costs on. It is part of why profit margins look to have slipped in the second quarter. But for most Americans, the combination of rising wage growth and low inflation probably counts as a good thing.

It is easy—and often makes sense—to view big U.S. companies as a barometer of the U.S. economy, but that is misleading at the moment. A measure of something isn’t the same as the thing itself.

0 comments:

Publicar un comentario