Weakness in Chinese currency raises questions over Beijing’s tactics in trade spat

Hudson Lockett and Daniel Shane in Hong Kong

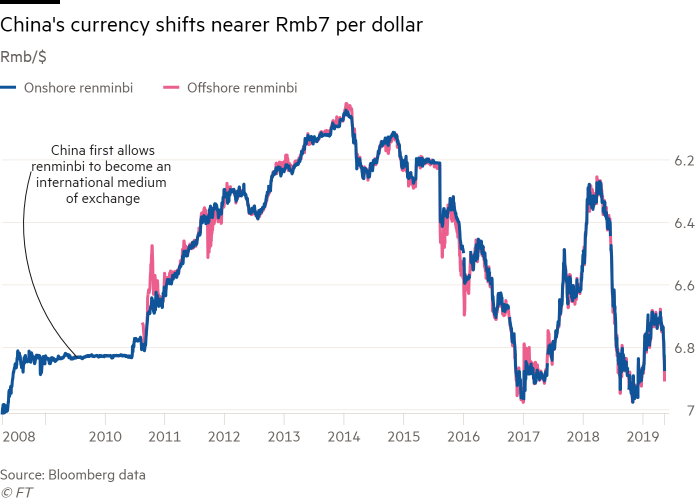

What’s going on with the renminbi?

In short, it is weakening, as market participants brace for further details about planned US tariffs on a further $300bn of goods imported from China.

The scale of the fall depends on which type of the Chinese currency you are referring to. The offshore renminbi slipped almost 1 per cent on Monday to more than Rmb6.9 per dollar, its weakest level since December, while the more tightly controlled onshore exchange rate was a touch less volatile, weakening as much as 0.8 per cent to Rmb6.877.

How does this help China, and is Beijing behind the move?

China has devalued its currency in the past in an effort to support exports while limiting imports. These days, it tends to step back and allow markets to push the exchange rate in either direction, usually quite gradually, in line with its objectives at the time. On Monday the People’s Bank of China, the central bank, set the onshore rate’s trading band weaker for a third straight day, suggesting it is not averse to further falls.

But it is too early to tell if Beijing is forcing the slide at the moment.

A weaker exchange rate in the wake of the latest rise in US tariffs would provide China with cheaper and more competitive exports as it grapples with the latest demands for concessions out of Washington. But it would also have costs.

In August 2015, Beijing carried out the biggest one-day devaluation of the renminbi in more than two decades, in what critics described as an effort to boost its export-driven economy. However, the downward adjustment of the currency exposed China to criticism and it complicated relations with the US, where politicians have long argued that the renminbi is undervalued.

The move also undermined China’s efforts to have the renminbi accepted as a global reserve currency alongside the dollar, yen, euro and sterling. Gains made by the renminbi in this respect, before the devaluation, have since been reversed. In March the currency accounted for just 1.2 per cent of international payments, according to data from Swift.

Could this escalate and how will the US respond?

China could continue to allow the renminbi to weaken against the dollar by declining to step in and counteract downward pressure from markets. Analysts have tipped the exchange rate to become more volatile in the next few weeks amid heightened uncertainty over whether Beijing and Washington can finally bury the hatchet on trade. Some expect it to pass Rmb7 per dollar by the end of the year.

But there is little sign that Beijing has abandoned its long preference for more gradual, managed movements in the foreign exchange rate. Few observers expect a drastic move akin to that seen four years ago.

The case against Beijing is not very strong at the moment, even from a US policy perspective. The US Treasury Department in October once again declined to label China a currency manipulator even as it expressed “concerns” over the weakening exchange rate, which was then closer to Rmb7 per dollar than at any point since 2008.

That lack of an official designation is unlikely to stop the Trump administration from accusing Beijing of currency manipulation, particularly if trade tensions escalate further, putting still greater downward pressure on China’s currency.

What do falls in the renminbi mean for other countries?

The effects of a weaker renminbi may be seen on those economies that depend on selling goods to China, such as South Korea and Australia, because their exports have effectively become more expensive for Chinese buyers. South Korea’s won also fell sharply on Monday.

When Beijing engineered a major devaluation of the renminbi four years ago, some of the biggest initial responses were felt in the prices of commodities such as oil and shares of mining companies, for which China is a major customer.

Declines in the value of the renminbi make Chinese goods cheaper for the rest of the world which, given the country’s role as the world’s second-largest economy, could risk spreading deflationary pressures to trading partners. When a country slashes the value of its currency to boost exports, it can also risk triggering competitive devaluations by trading partners seeking to protect their own export industries.

0 comments:

Publicar un comentario