The Cycle's Last Stand

by: SA Marketplace

Summary

- We zoom out for the year-end Marketplace roundtable to look at the macro environment. Does Q4 2018 foretell a shift?

- There's consensus that the current economic cycle is drawing towards an end, but the Fed's exact role remains up for debate.

- Bonds, emerging markets, and perhaps a last leg of the equity bull market stand out as possible directions to watch for in 2019.

- There's consensus that the current economic cycle is drawing towards an end, but the Fed's exact role remains up for debate.

- Bonds, emerging markets, and perhaps a last leg of the equity bull market stand out as possible directions to watch for in 2019.

2018 seems to be ending on the wrong note in the markets. December is setting the wrong kind of records, and Q4 has been a bumpy one in general. This is what happens in the stock market sometimes, but it's been easy to forget over the decade-long bull market.

We're using the end of the year as a chance to lift our heads, survey the market, and see what might be coming ahead. To do so, we're inviting our Marketplace authors to do a series of roundtables. 2018 was another steady growth year for the platform, and we have a lot of great voices on the Marketplace, so we wanted to share their perspective with you.

Our Year End Marketplace Roundtable series will run through the first full market week in January. We'll feature ten different roundtable discussions, with expert panels chiming in on Tech, Energy, Dividends, Other Income strategies, Gold, Value Investing, Small-Caps, Alternative investing strategies, Biotech, and the Macro outlook.

This roundtable looks at the macro climate and the big picture. The Fed, the state of the economy:

- Eric Basmajian, author of EPB Macro Research

- Topdown Charts, author of Weekly Best Idea

- Avi Gilburt, author of The Market Pinball Wizard

SA: Rates have gone up steadily in the US, and that has seemed to have repercussions. What has mattered most about the Fed's behavior in 2018? (question asked before the December fed meeting)

Eric Basmajian: The biggest mistake the Federal Reserve made in 2018 was tightening monetary policy into a global and now domestic economic slowdown. The global economy empirically peaked in January of 2018 while the US economy peaked in Q2. In year over year GDP terms, growth actually peaked in Q3 for the US, but 75% of the third quarter gains were inventory and government spending, so the underlying economy peaked in Q2. When the economy slows, long-term yields fall. As the Fed tightened policy into a slowdown, long-term rates fell as short-term rates pushed higher, flattening and inverting parts of the yield curve. Inversions in the yield curve cause dramatic slowdowns in bank lending and shadow banking which manifests itself in the form of slower economic growth 2-4 quarters in the future. In 2019, the US economy will suffer the consequences of Fed policy in 2018; the slowdown has just started.

Topdown Charts: Quantitative tightening has been the bigger, and up until recently, more underappreciated issue in my view. Add to that the tapering by BOJ & ECB and we've seen developed market effective/shadow composite rates up over 200bps vs. the some 90bps on a headline basis. Make no mistake, central banks are moving to become sources of volatility rather than supressors of volatility.

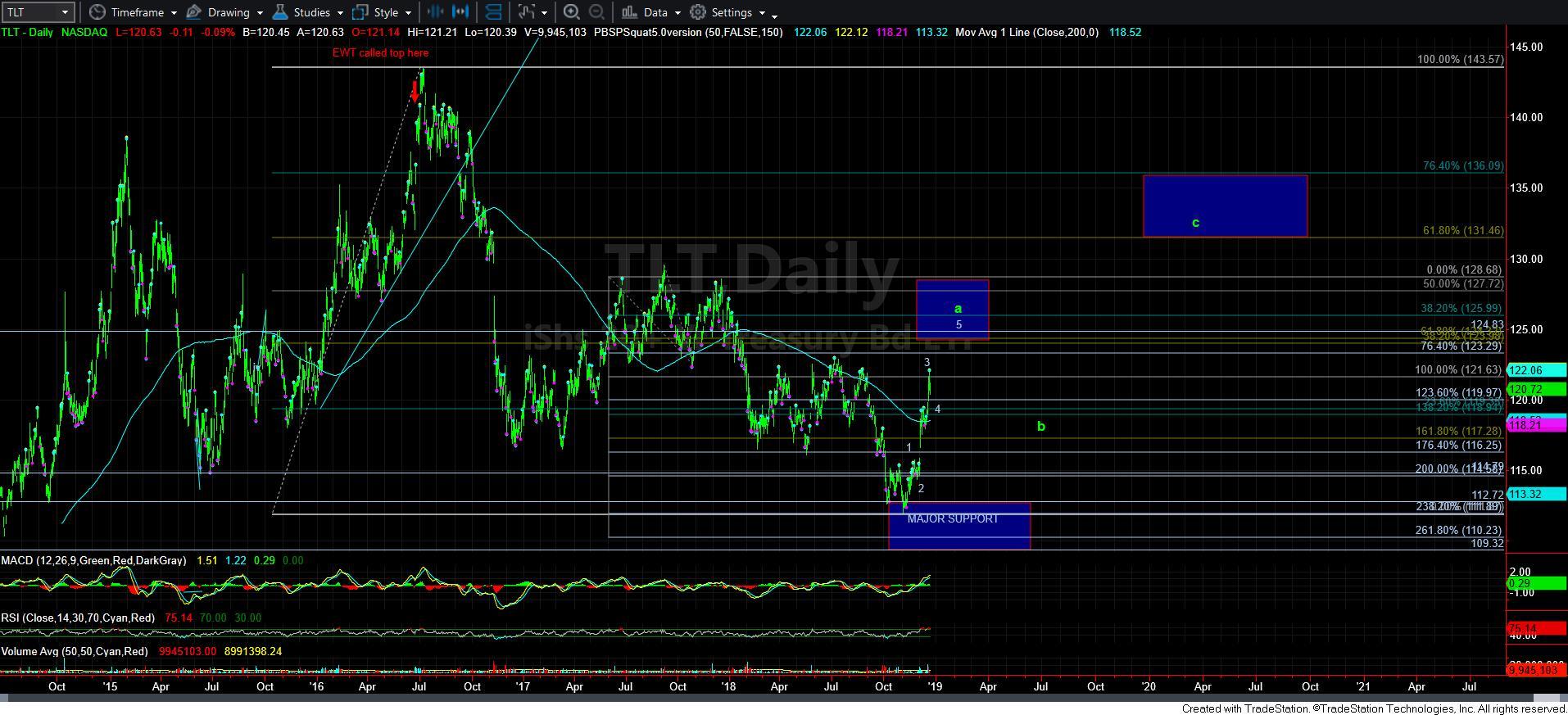

Avi Gilburt: I do not view the Fed as significant as many others. In fact, as the Fed was expressing its intention to continue to raise rates, I was suggesting a long position in the TLT when we struck 113. Moreover, my minimum target over the next year or two is the 131 region in the TLT. So, no matter what the Fed does or does not do, I think the market will overpower the Fed when it comes to rates.

Source: Avi Gilburt

Source: Avi Gilburt

SA: Where do you think the Fed or interest rates go from here in 2019 and beyond?

Eric Basmajian: In the long run, interest rates follow the trending direction in growth and inflation. From 2016 to 2018, real GDP accelerated from 1.3% year over year to 3.04% (Q3 2018) which caused interest rates to rise across the entire Treasury curve. Now that growth and inflation have peaked and are decelerating, we can expect the Federal Reserve to back off future monetary tightening and for long-term rates to move lower as well. Interest rates across the Treasury curve will move lower, following the rate of change in growth and inflation.

Topdown Charts: Expect ongoing QT and rate hikes next year, with a recommencement of QE when the next recession hits.

Avi Gilburt: Over the next year or two, I expect rates to pullback. As I noted, I bought TLT at 113, and expect it to rally to at least the 131 region.

SA: 'Late Cycle' was one of the phrases of the year in the market. Do you view that as an accurate description of the current market and economic cycle, and why or why not?

Eric Basmajian: Yes. Currently, the US economy is in the "maturity" phase of the economic cycle. Early indicators that the economy has peaked include a slowdown in housing, auto sales, and durable goods consumption or "big-ticket" consumption. Those three specific sectors lead the economic cycle because they are large line items in the consumer basket and often require interest rate financing. As interest rates rise, these sectors are hit first, and then employment in the housing and auto industry slows, perpetuating the end of the economic cycle. We have seen a very notable decline in home construction, specifically building permits which are down 8% from their peak as well as auto sales. The next place this economic slowdown will appear is in the employment market, specifically in the average work-week length and aggregate hours.

Once the slowdown appears in the employment market, we will be moving past "late cycle" and moving closer to the official end of the cycle.

Topdown Charts: The big debate is as to whether we are late cycle or end cycle. I think late cycle, but I am closely monitoring a couple of key charts on a global level, which to be fair are flagging risks of a slowdown.

Avi Gilburt: I view the stock market as having started its latest bull-cycle in 2009. And, since I utilize Elliott Wave analysis, wherein we view bull trends as taking shape within 5 waves.

Currently, I see us as being within the 4th wave of that 5 wave structure off the 2009 lows. And, once we complete this 4th wave correction, I see a rally to at least the 3225SPX region in the years to come. That last rally will complete this bull cycle off the 2009 lows.

SA: It's easy to over-dramatize the times we live in, so that 2018 seems like the most 'fill in the adjective' year ever. How does this moment in time compare to other market cycles or moments you have lived through or study? Are there lessons we can draw from history to guide us in 2019?

Eric Basmajian: I take a less over-dramatized approach. Put quite simply, when the Federal Reserve tightens monetary policy during an economic slowdown, assets respond negatively. We can look at all the periods of Federal Reserve monetary tightening for a proxy on how this cycle will end. When growth is accelerating, as it did from 2016 to 2018, monetary tightening is relatively painless. As soon as growth starts to decelerate, monetary tightening becomes catastrophic. I am not referring to "strong" growth or "weak" growth; those are opinions. Accelerating or decelerating rates of growth are empirically measured facts. When growth is accelerating, the market can handle tightening. When growth is decelerating, as it is now, and the Fed is tightening, move out of the way.

Topdown Charts: Sticking to recent history one thing I would highlight is how big a contrast the end of 2018 is to 2017: at the end of 2017 we saw increasing overvaluation across assets and markets, significant optimism on the markets and economy, and a sense of complacency. Right now, we have much cheaper valuations, increasing pessimism, and even signs of panic in some indicators. This contrast should make contrarians prick up their ears.

Avi Gilburt: I believe that the market is fractal in nature. This means that these movements are variably self-similar at different degrees of trend. In other words, the impulsive and corrective movements of the market are occurring at all degrees and in all time frames. So, if one truly understands the underlying nature of the market, history is constantly repeating itself.

And, to quote R.N. Elliott:

“The causes of these cyclical changes seem clearly to have their origin in the immutable natural law that governs all things, including the various moods of human behavior. Causes, therefore, tend to become relatively unimportant in the long term progress of the cycle. This fundamental law cannot be subverted or set aside by statutes or restrictions. Current news and political developments are of only incidental importance, soon forgotten; their presumed influence on market trends is not as weighty as is commonly believed.”

SA: What was the big story or lesson learned for you in 2018?

Eric Basmajian: Significant increases in government spending cannot change the economic cycle but can prolong an acceleration phase or delay the transition into the latter stages of an economic cycle. The global economy peaked in Q1, as the US economy should have. Massive fiscal spending, captured in the GDP report, delayed the slowing of US GDP for two quarters and had a more substantial impact that was initially thought. This delayed the decline in long-term interest rates that we are currently seeing that should have more than likely started when the rest of the world peaked in Q1.

Topdown Charts: Pay attention to the charts, and be constantly on a mission to improve and expand your analytical process. I missed or was slow to change on a couple of things (opportunity to improve), but managed to get ahead of and nail several market calls on the back of a chart/data driven process. That and don't count out the macro picture!

SA: What are you preparing for in 2019? Any big themes to watch out for?

Eric Basmajian: I am preparing for a continuation of the deceleration in domestic economic growth. Growth in Q4 will be lower than Q3 and the first quarter of 2019 will show headline inflation below 2% and economic growth significantly slower than 2018. Asset prices will respond negatively at the start of Q1 to decelerating rates of growth and inflation.

Topdown Charts: Looking forward, the theme of “transitions” I think captures a lot of the major moving parts: a transition for central banks from suppressors to sources of volatility, rotation across assets and markets, and a transition stage in the business/market cycle. Risk is clearly elevated, but so too is opportunity.

Avi Gilburt: I am looking for a continued rally in bonds, whereas I am also preparing for the opportunity to move back into the stock market. In August and September, I began to "emotionally" prepare my subscribers for the stock market topping out and beginning a 20-30% correction. And, when the S&P500 broke 2880SPX, I noted that I was moving to cash. I am looking for the opportunity to get back into the market in 2019 for the last phase of the bull market which should take us up to at least the 3225SPX before the bull market which began in 2009 completes.

SA: What's your favorite idea to have in your portfolio or to position your portfolio, and what's the story?

Eric Basmajian: Investors should continue to position defensively relative to their asset allocation strategy. The best idea is long-term Treasury bonds. Long-term interest rates follow the trending direction in growth and inflation, and with economic trends moving lower, long-term bonds will gain. Don't let bonds fool you. There can be massive capital appreciation with bonds too. As a reminder in 2014, long-term bonds, expressed through ETF (EDV), rose 45%.

Topdown Charts: The stars are aligning for emerging market equities, particularly relative to developed markets. Valuation, sentiment, technicals, and cycle indicators are all coming together to create a potential stellar year or even couple of years for emerging markets. Though they have taken a lot of pain this year, that's actually been a key part of the setup. I also like commodities and China A-shares for similar reasons.

0 comments:

Publicar un comentario