Think Local When It Comes to China’s Debt

One of the biggest areas of vulnerability in China’s huge debt pile is bonds issued by investment vehicles linked to local governments.

By Andrew Peaple

A woman walks at the construction site of a 'red tourism' attraction featuring Chinese Communism, in Shazhou village located in Hunan province, China on Dec. 3. Photo: shu zhang/Reuters

All politics is local, runs the old saw. In China, local governments lie at the root of the country’s debt problem—a problem likely only to grow in 2019.

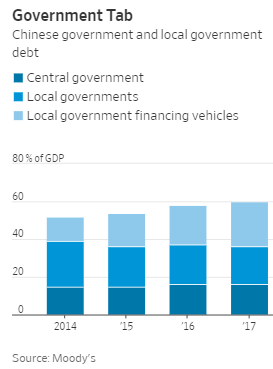

Most analysts see the Chinese government’s relatively low debt—equivalent to around 16% of GDP at the end of 2017, according to Moody’s—as a strength. But add in both official local government debt, and debt issued by off-balance sheet financing vehicles backed by local governments—known as LGFVs—and that ratio climbs to 60% of GDP.

These LGFVs, which started sprouting up after the global financial crisis, have become an area of huge vulnerability. Back then, Chinese local governments were restricted from issuing their own debt, but still needed to stoke the economy. The solution: set up off-balance sheet vehicles which could issue debt, often collateralized with local government-owned land, and spend the money raised on big investment projects.

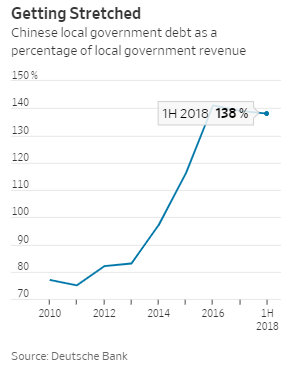

In recent years, local governments have become freer to sell their own official debt, but they still face centrally-imposed limits on how much they can issue. With tax revenues declining as Chinese growth slows, and another of local governments’ big income sources—land sales—highly volatile, they face an annual funding gap equivalent to around 10% of China’s GDP, Moody’s reckons.

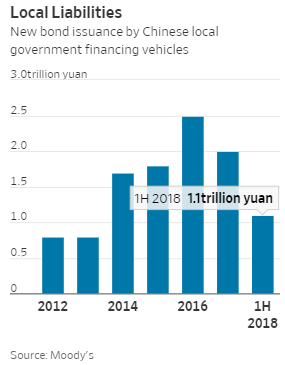

This persistent revenue shortage has left local governments still reliant on LGFVs to keep issuing debt to fund investment. LGFV bond issuance has grown rapidly this decade; and despite a dip last year, it reaccelerated in the first half of 2018.

Cracks in this system are starting to show. A big concern is that many of the investments LGFVs have made over the years can’t and won’t generate adequate returns. Beijing’s crackdown on shadow banking has put the squeeze on investing entities that have been big buyers of LGFV debt. In turn, funding costs have been rising, particularly for lower-rated LGFVs, meaning interest payments are becoming an ever greater proportion of local government spending, particularly in poorer areas of China.

A big question now is who will bear the fallout if—as many analysts expect—LGFVs start defaulting on bond payments in big numbers. Investors have long assumed these financing vehicles have implicit backing from local governments and, ultimately the central government. Beijing, though, has been trying to dispel that impression, with a series of measures imposed to cut the potential support from local governments to the LGFVs.

If Chinese regulators allow a spate of defaults on debt long believed to be quasi-government, confidence in China’s bond market—vast swaths of which are priced as if they have Beijing’s ultimate backing—could plummet. Conversely, heavy government bailouts would lead to a reassessment of Chinese central government debt levels, and hence a potential repricing of government bonds.

Either way, the hangover from China’s local government debt binge is about to get very interesting.

0 comments:

Publicar un comentario