Powell, Tariffs And Trump: A Friday Tragicomedy

by: The Heisenberg

Summary

- On Friday morning, China retaliated against forthcoming tariffs from the Trump administration, throwing equities and risk assets for a loop.

- Jerome Powell's Jackson Hole speech was acceptable, and briefly stabilized things.

- Then, President Trump weighed in on Twitter, chancing a conflagration in "tinderbox" markets.

Here's a quick take, including a brief recap of why this is a dangerous setup.

- Jerome Powell's Jackson Hole speech was acceptable, and briefly stabilized things.

- Then, President Trump weighed in on Twitter, chancing a conflagration in "tinderbox" markets.

Here's a quick take, including a brief recap of why this is a dangerous setup.

On Thursday afternoon, in a somewhat cautious post for this platform, I gently suggested that one of the major risks headed into Jerome Powell's closely-watched speech at Jackson Hole was that the Fed Chair wouldn't come across as dovish enough to satisfy President Trump, setting the stage for a scenario in which the White House refuses to accept the implicit pushback, instead opting to escalate the trade war further in a bid to test Powell's mettle.

As I write these lines, we're still hours away from the closing bell on Wall Street, but it's been an eventful day. China announced retaliatory tariffs on $75 billion in US goods, including new 5% levies on soybeans and oil from September 1, and the reinstatement of 25% duties on autos starting on December 15.

That news sent equity futures tumbling, but fortunately, Powell's Jackson Hole speech was replete with references to the darkening global growth outlook and allusions to geopolitical turmoil. He specifically mentioned weakness in the data out of China and the worsening situation in Germany, and he checked all the boxes when it comes to letting the market know he's apprised of the potential for political frictions to boil over, with negative ramifications for investors. To wit, from the speech:

We have seen further evidence of a global slowdown, notably in Germany and China. Geopolitical events have been much in the news, including the growing possibility of a hard Brexit, rising tensions in Hong Kong, and the dissolution of the Italian government.

Crucially, Powell said the Fed's "assessment of the implications of these developments" will inform the effort to sustain the expansion. Although not overtly "dovish", per se, that was most assuredly a sign that the Fed will assign a heavier weight than they otherwise might to international developments when deciding how best to ensure that the longest US expansion on record gets even longer.

US equities (and risk assets in general) recovered most of their morning swoon as traders digested Powell's remarks.

And then the president started tweeting. I don't think I have to quote directly from Trump's tweets (nor do I want to), but suffice to say he took his irritation with China's retaliatory measures out on Powell, who he explicitly called an "enemy" on par with "Chairman Xi". The President also said he would "respond" soon to China's retaliatory tariffs.

Irrespective of what form that response ends up taking, the fact of the matter is that Powell delivered what could reasonably be expected of him, especially in light of the hawkish setup from regional Fed presidents as discussed in the linked post above.

That is, there was every indication that Powell's remarks in Jackson Hole would lean overtly hawkish, betraying a desire for the Fed to stick to the "mid-cycle adjustment" script, but instead, we got a Fed chair who emphasized the myriad international developments weighing on growth and investor sentiment. That market-friendly lean was reflected in the bounce off the morning lows.

That is, there was every indication that Powell's remarks in Jackson Hole would lean overtly hawkish, betraying a desire for the Fed to stick to the "mid-cycle adjustment" script, but instead, we got a Fed chair who emphasized the myriad international developments weighing on growth and investor sentiment. That market-friendly lean was reflected in the bounce off the morning lows.

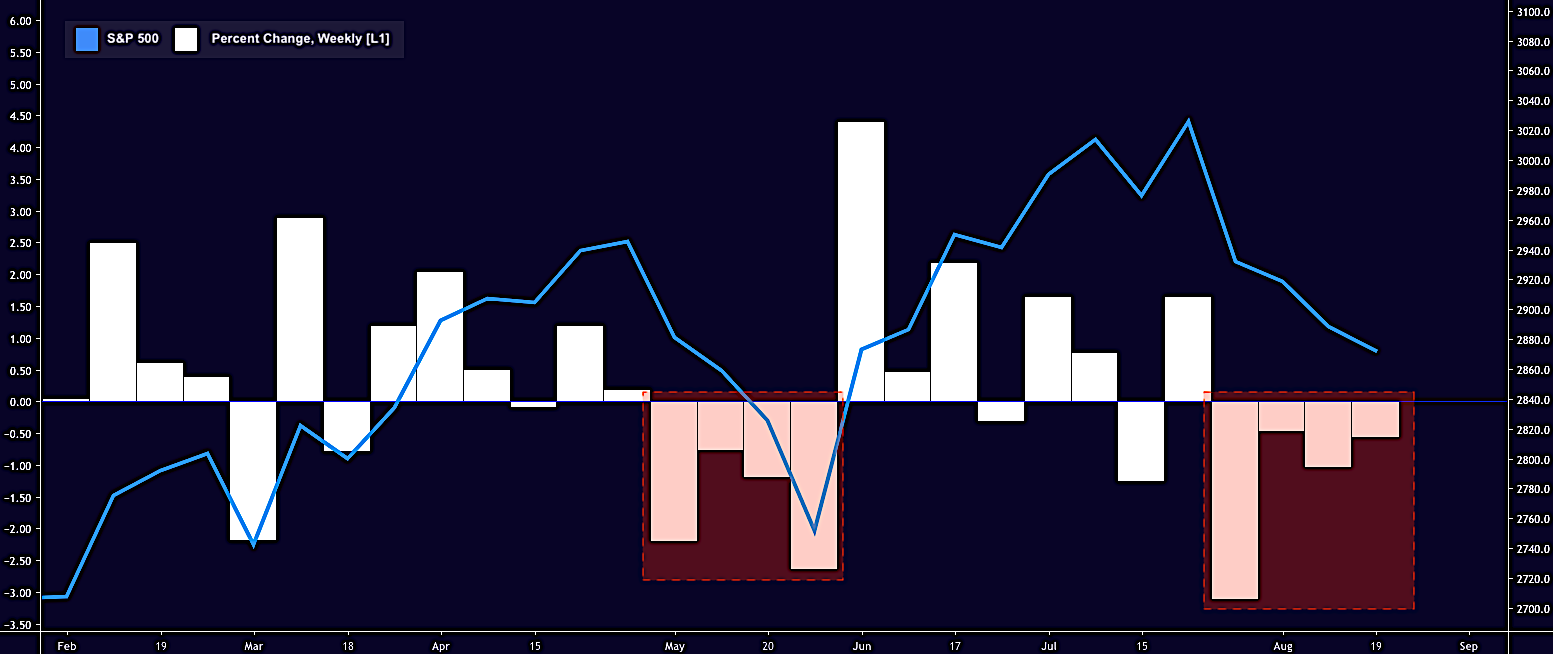

Have a look at this chart:

(Heisenberg)

(Heisenberg)

Powell did his job. He stabilized both equities and the yuan. Trump wanted more, although as I noted elsewhere, it's not entirely clear what the President expected. It's not as though Powell could re-write his speech an hour ahead of the public release and he certainly can't just cut rates from the podium in Wyoming.

In any event, that chart says it all, and the only saving grace as of lunchtime on Friday in New York is that the curve bull steepened a bit as the market still seems to think that trade escalations will be enough to force a Fed relent, especially in light of Powell's internationally-focused comments.

The dollar came off pretty sharply as well, and all else equal, that's a positive development for risk assets, but right now it doesn't matter - markets are spooked.

Barring a turnaround (which is possible depending on what the President says later), this will be the fourth consecutive week of losses for US equities. The last time that happened was, of course, in May, when Trump's decision to break the Buenos Aires trade truce threw stocks for a loop after Powell engineered a mammoth four-month rally.

(Heisenberg)

(Heisenberg)

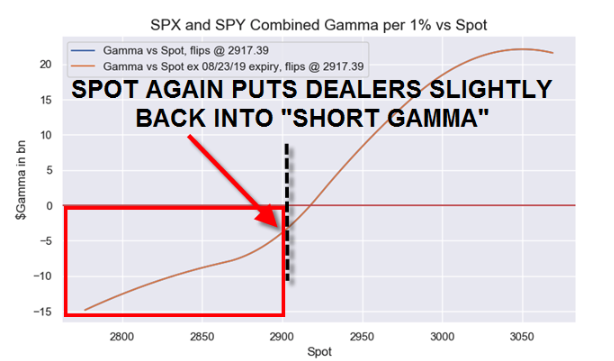

Far be it from me to question the White House's trade policies, but I would suggest that the administration is wading into dangerous waters with markets. As Nomura's Charlie McElligott wrote on Friday morning, we'll be dealing with "still-weak post-summer holiday volumes [and] depth of book" along with "tight liquidity and VaR constraints from dealers" for weeks to come. Market depth has dried up in both rates and equities at various intervals in August, exacerbating the price action.

Dealers' gamma profile now looks to have flipped negative again (see visual below) and on some models, we're back near de-leveraging levels for some trend-following strats.

(Nomura)

(Nomura)

If the White House doesn't exercise some restraint, we good see equities careen through key levels and strikes, triggering systematic flows (both from trend-follower de-leveraging and dealer hedging) into a thin, August market.

At the same time, any further rally in bonds could bring more hedging flow, catalyzing another forced duration grab, which could push long-end yields even lower, sending a further risk-off signal to the market and, if the short-end can't keep up, inverting the 2s10s again, only this time sustainably.

This is something of a tragicomedy. China's retaliation was expected and, as alluded to above, Powell's speech in Jackson Hole was generally fine. Friday's drama was wholly unnecessary, and entirely dangerous when markets are, as I described them here a few days ago, a "tinderbox."

0 comments:

Publicar un comentario