Failure To Communicate

by: The Heisenberg

Summary

- Jerome Powell's post-FOMC press conference on Wednesday ended up shifting the narrative materially.

- It's not entirely clear whether the Fed chair meant to come across as "hawkish", per se, and therein lies the danger of holding press conferences after each meeting.

- Here's a comprehensive, in-depth take on this week's most important event.

- It's not entirely clear whether the Fed chair meant to come across as "hawkish", per se, and therein lies the danger of holding press conferences after each meeting.

- Here's a comprehensive, in-depth take on this week's most important event.

It took roughly six months for me to feel vindicated regarding my long-held contention that Fed Chair Jerome Powell's "plain English" (as he famously called it) approach to communicating with markets would end in tears.

Right up until October 3, pundits and analysts celebrated Powell's "non-academic" approach. But cheers turned to jeers when the Fed chair's tone-deaf characterization of policy as "a long way from neutral" came across as unnecessarily aggressive under the circumstances and set the stage for what would eventually morph into a horrendous quarter for risk assets of all stripes.

Powell's December press conference was, by most accounts, disastrous. Minutes from the December meeting would later reveal that Powell arguably failed to convey the tone of the actual policy discussions taking place at the time, to the detriment of fragile market sentiment.

A related argument of mine from last year was that Powell's decision to hold press conferences after every meeting was a bad idea. It would, I suggested on too many occasions to count, have the opposite of its intended effect. Specifically, I argued that more frequent press conferences had the potential to create confusion, especially if Powell proved to be less-than-adept at communicating.

Wednesday's proceedings were an example of why less is often more when it comes to post-FOMC press conferences. The market went into the May Fed decision expecting a "dovish hold" and that's precisely what the FOMC delivered. The statement effectively downgraded the inflation outlook and referenced the Fed's "patient" approach. The committee also delivered the IOER cut that everyone knew was coming at some point.

Obviously, the Fed has come under immense political pressure to cut rates, despite the US economy expanding at a 3.2% annualized pace in Q1 (the internals from the GDP report weren't great, but the headline print certainly doesn't scream "time to cut rates") and despite unemployment sitting at a five-decade nadir. Over the past two months, Fed officials, White House aides and President Trump himself have gone out of their way to debate whether subdued inflation theoretically provides a justification for what, in market circles, is known as an "insurance" cut. Calls for such a move come as the Fed is set to reconsider its inflation framework and there are rumors that policymakers could eventually opt for a strategy that involves letting the labor market run "super-hot" (think: a 2-handle on unemployment) on the excuse that that's what's necessary to get inflation sustainably to target.

If you go back and read the transcript of the October 23-24, 2012, FOMC meeting, you'll find Powell delivering the following remarks (he was referring to the balance sheet, but the sentiment is applicable in a general sense):

The market in most cases will cheer us for doing more. It will never be enough for the market.

At the beginning of this year, markets were clamoring for clarity on the balance sheet. All anyone wanted was a hint that the Fed would at least consider altering the pace of runoff to account for the possibility that at some point last year, QT ceased to be "like watching paint dry" (as Janet Yellen put it) and began to negatively affect risk assets. Bear in mind that there is scant evidence to support the contention that we crossed some kind of magical threshold in the second half of last year beyond which runoff was having a direct, mechanical impact. The psychological effect was likely far more important in explaining the apparent connection between the selloff in risk assets and QT. That said, there is a link between MBS runoff and stocks/volatility, and it is true that if you add the current Fed rate to the 300bp rise in the shadow rate from the lows in 2014 (attributable to the wind down of QE), you end up around 5.5% worth of tightening, so it's at least plausible to suggest that things finally "snapped" in Q4.

In any event, fast forward from the first three days of January (i.e., before Powell's remarks in Atlanta on January 4 which set the dovish pivot in motion) to this week's FOMC meeting, and the Fed has given the market everything and more.

There is now an end-date for runoff, the beginnings of a plan on what will happen after runoff ceases, a commitment to being on hold ("patient") enshrined in the dots, and regularly-floated trial balloons, which all generally seem to suggest that at some point, subdued inflation could warrant a preemptive rate cut, even if the economy is doing well.

The market has responded by pricing in easing and risk assets have levitated. Cross-asset volatility has concurrently collapsed. Stocks are at all-time highs, high yield spreads have tightened dramatically off the Q4 wides, BBB credit (last year's boogeyman) had its best first quarter to a year since 1995, and on and on. Here's an updated cross-asset performance chart (current through Monday):

(Goldman)

But, as Powell put it more than six years ago, "it will never be enough for the market", and now that "the market" includes the President of the United States, it's little wonder that the Fed chair was subjected to questions on Wednesday about the threshold for a rate cut.

Here is where I get to remind you that Wednesday's press conference was entirely unnecessary. It was Powell's decision to hold press conferences after every meeting, and had he not presided over one this week, he would have been spared a series of questions about inflation and whether subdued price pressures could conceivably be used as an excuse to cut rates. The Fed could have easily worked into the statement language which communicated the idea that factors weighing on inflation are seen as transitory. Further, if someone can explain to me why Powell needed a press conference this week to reiterate that the Fed currently sees no strong case for moving either way on rates, I'd love to hear it, considering that when you've just kept rates on hold it pretty much by definition means you didn't see a strong enough case for adjusting them.

Long-time followers of mine might well be tempted to respond with "What about Mario Draghi's press conferences?" To that I would simply reiterate that Jerome Powell is not Mario Draghi who, in addition to being famously adept at communicating, generally has more to talk about given that he's conducting monetary policy for a disparate collection of economies, all with their own unique fiscal and political situations.

In any event, the dovish market reaction to the Fed statement and the IOER cut was promptly erased when Powell discussed the reasons why he believes the factors weighing on inflation are likely to prove transitory. His reiteration that the committee didn't see a strong case for moving either way on rates only magnified the hawkish character of the presser.

You might well argue that Powell felt it was incumbent upon him to push back against the notion that a rate cut is imminent and to (implicitly) defend the Fed's independence amid withering political pressure to ease. You could also plausibly argue that Powell knew the IOER cut had the potential to be interpreted as something other than a technical adjustment (i.e., as conveying something about policy) and therefore thought he needed to clarify.

But, again, all of that could have been worked into the statement and, in the case of the clarification on the IOER tweak, into the implementation note.

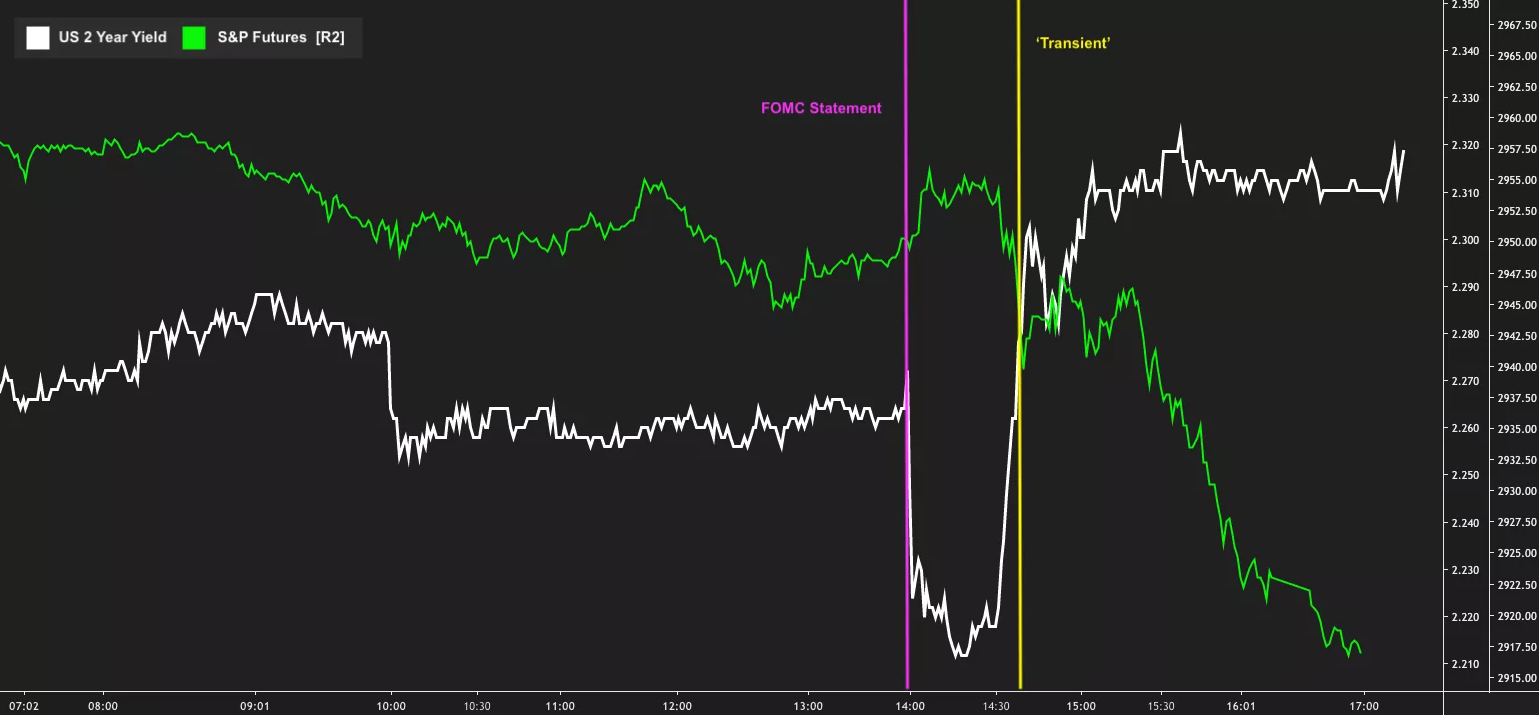

Instead, it was delivered in "plain English," and while I don't pretend to know how policymakers felt about the U-turn in rates on Wednesday, I can confidently say that what you see in the following chart isn't desirable from a policymaker perspective:

(Heisenberg)

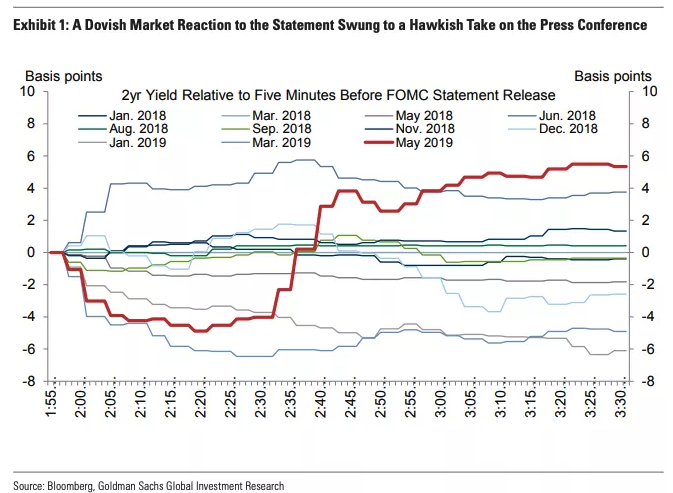

If you're wondering whether that ~10bps swing in 2-year yields from the initial knee-jerk to where things stood an hour later is "normal", the answer is no. Here's a chart from Goldman:

(Goldman)

Again, this was avoidable. Everything Powell said in the press conference could have easily been incorporated into the statement, and markets would have latched onto the "dovish hold" and gone about their business. Instead, there was confusion.

You can read a summary of Wall Street's reactions here, but suffice to say analysts are willing to give Powell the benefit of the doubt regarding the relative wisdom of expounding on the "transient" factors pushing down inflation. As I argued on Thursday morning, though, that generous assessment could well be explained by the fact that so many desks were caught completely wrong-footed with their Fed calls for 2019 and are now hoping against hope that a cut doesn't in fact materialize and make those calls seem even more off the mark in hindsight.

For my money, I'm inclined to agree with Nomura's Charlie McElligott, who expressed more than a little skepticism about the whole situation on Thursday morning. "I remain completely convinced that the bar to cut rates is infinitely lower than the bar to hike again", he wrote, after noting that "Powell's messaging on 'transitory' factors behind inflation weakness was met with a collective eye-roll and broad investor cynicism."

The follow-through on Thursday was less than inspiring, as both stocks (SPY) and bonds (TLT) fell in tandem in what was pretty clearly a post-Fed positioning adjustment. Sharply higher real yields certainly didn't help stocks' cause.

(Heisenberg)

In case you were wondering whether you can blame risk parity (a frequent scapegoat whenever bonds and equities fall/rise simultaneously), the answer is probably not. Rather, this was just an example of what happens when the narrative suddenly shifts. Here's what McElligott had to say in an afternoon client note:

We simply had a lot of people on the same side of the same trades with the same view-and it was working fine; stability breeds instability however, and all it takes sometimes is a modest tweak to a narrative which then "tilts" excess positioning / leverage into a correction with occasional "cleanses".

Goldman of course had a lot to say in the aftermath of the press conference, but midway through Thursday, the bank weighed in with a little ad hoc color as follows:

We didn't think the Fed was contemplating a cut, but we acknowledge that markets did, and markets have had to unwind some of this expectation over the last few trading hours. Interesting to consider: you can't have it both ways. The reason why the Fed is not factoring in a cut is because it thinks growth remains "moderate or perhaps modest" - also consistent with the absolute levels of the ISM Manufacturing Index (if not the second derivative inflection).

The point being, you might well think Powell said all the right things during the press conference (and, for what it's worth, Goldman's other two Fed postmortems suggest the bank thinks he in fact did get it right), but in my view, everything that needed communicating could have been channeled through the statement. You are not going to convince me that whatever position adjustments have been made over the past 24 hours would have looked the same way had the message been delivered more subtly via the statement as opposed to Powell standing at the podium and pounding the table on "transitory". It is my opinion that Wednesday's press conference created unnecessary confusion.

Perhaps the riskiest thing about Wednesday was that the perception of a hawkish turn from Powell helped put the brakes on a much needed pullback in the dollar, which recently summitted new YTD highs. At a certain point, dollar strength is going to weigh on risk assets and, indeed, it's already starting to impact emerging markets at a time when idiosyncratic turmoil is picking up again in Argentina and Turkey.

As you're probably aware, the Fed's dovish turn in 2019 has not translated into dollar weakness, primarily because the FOMC's global counterparts leaned dovish in tandem and also because relatively speaking, the US economy continues to hold up well. Have a look at the following chart:

(Heisenberg)

I used a red line to show Thursday's rise in real yields. The question you should ask yourself when you ponder that visual is this: If the dollar has been as resilient as it has in the face of sharply lower real yields, what will the greenback do if, suddenly, real rates start to rise again on the back of more hawkish Fed expectations?

If your answer is that the dollar will probably strengthen even more, then think about the implications of that for EM.

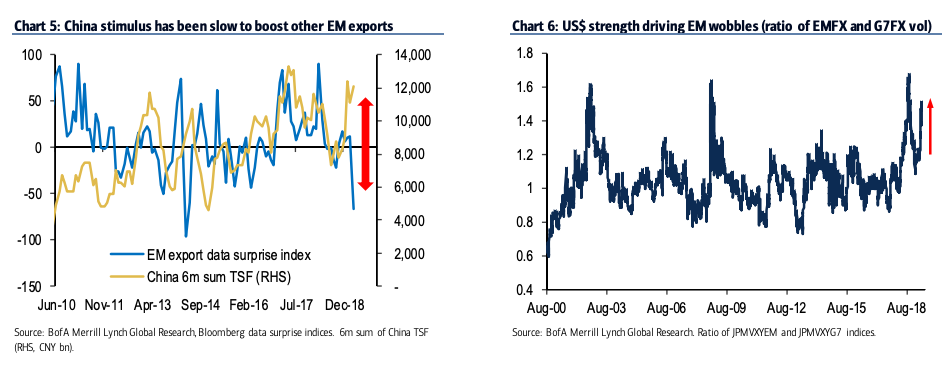

In that context, consider this brief color from a BofA note dated Thursday:

While China is doing an impressive job at stimulating (note the jump in Total Social Financing), export dataflow for other EM economies remains disappointing (South Korea and Taiwan exports are still very weak). China's stimulus may be less effective this time around (vis-à-vis '15/'16) given the rebalancing of the Chinese economy more towards domestic consumption and away from investment. EM has been a winner in 2019 amid central banks' dovish pivot. YTD inflows into global EM debt funds have amounted to an impressive $25bn (close to surpassing the pace of inflows in '17). But US Dollar strength may be a harbinger of a rise in EM FX volatility. Chart 6 shows that the ratio of EM FX vol to G7 FX vol has risen again since the end of March.

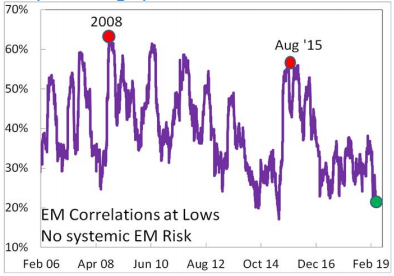

On the bright side, EM country correlations (stock markets) are near record lows, which suggests any spillover from dollar strength into vulnerable locales with idiosyncratic issues should remain contained. Here's JPMorgan's Marko Kolanovic on the correlations point:

Country correlations near all-time lows indicate there is little risk of a systemic EM crisis, e.g. driven by the strong USD. Record low correlations indicate that recent EM troubles are more of a collection of country-specific developments (e.g. Turkey, Brazil, Argentina, etc.) rather than a systemic EM crisis in the making.

The point in all of the above is to illustrate and otherwise underscore how sensitive the narrative is to any turn of phrase from the Fed.

Wednesday's post-FOMC press conference might fairly be described as an admirable effort on the part of Powell to recalibrate market expectations vis-à-vis a cut and to reassert the Fed's independence from politics. That's all fine and good, but I would argue that markets could have done without the extended discussion, especially when it comes from someone who isn't known for his ability to strategically employ academic doublespeak in the service of making it difficult for market participants to confidently categorize a given utterance as "hawkish".

The punchline to this whole discussion is that everyone will have a chance to effectively re-trade the Fed on Friday as April payrolls will now be viewed through the lens of Powell's presser.

0 comments:

Publicar un comentario