Why America is learning to love budget deficits

The trend towards looser fiscal policy could mark the biggest shift in economic thinking in a generation

Sam Fleming and Chris Giles in Washington

For a newly elected Democrat, it was an unusual way to make your mark. Ben McAdams, the Democratic representative from Utah, this month introduced an amendment that would make it unconstitutional in normal circumstances for the American government to fail to balance its books.

The proposal, which he says prompted a fierce backlash from within his own party, reflects a fear that both fellow Democrats and Republicans are giving up on any attempt to curb the budget deficit. “Politicians are like water — they will take the course of least resistance,” says the 44-year-old congressman, an ex-mayor of Salt Lake County. “In our case the course of least resistance is deficit spending.”

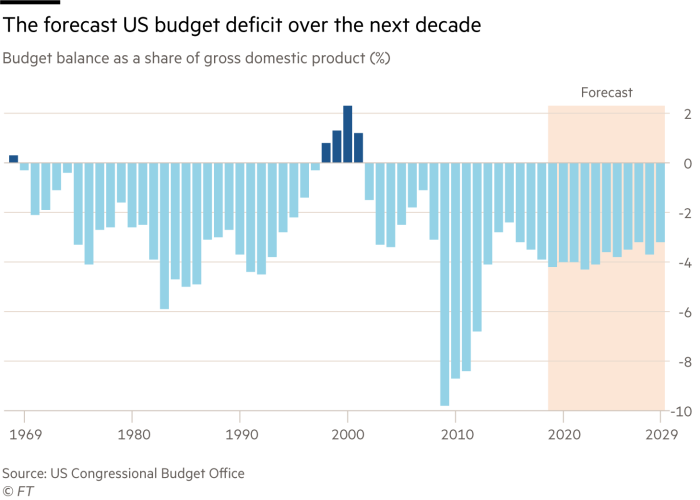

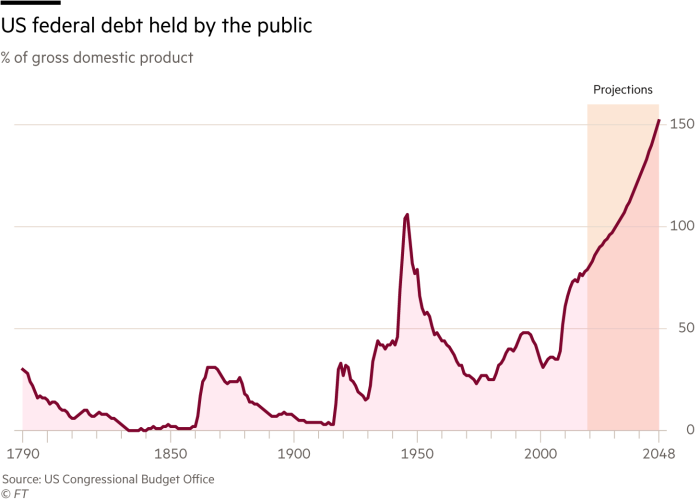

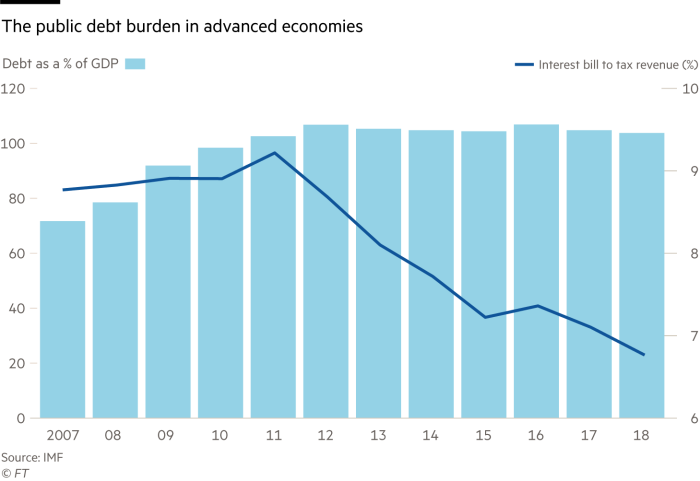

Fiscal conservatism may once have had deep roots within both the Republican and Democratic parties, but today it appears critically endangered. The Congressional Budget Office’s latest outlook suggests deficits are projected to average 4.4 per cent of gross domestic product in 2020-29, far above the average set over the past 50 years of 2.9 per cent of GDP. That will ensure public debt as a share of GDP rises steadily to eventually exceed records set immediately after the second world war.

Symbolically charged amendments such as the one sponsored by Mr McAdams and backed by the Blue Dog coalition of fiscally conservative Democrats have little or no chance of ever becoming law. Instead, they could end up being relics of a bygone era in thinking about the economy.

The trend towards looser fiscal policy led by the US marks potentially the greatest change in economic policymaking for a generation. Persistently low inflation is allowing central banks to keep interest rates down, easing the cost of servicing public debt. As a result, many economists now argue there is little pain and much to gain from further loosening budgetary shackles.

After four decades when central banks have been the dominant actors — first through their efforts to use monetary policy to vanquish inflation and then, over the past decade, to avert disaster following the financial crisis — it is fiscal policy and government spending that have the potential to become bigger driving forces in the economy.

While US politicians continue to publicly deplore deficits, many are in practice embracing them. On the right, President Donald Trump has led his party down a path to a US deficit blowout that will soon take annual budget shortfalls above $1tn. On the left, influential figures such as Alexandria Ocasio-Cortez, the leftwing representative from New York, have suggested that not all spending needs to be offset with extra taxes, as progressives propose major expansions of public health spending and environmentally-friendly investment. Bernie Sanders, one of the early frontrunners to become the Democratic presidential candidate, is advised by Stephanie Kelton, a prominent economist who argues deficits are harmless if twinned with low inflation.

Even in the sometimes lonely middle ground, economists are showing a willingness to embrace deficits. Lawrence Summers and Jason Furman, former advisers to Barack Obama, argued earlier this year that it is time Washington ends its debt obsession and recognises that there had been few if any fiscal crises in countries that borrow in their own currencies and print their own money.

British economist John Maynard Keynes advocated deficit spending during recessions, and when monetary policy has lost its power to stimulate spending © Getty

“The fiscal floodgates are wide open,” says Mark Zandi, chief economist at Moody’s Analytics. “Both the Republicans and the Democrats now have theories that allow them to ignore deficits and debt . . . The whole game has changed.”

Similar stories are playing out elsewhere. Japan has arguably not worried much about budgetary strictures for two decades. In Europe, politicians are beginning to question the old orthodoxy, which required the public finances to be sustainable and prudent while central banks sought to curb economic booms and busts. Germany is under particular pressure to relax its balanced budget policy — the so-called schwarze Null (“black zero”) — and boost its infrastructure.

To politicians, the allure of the new thinking on deficits is obvious if it helps justify popular tax cuts or public spending increases. In the past politicians were wary of the risks associated with lost budgetary credibility — including the threat of surging borrowing costs and higher inflation, or lower growth associated with hefty public debt mountains.

But now a series of developments has triggered a reassessment of fiscal policy, says Mohamed El-Erian, chief economic adviser to Allianz. These, he explains, include persistently low and, in some cases, negative interest rates; the absence of inflationary pressures despite low rates and central bank liquidity injections; a prolonged period of relatively low and insufficiently inclusive growth; and concern that the manner in which central banks conducted quantitative easing disproportionately benefited the rich.

“All this comes in the context of a growing realisation that central banks cannot be the only game in town when it comes to the policy challenge of generating high inclusive growth and genuine financial stability,” he adds.

The US serves as a vivid example of the changing political weather. Mr Trump spoke implausibly during the 2016 campaign about paying off America’s national debt in just eight years, and went on to appoint Mick Mulvaney, a hardline deficit hawk, to be his first White House budget director.

But the president then executed a stunning U-turn on the budget, ruling out reforms to the fundamental drivers of rising public spending — namely social security and pension-age medical expenditures. At the same time his administration embarked on a major tax-reduction programme, taking a leaf from supply-side folklore with claims that the cuts would pay for themselves via higher economic growth.

Trump administration policies are now set to push the US into the deepest protracted budget deficits on record outside wars and recessions — at a time when the US economy is near or at full employment.

Kevin Hassett, chairman of the president’s Council of Economic Advisers, insists the White House does care about the deficit, but that it was right to prioritise tax cuts that it expected to boost growth. “The growth part of the policies is working,” he says in an interview with the FT. “The White House agenda is getting ahead of the curve on spending.”

Stephanie Kelton, an adviser to Bernie Sanders’s 2016 and 2020 presidential campaigns, is a proponent of Modern Monetary Theory © Bloomberg

The Republicans’ relaxed approach to fiscal policy has helped spur a debate within the Democrats — who presided over a fleeting bout of budget surpluses in Bill Clinton’s presidency. As progressives gain influence within the party, some are backing massive and potentially deficit-expanding spending programmes addressing climate change and social policy priorities.

One example is the so-called Green New Deal investing in clean-energy jobs and infrastructure being pushed by Ms Ocasio-Cortez and Ed Markey, the junior Democratic senator from Massachusetts. Another is the “Medicare for all” public health proposals backed by many of the Democratic presidential candidates, including Mr Sanders.

Ro Khanna, a California congressman and leading progressive, insists that the party cannot afford to ignore deficits. But he argues austerity policies in the wake of the financial crisis were a mistake, and that the priority now is to shift away from tax cuts for the most wealthy towards investments in healthcare, education and infrastructure. Early this year he was part of an unsuccessful revolt by progressives against a package of rules in the House of Representatives that require new spending to be offset by savings elsewhere or extra revenue.

“The winning formula for the Democrats is they are going to have to endorse some of these relatively fiscally extreme positions to get nominated,” says one Democratic strategist, speaking of the 2020 presidential contenders. “The threats of debt and deficits have not panned out. We have been running deficits and debt for 30 years and where is the crowding out, the inflation and the soaring interest rates?”

One recent catalyst for the new thinking on easier fiscal policies, overturning seminal papers from the 1980s, which ushered in the pre-eminence of monetary policy and independent central banks, was the January presidential address at the American Economic Association by Olivier Blanchard, former IMF chief economist.

Mr Blanchard argued for fiscal policy to be given greater emphasis now that interest rates appear to be persistently low — and below the annual growth rate of nominal GDP. He turned around the famous argument of Thomas Piketty that inequality would rise because interest rates were higher than growth rates, which increased the power of capital. Instead, Prof Blanchard said the world was shifting toa more normal period where growth rates exceeded long-term, risk-free interest rates.

Backers of defecit-expanding spending programmes argue the priority now is to shift away from tax cuts for the wealthy to investments in healthcare, education and infrastructure © Getty

That meant countries can have higher debt because their ability to service it and eventually repay it becomes ever easier as their economies grow. “The issuance of debt without a later increase in taxes may well be feasible,” Prof Blanchard said.

An allied strand of academic thinking argues that with interest rates stuck at zero or close to zero, monetary policy is largely ineffective and fiscal policy will need to take up the reins of managing demand. Achieving this will be no mean feat in countries like the US, where political gridlock makes it tough to achieve nimble changes in budget policy.

Mario Draghi, president of the European Central Bank, issued a call for more help from governments at the recent IMF spring meetings in Washington. “It’s quite clear our current monetary policy is already very accommodative and can be made even more so if needed. But we reach a point where fiscal policy becomes more and more important,” he said.

As such, many economists complain that budgetary policies from institutions such as the European Commission are unduly harsh. Robin Brooks, chief economist of the Institute of International Finance, says it is “unsustainable” that a major economy like Italy is in quasi-permanent stagnation, adding that on the eurozone periphery there has been a “huge over-tightening [of fiscal policy]”. Italy’s populist new government has taken this argument to Brussels in its battle with the commission.

Bernie Sanders, an early frontrunner for Democratic presidential candidate, backs economists who argue deficits are harmless if twinned with low inflation © AFP

At the extreme end of the rethink is so-called Modern Monetary Theory, which argues that policymakers in countries that print their own currency can take on as much debt as is necessary to keep the economy purring away at full employment. These arguments, propounded by the likes of Prof Kelton, an adviser to Mr Sanders’s presidential 2016 and 2020 campaigns, go beyond standard Keynesian orthodoxy, which advocates deficit spending during recessions and when monetary policy has lost its power to stimulate spending.

Instead, MMT advocates say that in normal times governments do not need to counter every spending decision with either higher tax or an expenditure cut elsewhere. Inflation, if it becomes a menace, can be offset by higher taxes to counter excess government-created liquidity.

Prof Kelton complains that politicians in the US are accustomed to going to the Congressional Budget Office with spending proposals to see if it judges that their numbers balance up. “Now is not the time to wait around for permission slips to [take] action on climate change,” she tells the FT. “We are not going to tie our shoes and complain we can’t run.”

Those advocating budgetary prudence have by no means thrown in the towel. In a recent lecture to central bankers in Washington, Kenneth Rogoff of Harvard University questioned the assumption that interest rates and inflation would stay low for a long time, making public debt much less expensive and a MMT policy almost free to finance.

“It is probably true — you can have much more debt — interest rates are low. But in MMT, the debt is all very, very short term, so [the debt] is cheap, but it’s risky,” he said. “It’s very cheap until it’s not.”

Professor Francesco Giavazzi of Bocconi University in Milan, Italy, argues that keeping a tight rein on budget deficits is necessary and does not harm economic performance if tax rates are kept low. “Austerity policies have been effective where implemented mostly by cutting expenditures,” he says, citing examples such as Ireland and the UK in 2010-14 and Denmark in the 1980s. Italy, he noted, had raised taxes and seen “its economy plummet”.

Larry Summers, former adviser to Barack Obama, argued earlier this year that it is time Washington ends its debt obsession © Getty

The more extreme versions of fiscal activism, including MMT, are being challenged by mainstream economists who question the idea that public debt can always be financed by printing money without triggering problems such as high inflation. Mr Summers has decried it as “voodoo economics” offering false promises of a free lunch — drawing a parallel with conservative supply-side theorists who he says argue tax cuts can pay for themselves. Jay Powell, the Federal Reserve chairman, has called the theory “just wrong”.

John Llewellyn, a former chief economist of the OECD, says MMT activists were “often near-messianic in tone, while somewhat vague in exposition”. He adds: “MMT is appropriate only in exceptional situations, where economies are far from full employment, deflationary pressures are in evidence, and interest rates are at the zero bound.”

Even US progressives are anxious to avoid being labelled as fiscally irresponsible, with Democrats focusing heavily on taxing the wealthy as a way of raising revenue and redressing inequality. Mr Sanders in a recent Fox News debate insisted that high public debt was a “legitimate concern” and insisted he would pay for his far-reaching plans to expand state medical coverage. “We pay for what we are proposing, unlike the president of the United States,” he said.

Yet few politicians are putting forward plausible plans to arrest the inexorable rise in debt. No matter who holds the White House, the world is set to watch a major fiscal experiment over the coming decade. This will establish whether the remorseless rise in America’s public debt is a largely benign phenomenon — or an economic and financial menace.

0 comments:

Publicar un comentario