Don’t let emerging markets be the ‘something that breaks’

The Fed is stirring a perfect storm and EM policymakers must act while they can

José Antonio González

The US Federal Reserve in Washington, DC. Emerging markets are "price takers" of US monetary policy © Reuters

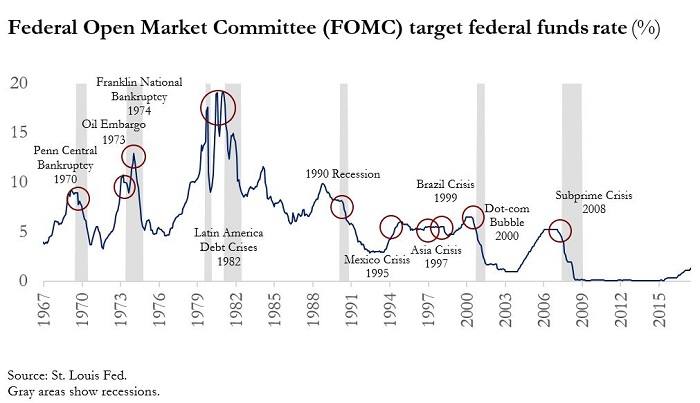

Ever since the Great Depression, with only two exceptions, every time the US Federal Reserve has gone through a monetary tightening cycle, something in the world economy has broken — the bankruptcy of a major bank, a localised banking crisis, or an outright, full-fledged financial crisis. And ever since emerging markets became more integrated into the world’s financial markets, they have tended to be centre stage.

A Fed tightening cycle preceded the debt crisis in Latin America in 1982, the Mexican crisis in 1995, the dotcom bubble in 2000 and the global financial crisis of 2008-09. Although rates did not rise at the time, one could argue that the Asian and Brazilian crises of the late 1990s were in part due to the that fact interest rates remained relatively high.

The transmission mechanism is well understood. In a nutshell, the Fed sets interest rates for the dollar and, the dollar being the world’s reserve currency, this determines the cost of money worldwide. When the Fed increases rates, the cost of money rises, investment decreases and the economy slows down.

In emerging markets, there are typically two additional effects when interest rates rise. First, risk-adjusted rates of return become less attractive, causing a reversal of capital flows, in turn leading to more than proportional increases in local interest rates (known in the international parlance as spread decompression). This further decreases investment and complicates new financing and debt rollovers for governments and firms. Second, the slowdown typically causes a drop in commodity prices, which can have a large impact on certain economies.

But let’s be clear, this is not the Fed’s fault. Although it is sensitive to the repercussions of its policy decisions, the Fed has its own clear monetary mandate. Emerging market economies are “price takers” of monetary policy from the Fed and should adjust accordingly.

This brief historical recap is relevant today because there are various elements in the macroeconomic financial conditions worldwide that are coming together to form a particularly difficult juncture and, if not a perfect storm, certainly a pretty good one.

First, the Fed began a new monetary tightening cycle in 2015. It has included nine hikes, and market participants are expecting more, although there is a debate as to how fast and how high interest rates will rise. Admittedly, by historical standards, the levels are still low, at 2.25-2.5 per cent, but the trend is clear.

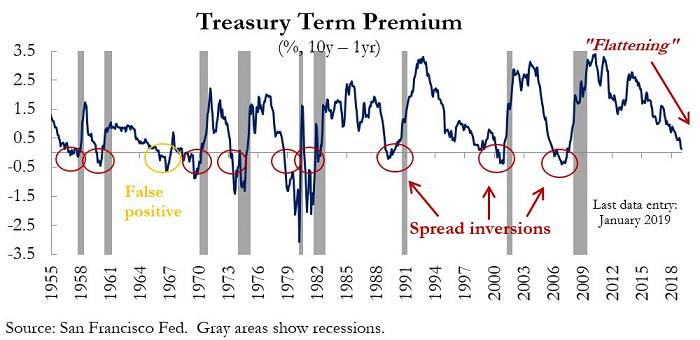

Second, increases in the Fed’s rate have caused the term spread (the difference between short and long-term interest rates) to flatten to around 0.13 percentage points — comparable to levels observed before the onset of the 2008 financial crisis. History shows that an inversion in the term spread is a good predictor for a recession in the US. Since World War II, every time the term spread has inverted, a recession has followed — with only one exception, when there was not a recession but a deceleration.

The third element is that trade tensions could damage global and domestic activity as well as confidence. Since April 2018, stock performance of firms exposed to trade have underperformed by as much as 8 per cent compared with the S&P 500. Moreover, the IMF has warned that current trade tensions risk lowering global growth by as much as 0.5 per cent by 2020, or about $430bn in lost GDP worldwide.

In short, if these factors come together simultaneously they could have a huge impact in emerging economies. A looming recession or deceleration in advanced economies will lower export demand, which, coupled with trade tensions, will probably cause commodity prices to fall, hurting export-dependent emerging market economies. Rising interest rates in the developed economies will cause capital flow reversals from emerging markets, which we began to observe in 2018, making refinancing and debt rollovers more difficult.

There is a silver lining, however: the storm is not here yet. The two largest economies, the US and China, still show robust growth and, perhaps more importantly, the Fed recently indicated that it may raise rates more gradually. Policymakers in emerging markets have time.

There are no magic bullets. The best course of action is to make sure the basic macroeconomic indicators are in order:

1) Fiscal accounts need to be balanced in at least two dimensions: fiscal deficits need to be lowered or outright eliminated, as access to financing will become more difficult; and the debt profile needs to be improved by opting for domestic rather than foreign debt, fixed rather than flexible rates, and longer maturities.

2) External accounts also need to be balanced. The current account should be close to equilibrium because, even if fiscal accounts are in order, external imbalances can be a source of vulnerability and cause a foreign exchange crisis.

3) Monetary policy plays a crucial stabilising role in the face of volatility. It should be conservative both to ensure price stability and to avoid sudden capital flow reversals. At the same time, central banks in emerging markets face a limit to how much to defend the flow of capital, and a commitment to free-floating exchange rates is paramount. Fixed exchange rate regimes have proved costly in the past.

4) Finally, the financial sector must be well capitalised, liquid, not overly exposed nor be the cause of an asset bubble (especially in real estate). It is important not only to look at banks but also at non-bank financial intermediaries, particularly now that inclusion in the financial sector has been actively promoted through fintech and financial innovation.

If the measures outlined come from such basic macroeconomic principles, the obvious question is, why have emerging economies been caught off guard so many times in recent history? The answer is not clear, but let me propose two possible explanations:

First, prudent macroeconomic policies are not popular or easy to implement anywhere, but especially in emerging economies: Fiscal deficits allow greater public spending on social programmes; current account deficits are typically associated with overvalued exchange rates, which make imports and the goods and services we buy abroad cheaper; and financial regulatory forbearance implies that credit is more widely available. The problem is that all of these conditions are temporary and not sustainable.

Second, macroeconomic financial institutions are less mature in emerging markets: central banks and financial regulators are not as independent and as capable as in developed countries, fiscal rules and budget laws are not as solid and, therefore, do not insure long term fiscal sustainability and transparency.

But there is time for emerging markets to prepare for what is coming. Now is not the time to doubt prudence and test the will and ferocity of the worlds’ financial markets. Now is the time to adopt prudent macroeconomic policies to make sure that our economies are resilient to the headwinds that will surely become stronger. In other words, to make sure that the “something in the world that breaks” is not the emerging markets.

José Antonio González is a former Minister of Finance of Mexico.

0 comments:

Publicar un comentario