Why Markets Have Been A Tinderbox In August

by: The Heisenberg

Summary

- New estimates show that most of the manic moves in stocks and bonds this month can be explained by many of the self-feeding loops I've spent years discussing.

- In rates, the recent plunge in yields was mostly down to convexity hedging.

- In stocks, gamma hedging and CTA de-leveraging played a prominent role last week.

- And it's all exacerbated by disappearing liquidity.

- In rates, the recent plunge in yields was mostly down to convexity hedging.

- In stocks, gamma hedging and CTA de-leveraging played a prominent role last week.

- And it's all exacerbated by disappearing liquidity.

If you're looking to assign blame for the manic market moves that have, through Monday anyway, defined the month of August, you can point to systematic flows and technically-driven price action.

I've discussed this at length here and elsewhere over the past two weeks, effectively documenting it in real time, but I think it's worth fleshing out a bit further for the audience here in the interest of perhaps shedding a bit more light on something that still isn't well understood by retail investors.

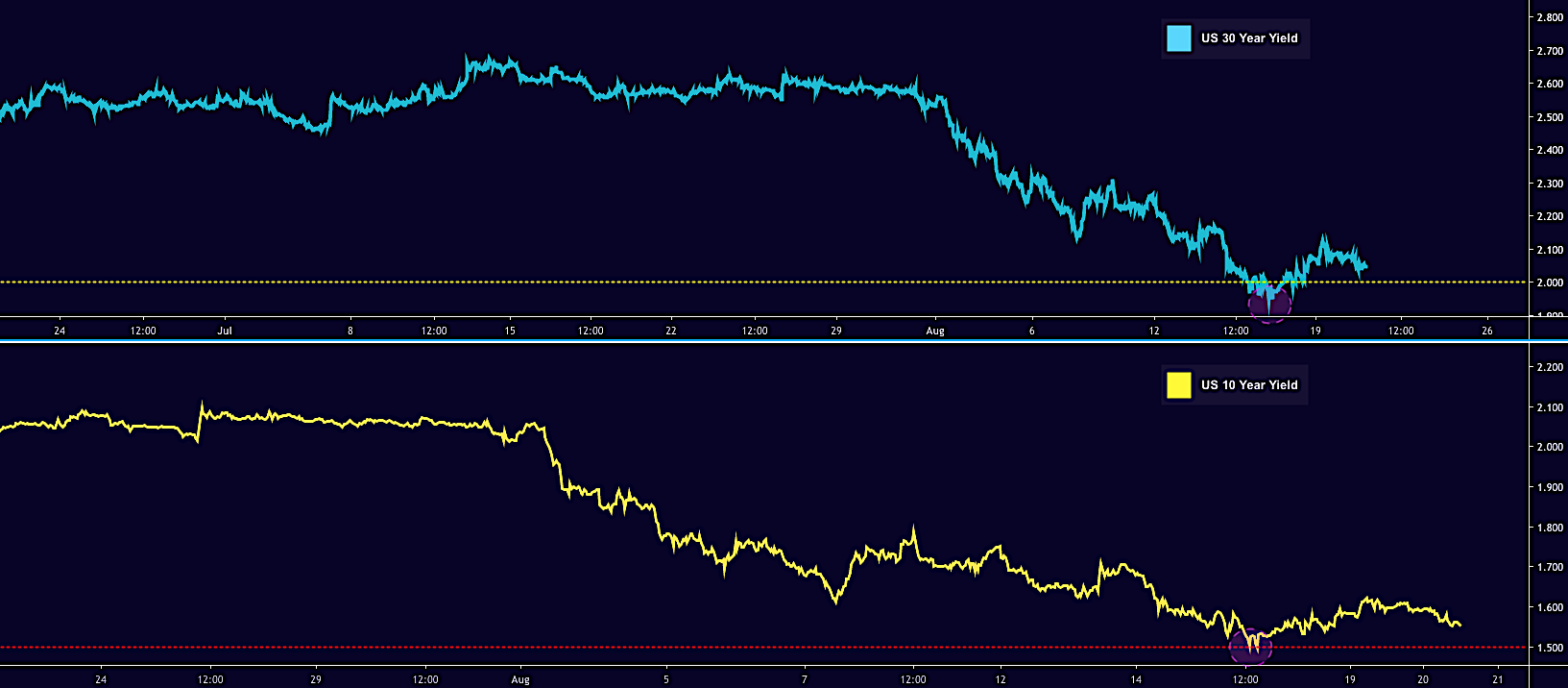

Starting in rates, I talked quite a bit in a Friday post for this platform about receiving flows and convexity hedging and the extent to which that had almost certainly played an outsized role in the frantic rally at the long-end of the US curve. 10-year yields fell below 1.50% and 30-year yields below 2.00% at the height of the rally last week.

(Heisenberg)

(Heisenberg)

We've seen the bottom fall out for yields on several occasions in 2019 and while some of that is down to growth concerns, collapsing inflation expectations, a flight-to-safety and the assumption of lower rates, a large percentage of this month's downdraft in yields is attributable to mortgage investors and banks chasing the rally.

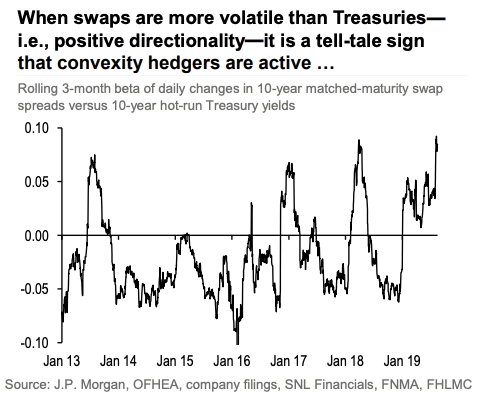

That sprint created some $500 billion in demand, according to JPMorgan, whose rates strategists on Tuesday reminded clients that these flows are easy to see. "[It's] clear from the behavior of derivatives markets, since most of these hedging flows occur in interest rate swaps," the bank noted.

(JPMorgan)

(JPMorgan)

As I wrote Friday on this platform, this sets in motion a self-fulfilling prophecy. The lower long-end yields go, the more convinced market participants become that everyone else is panicking about the outlook for global growth. Those jitters beget still more demand for duration, which pushes yields even lower, forcing more hedging, and around we go.

And then there's the psychological impact on equities. The exaggerated moves in rates described above are part of the reason the 2s10s inverted. That inversion, in turn, dealt a grievous blow to investor psychology last Wednesday, when the Dow suffered its worst one-day drop of 2019.

This is a maddeningly circular and exceptionally precarious dynamic. When fundamental, discretionary investors sell on recession jitters tied to what, as noted above, was an exaggerated move in the bond market, that can push equity benchmarks through key levels, which starts tipping dominoes for systematic deleveraging by the likes of CTAs.

JPMorgan's Marko Kolanovic underscored all of this in a note out Tuesday morning. "This is an important data point for equity investors, as moves in rates (e.g. yield curve inversion) significantly impact investment sentiment”, he wrote, on the way to quantifying how much selling in and around last Wednesday's rout was attributable to programmatic/systematic strats. That figure, according to Marko, was roughly $75 billion, with 20% of it coming from CTAs.

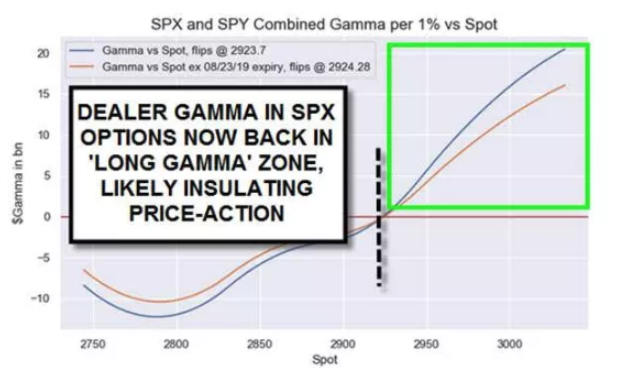

Now, recall how, on August 11, I mentioned in a post for this platform that dealers' gamma positioning likely flipped negative after the FOMC, which meant that selling would beget more selling. Kolanovic on Tuesday underscored that assessment, noting that heading into last week, dealers' gamma positioning betrayed "a sizable short".

Try to appreciate how the dominoes fall. As yields move lower on what are, initially, fundamental concerns, convexity hedging flows turbocharge the bond rally. That has the potential to create a false optic, or to magnify recession concerns (I referred to it as a "Fata Morgana" earlier this year). Last week, that manifested itself in the inversion of the 2s10s, which led to selling in equities. Once stocks fell through key levels, it activated CTA de-leveraging and because dealers' gamma positioning was negative, their hedging exacerbated the situation.

Kolanovic on Tuesday said some 50% of the above-mentioned $75 billion in programmatic selling during or as a result of the August 14 selloff was attributable to index option delta and gamma hedging, which he calls "the single most important driver of price action during both the selloffs and rallies last week".

Mercifully, that positioning is back to neutral now, something Nomura's Charlie McElligott illustrated on Monday as follows:

(Nomura)

That, folks, is how modern markets can turn into tinderboxes.

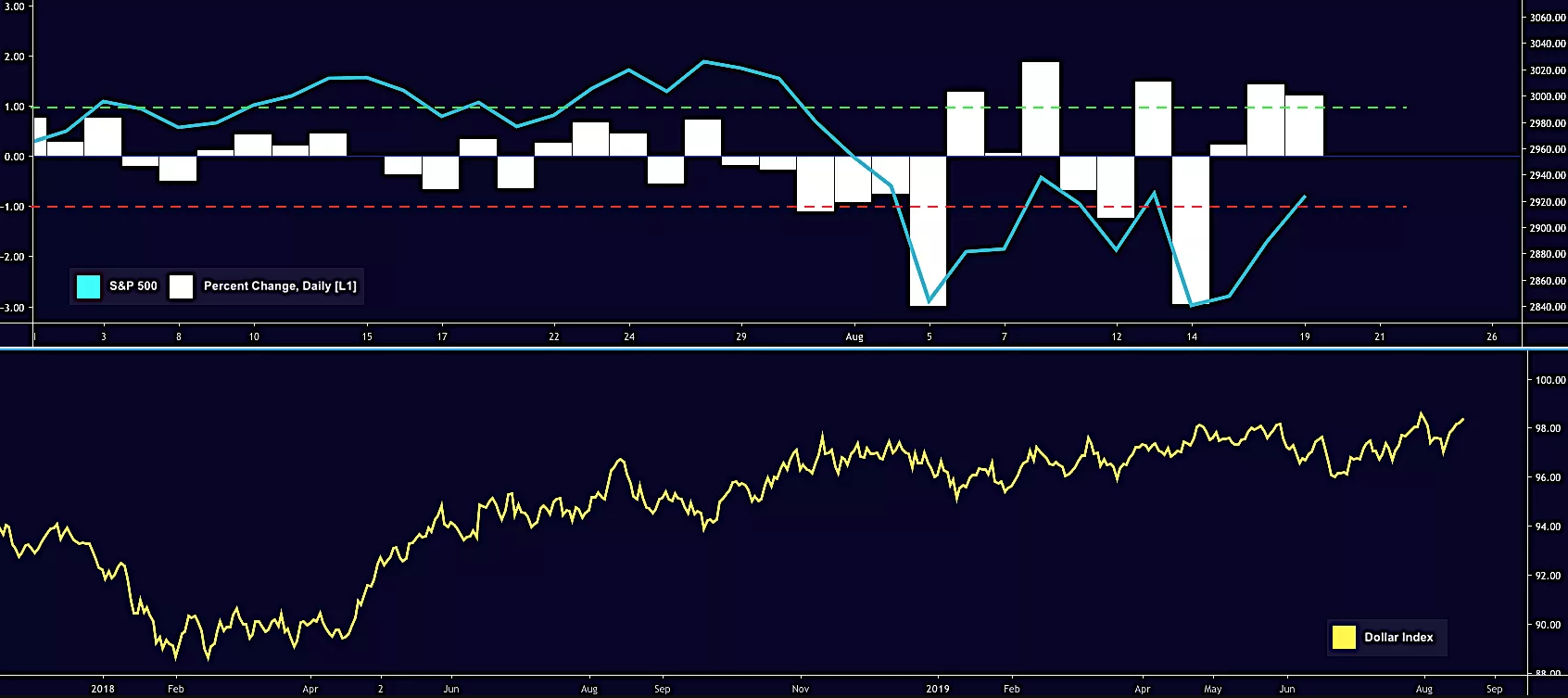

If you're looking to explain why nine of the 14 sessions since the July FOMC have seen S&P moves of 1% or more (top pane in the figure), that's why.

(Heisenberg)

(Heisenberg)

This is exacerbated materially by low liquidity. These flows are hitting during a month when liquidity is seasonally sparse, but this August has been particularly dry. More broadly, liquidity in S&P futures simply never recovered after the February 2018 vol. event.

(Deutsche Bank)

(Deutsche Bank)

That's attributable to a variety of factors, but one of the issues is that HFT liquidity provision is volatility-dependent. That is, algos pull back when volatility rises.

Well, needless to say, the interaction of all the dynamics mentioned above has a tendency to push up volatility. If vol. spikes prompt HFTs to reduce liquidity provision, it can make a bad situation immeasurably worse. That goes for bonds too. As JPMorgan pointed out again on Tuesday, "fast market participants represent roughly 80% of the liquidity provision in the hot-run interdealer Treasury market."

Going forward, positioning has once again been washed out a bit, with hedge fund betas very low, for instance. As noted above, dealers' gamma positioning is (basically) neutral now, so that should serve to help tamp down volatility.

But, it is by no means clear that the impact of hedging flows in rates is behind us, and on top of that, the dollar is near YTD highs. Jerome Powell has the potential to exacerbate both the decline in bond yields and dollar strength on Friday if he doesn't strike the "right" tone in Jackson Hole.

Suffice to Boston Fed chief Eric Rosengren did not signal a willingness to back off his propensity to dissent against more rate cuts when he spoke to Bloomberg on Monday.

And President Trump did not signal a willingness to step back from his insistence on those same cuts when he spoke to Twitter.

0 comments:

Publicar un comentario