Why the world economy feels so fragile

Political instability will make it harder to ride out a slowdown

Martin Wolf

Should we be concerned about the state of the world economy? Yes: it always makes sense to be concerned. That does not mean something is sure to go badly wrong in the near future. On the contrary, the world economy seems to be heading into just a mild cyclical slowdown. Far more important is the adverse longer-term structural and cyclical context because it makes any short-term swing far more perilous.

According to Goldman Sachs, the momentum of global economic growth slowed markedly in 2018. The most globally significant slowdown has been in the Chinese economy— the main engine of global growth since the financial crisis of 2007-08. But Germany and Japan also recorded economic contractions in the third quarter of last year. Stock markets have also been in turmoil. In part, that presumably reflects worsening perceptions of prospects. These falling markets should also weaken consumption and investment.

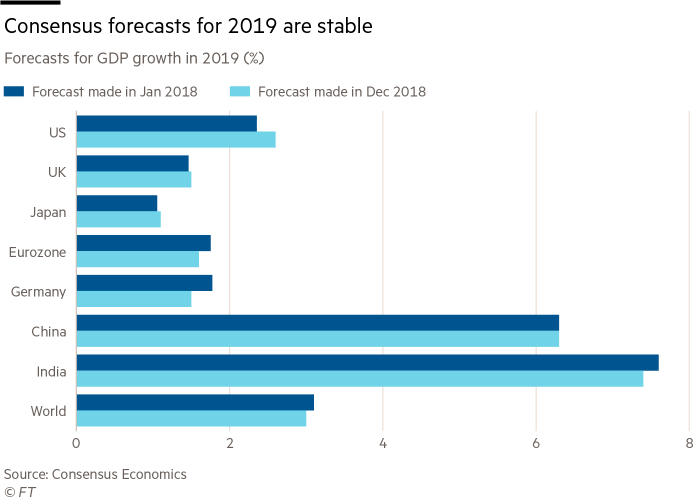

All this suggests a cyclical slowdown is on the way. Yet conventional forecasters are hardly unduly worried. The OECD stated last November that the “global expansion has peaked” and that global gross domestic product growth is “projected to ease gradually from 3.7 per cent in 2018 to around 3.5 per cent in 2019 and 2020, broadly in line with underlying global potential output growth”. This would be an ultra-soft landing. Consensus forecasts support this: the December consensus forecasts for growth in 2019 are little different from those made a year ago. Growth prospects for the US are even slightly upgraded. (See charts.)

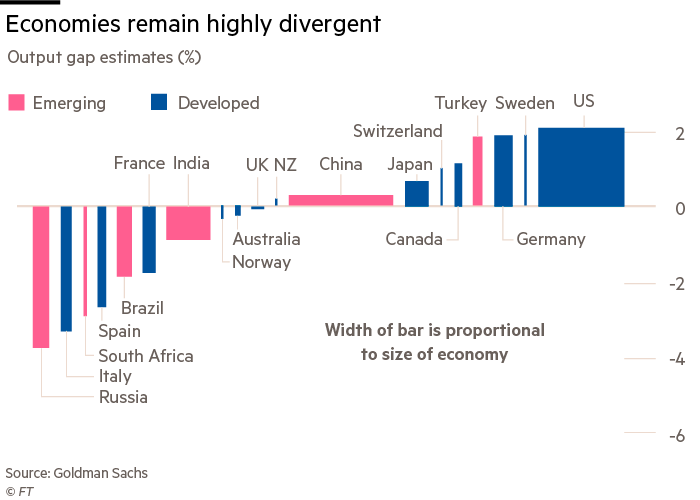

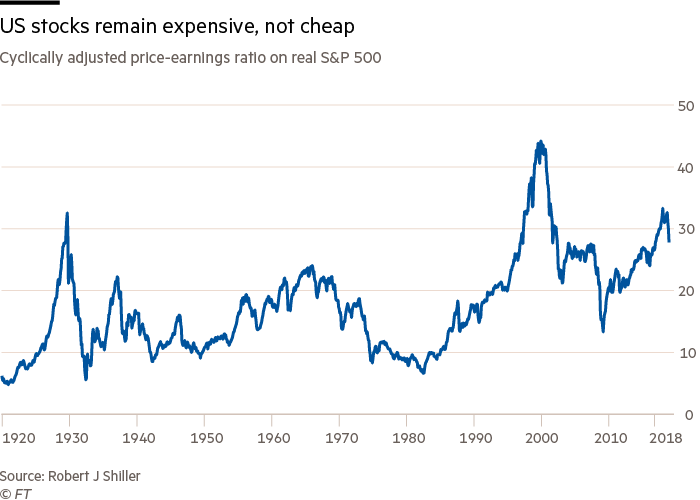

A mild economic slowdown should hardly be problematic. On the contrary, it is to be expected. In the high-income economies, which still generate three-fifths of world output (at market prices), the cyclical upswing is elderly and excess capacity has fallen sharply. Where the expansion is most advanced and excess capacity has disappeared, monetary policy has been duly tightened, quite appropriately, pace Donald Trump. Happily, inflation is still subdued and nominal and real interest rates are low. While equity markets have indeed corrected, US stocks have rarely been as highly valued as today.

Nothing here suggests a severe global recession is on the way. Indeed, it bears remembering that while capitalist economies have always been cyclical, severe recessions, especially global ones, are rare. It would appear wise, in sum, for everybody “to keep calm and carry on”.

Yet there is a catch — a big one. As Ray Dalio of Bridgewater argues in a note on what is going on, the short-term cycle is the least of our challenges. There are also structural changes, which he summarises in terms of differential productivity trends, and the long-term debt cycle.

Crucially, these developments have made the world economy fragile.

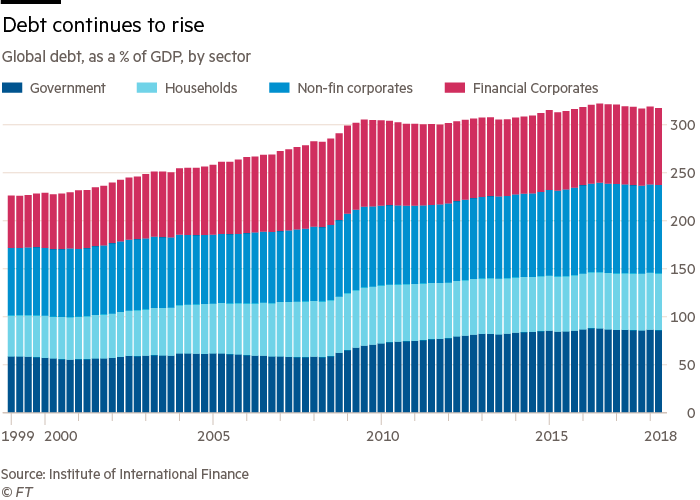

“Productivity” should be viewed as a shorthand way of summarising the shifts in global economic power, widening inequality, collapse in employment in manufacturing, rise of the digital economy and the “savings gluts” of past decades. The long-term debt cycle, which accelerated from the 1980s, was, among other things, a way to manage the social and economic consequences of those structural shifts.

These structural shifts have had big political effects: a surge in nationalism and populism, Brexit, the election of Mr Trump, a trade war between the world’s two most important economies and an erosion of the liberal global economic order. The long-term credit cycle reached its denouement in the disastrous financial crisis of 2007-08. Today, China, whose long-term debt cycle accelerated after the crisis, is reaching the limits of debt accumulations, too.

These long-term conditions significantly constrain any optimism one feels over a short-term cyclical slowdown.

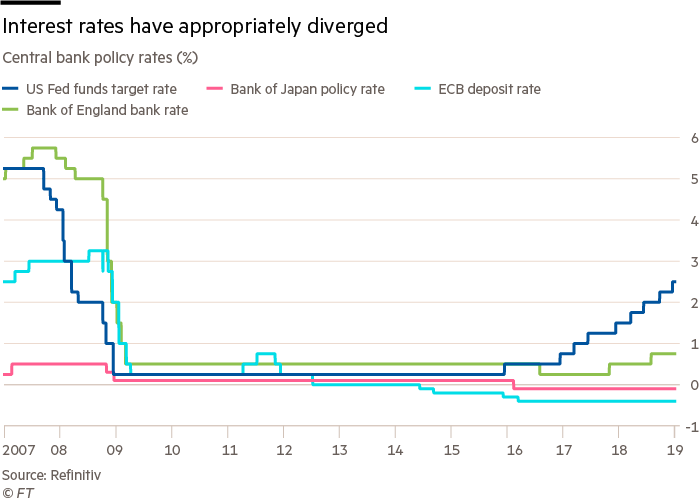

A powerful implication is that room for a response to a recession would be limited by historical standards, especially in monetary policy. If the US Federal Reserve had to make a standard response to a significant recession, its short-term rates might need to be minus 2.5 per cent. The European Central Bank and Bank of Japan would have to go further still. If the worst came to the worst, the Fed and the ECB might be forced to follow the BoJ into even more deeply unconventional policies. While the People’s Bank of China has more room for manoeuvre, reigniting China’s credit boom carries longer-term risks.

The transformation of the global environment brings further dangers, both negative and positive. The biggest negative risk is that it would be impossible to mount a co-ordinated and effective response to a severe global economic slowdown. One obvious positive danger comes from the possible unmanageability of the past accumulations of private and public debt. Another danger is that a breakdown in the global political order creates severe economic disruption on its own, perhaps through a collapse in trade, perhaps as a result of another geopolitical event.

The issue to worry about then is not the state of the short-term cycle. It is perfectly likely that there will be a modest and manageable slowdown, with nothing much damaged as a result. The worry must rather be over the context in which such a slowdown might occur. It is the political and policy instability, combined with the exhaustion of safe options for credit expansion, that would make handling even a limited and natural short-term slowdown potentially so tricky.

Unfortunately, no simple mechanisms for reducing these sources of fragility now exist. These are deeply ingrained and, given recent political developments, are more likely to get worse than better. If you do want to worry, you should worry about that.

0 comments:

Publicar un comentario