Nearly £6bn worth of ‘tap and pay’ transactions in February alone

James Pickford

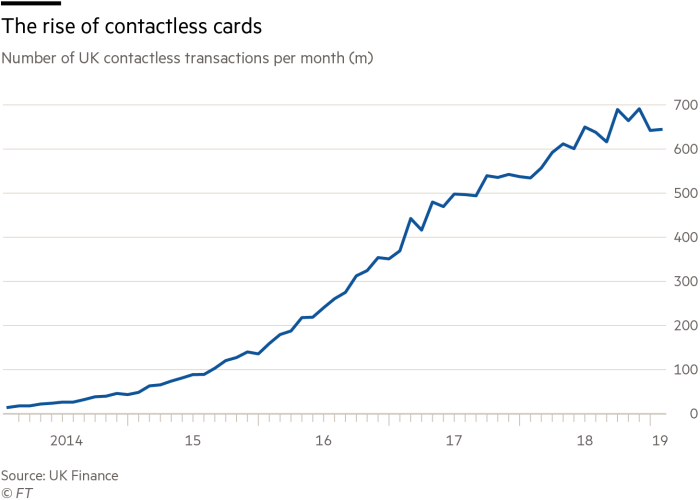

What does the chart show?

It illustrates the onward march of contactless card transactions, the now ubiquitous technology which allows “tap and pay” payments to be made using a debit or credit card. In the past five years, the number of monthly contactless transactions in the UK has rocketed from 14m in February 2014 to 644m in February 2019.

The latest monthly figures for contactless transactions, published this week by UK Finance, were 20.6 per cent up on February last year. A similar rise was registered for the value of transactions, which jumped by 19.8 per cent to £5.9bn compared with February 2018.

Is it likely to continue going up?

The trend is rising in the medium term, but the February figures are slightly lower than those for December. Some believe the growth in contactless will fall off as people get used to using their smartphones to make payments and other financial tasks.

UK Finance, which represents banks and other financial services providers, has no truck with this. It thinks the rise will continue for a lot longer yet and predicts that 36 per cent of all payments will be made via contactless cards by 2027, up from 15 per cent in 2017.

Eric Leenders, UK Finance managing director of personal finance, said in March: “Many of us are now reaching for our cards or mobiles rather than cash to make low-value purchases, as customers opt for the convenience and security of paying with contactless.”

How much is debit vs credit card spending?

The great majority of contactless payments — 85 per cent is spent via debit cards. The rise in debit card usage has also come alongside a fall in the use of cash to make payments, with debit cards overtaking cash for the first time in 2017 as the most frequently used means of payment. Debit card usage is expected to grow faster than any other payment method over the next decade.

UK Finance noted this year that there had been an increase in credit card use, but the slowing growth in outstanding balances suggested consumers were using credit cards for day-to-day spending rather than borrowing.

Is fraud a problem?

Yes, and the sheer variety of card frauds is sobering. Thieves could steal cards, using them up to the £30 contactless limit as often as possible before the card is stopped. Card details may also be extracted by criminals when the owner makes an online payment or responds to an unsolicited email or telephone call, usually as they are fooled into thinking the respondent is a trusted person such as a police officer or solicitor.

Hackers may also be able to tap into a network or computer and siphon off card details.

Fraudsters may also skim details from a card reader, clone cards or open an card account in someone else’s name, having stolen their personal information.

So-called remote purchase fraud, carried out when the card owner still has the card in their possession, account for most card fraud, covering 72 per cent of the total in 2017.

However, the most recent industry figures showed an 8 per cent fall in fraud losses on UK-issued cards, which totalled £566m in 2017 — the first decline for six years. At a time when total spending on all debit and credit cards hit £755bn, the industry says this reflected its efforts to combat fraud through high-tech security tools and quicker responses when fraud is reported.

0 comments:

Publicar un comentario