Hint: By stealing yields on bank deposits

By Nathaniel Taplin

Imagine the following: The labor market is suffering. You’re paying off an expensive mortgage while losing money on your bank account. Would you want to fork out for a pricey iPhone?

That’s the situation many urban Chinese face today. China’s two-year crackdown on high-yielding “shadow banking” investment products has curtailed some financial risks. But it has also deprived indebted households—which earn negative real returns on their standard bank deposits given inflation has been running higher than interest rates—of an important income source. Fixing this is one key to stabilizing consumer spending and to the prospects of China-exposed companies such as Apple .

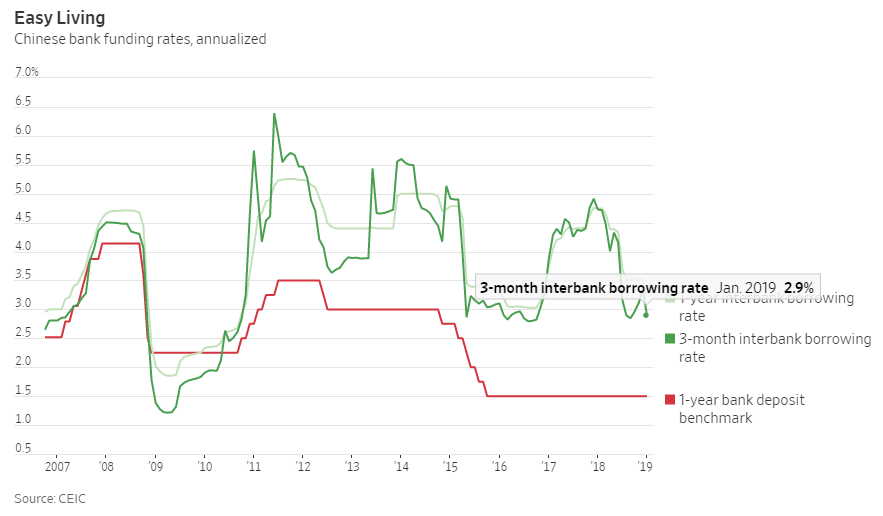

The root problem is the privileged position of China’s biggest state-owned banks such as Industrial & Commercial Bank of China IDCBY -0.13%▲ and Bank of China. They are able to suck in retail deposits, paying customers low state-set interest rates. In turn, they lend to smaller banks, which do much of the actual lending to the real economy but are prevented from competing for household deposits by freely raising rates. In essence, the big banks are earning a juicy spread as intermediaries between depositors and smaller lenders, stealing yield from the former and raising costs for the latter.

This rent-seeking activity by China’s banking behemoths is a big drag on Chinese households, whose biggest financial asset—totaling 71.6 trillion yuan ($10.6 trillion)—is bank deposits. If weighted average retail deposit rates were to rise by 1 percentage point, that would put an extra 716 billion yuan in households’ pockets, more than twice the 300 billion yuan Merrill Lynch estimates that China’s recent tax cut puts in households’ pockets.

Chinese spending on products such as the iPhone has been hurt by shrinking pockets. Photo: Lintao Zhang/Getty Images

The situation for households has been made harder by the shadow-banking crackdown. That has crushed issuance of higher-yielding savings products, which used to give savers a way to augment low deposit returns. Outstanding wealth-management assets, typically paying an annualized interest rate of about 5% against 2% for bank deposits, had dropped to 24.8 trillion yuan by the third quarter of 2018, according to Moody’s ,after nearly tripling to 30 trillion yuan from 2014 to 2016.

All this hits households in other ways, too. Why, for instance, should big banks bother lending to risky private companies—the main drivers of employment—when they can pocket easy money just by lending to smaller banks or higher rated state-owned enterprises?

Chinese regulators know they have a problem. There have been some recent, tentative signs of progress on reform, including marginally higher rates on big certificates of deposit and a slightly softer stance on wealth-management products.

These, however, are baby steps. Chinese consumption isn’t collapsing, but it’s definitely under pressure. Forcing households to prop up the sclerotic state banking system, on top of the weak labor market, isn’t helping.

0 comments:

Publicar un comentario