Monetary policy has run its course

It has made secular stagnation worse. Fiscal alternatives look a safer bet

Martin Wolf

Why are interest rates so low? Does the hypothesis of “secular stagnation” help explain it? What do such low interest rates imply for the likely effectiveness of monetary policy during another recession? What other policies might need to be tried, either as an alternative to monetary policy or a way to make it more effective? These are the most important questions in macroeconomics. They are also hugely contentious.

A recent paper by Lukasz Rachel and Lawrence Summers shines light on these questions. Its thrust is to support and elaborate the hypothesis of “secular stagnation”, revived by Prof Summers as relevant to our era in 2015. This paper’s principal innovation is to treat the big advanced economies as a single bloc. Here are four conclusions.

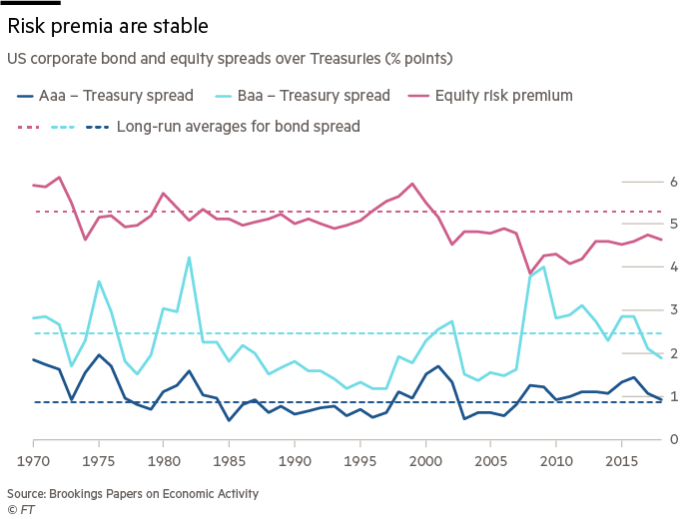

First, a dramatic and progressive decline in real interest rates on safe assets has occurred, from over 4 per cent in the 1980s to around zero now. Furthermore, shifts in risk preferences do not explain this decline, since spreads in yields of riskier over safe assets have changed little. (See charts.)

Second, this secular fall in real interest rates implies a roughly equivalent fall in the (unobservable) “neutral” or “equilibrium” rate — the rate at which demand matches potential supply.

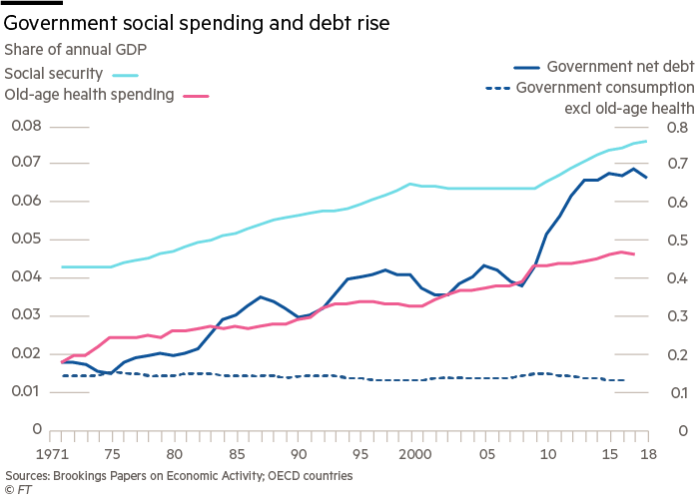

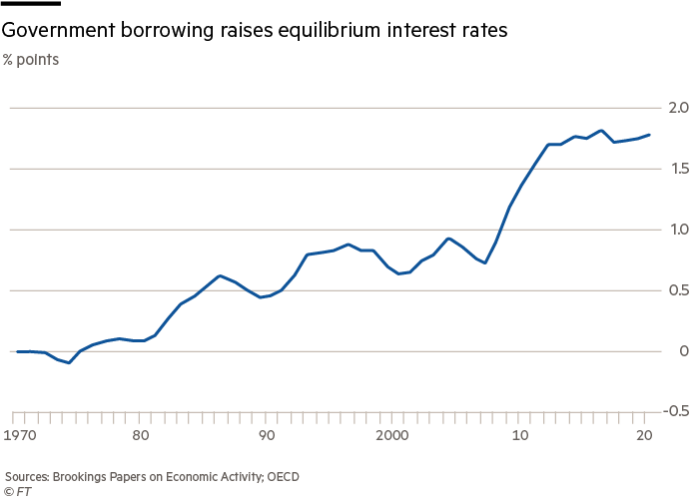

Third, governments are not generating this structural weakness in demand. On the contrary, by expanding social spending, deficits and debt, governments have raised equilibrium long-term real interest rates, other things being equal.

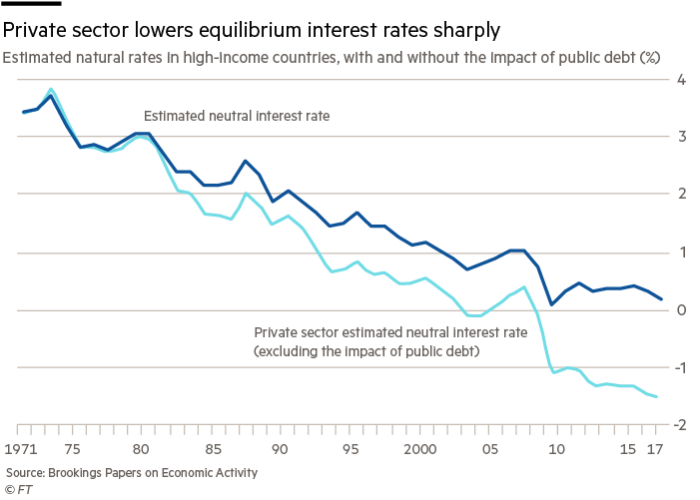

Finally, changes in the private sector would, on their own, have generated a fall of more than seven percentage points in the equilibrium real rate of interest. Among the many factors driving this sharp decline must have been ageing; declining productivity growth; rising inequality; declining competition; and falling prices of investment goods.

The authors conclude that the hypothesis of “secular stagnation” in the high-income economies — chronically weak demand, relative to potential output — is highly credible. After all, they write, “prior to the financial crisis, negative real short-term interest rates, a huge housing bubble, erosion of credit standards and expansionary fiscal policy were only sufficient to achieve moderate growth. Adequate growth in Europe was only maintained through what in retrospect appears to have been clearly unsustainable lending to the periphery.”

This analysis has big implications now. When recessions hit, real short-term interest rates need to fall sharply and the yield curve (which shows the rates on bonds of varying maturities) needs to become strongly upward sloping if monetary policy is to stabilise the economy. Suppose, then, that our economies were to fall into a deep recession, yet still have near zero real interest rates and very low nominal rates, too.

Suppose, too, that, inflation were somewhere between zero and two per cent. Then the response to a recession would require strongly negative short-term nominal interest rates, possibly as low as minus 5 per cent. That would, to put it mildly, create a wasps’ nest of technical, financial and political problems.

This analysis implies that central banks are not creating low real interest rates, as critics charge, but delivering the low real rates the economy needs. A paper by Claudio Borio and others at the Bank for International Settlements takes precisely the opposite point of view: this argues that monetary regimes set real interest rates, even in the long run — a position that contradicts standard views on the need to separate monetary from real processes in economics.

This seems hard to accept, in general. But it is highly relevant in a critical respect: this is that interest rates play a big part in driving credit cycles. Indeed, that is how monetary policy normally works. If the central bank wants to raise inflation in an economy with structurally weak demand, it will do so by encouraging the growth of credit and debt. It might then fail to raise inflation, but create a debt crisis. That is deflationary, not inflationary.

Thus, the pre-crisis monetary policy, aimed at raising inflation, has now created the opposite: a deflationary debt overhang that works via what Richard Koo of Nomura calls “balance-sheet deflation”. That in turn leads to still lower nominal (and real) rates. Thus, the financial mechanisms used to manage secular stagnation exacerbate it.

We need more policy instruments. The obvious one is fiscal policy. If private demand is structurally weak, the government needs to fill the gap. Fortunately, low interest rates make deficits more sustainable. According to recent papers by Olivier Blanchard, former chief economist at the IMF, and Jason Furman, former chairman of the US council of economic advisers, together with Prof Summers, this combination is not just true now, but has been true in the past. That makes fiscal policy a far safer bet.

It is of course essential to ask how best to use those deficits productively. If the private sector does not wish to invest, the government should decide to do so. But it can also improve the private incentive to invest. The world needs to make huge investments in new energy systems: a mixture of public and private investment is clearly the best response.

The credibility of the “secular stagnation” thesis and our unhappy experience with the impact of monetary policy prove that we have come to rely far too heavily on central banks. But they cannot manage secular stagnation successfully. If anything, they make the problem worse, in the long run. We need other instruments. Fiscal policy is the place to start.

0 comments:

Publicar un comentario