Should You Trust This Rally? Dr. Copper May Have The Answer

by: Eric Basmajian

Summary

- Has the market bottomed or is this a dead cat bounce?

- Growth sensitive commodities are not as euphoric as the stock market.

- Have the growth fears really disappeared already?

Should You Trust This Rally? Dr. Copper May Have The Answer

The S&P 500 (SPY) has now rallied about 10% off the Christmas Eve low as all the fears that caused the sell-off have magically vanished. As the market was tumbling, fears of a global economic slowdown (and a domestic slowdown) in addition to a Federal Reserve that had perhaps pushed too far and the sideshow of trade wars and political theatrics pushed the market lower in a seemingly relentless decline.

Fast forward roughly two weeks, the S&P 500 is about 10% higher and all of the aforementioned fears are gone as the Federal Reserve members stumble over each other to find out who can capitulate the farthest in the dovish direction. Most Fed members advocated for 2-3 rate hikes this year going back as early as November of 2018. Today, less than two months later, there is a race to see which Fed member can become the most dovish, with consensus shifting towards zero rate hikes this year and a strong likelihood of adjusting or pausing Quantitative Tightening "QT."

Fed Near Term Forward Spread:

Source: Bloomberg

Tangent aside, the real question we should be asking in regards to this 10% equity market bounce is whether or not this is a dead cat bounce or a bear market rally (or something similar to that) in which a visit of the recent lows is in the cards, or if all the previously mentioned factors that caused the market decline have since gone away and we are back to the bull market.

At EPB Macro Research we are uniquely focused on getting the trending direction of global and domestic growth right and not at all worried about trade wars or political theater. Following growth trends allowed us to position defensively in the summer of 2018 and even get short financial sectors such as regional bank ETF (KRE), before a large 30% decline.

Investors have a choice regarding this equity rally now that most of the fear is out of the picture. At EPB Macro Research the question can be simplified to growth. Is growth bottoming and starting to re-accelerate? If so, it is certainly time to buy the market. If not, and growth is still decelerating, then this rally will likely fade as the market catches back down to the reality of the underlying growth trends that have not changed.

We will take a look at industrial metals for a read on the trends of global growth.

Industrial metals provide critical insight into the trending direction of global growth, specifically out of China, one of the world's largest growth engines. A sustained decline in industrial metals is a clear sign that industrial activity has cooled substantially and a leading indicator of slowing growth.

One of the industrials metals to watch is copper, or more famously known as Dr. Copper, for the unique ability to diagnose global growth trends.

First, looking at the Bloomberg index of industrial metals shows growth is likely still decelerating around the world. In 2014, the industrial metals index was declining rapidly, foreshadowing the economic slowdown to come in late 2015-2016.

The industrial metals index bottomed and started to move higher in late December and early January 2016 when the stock market did not bottom until mid-February, a nice lead.

While the US stock market did not peak until Q3 of 2018, the global economy and global stock markets started to decline in Q1 of 2018, just after the industrial metals index broadly rolled over and started to signal yet another global slowdown in growth.

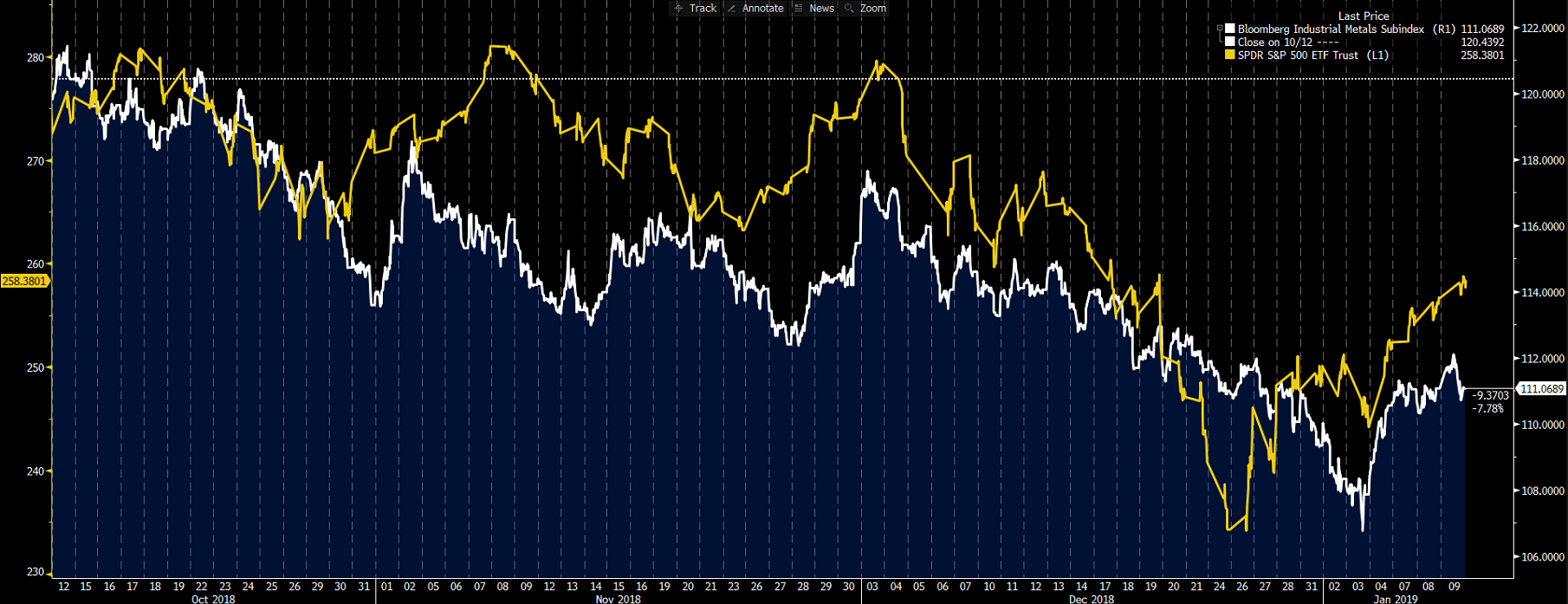

Bloomberg Industrial Metals Subindex:

Source: Bloomberg

While the equity market has continued to rally, the industrial metals index has stopped moving higher and actually declined yesterday (Wednesday), a sign that this rally may have more to do with a short-squeeze than a fundamentally driven move higher.

Source: Bloomberg

The doctor shows a similar long-term path, rising as the global economy accelerated from 2016 through late 2017 and subsequently making a top in early 2018 before declining notably as the global economy decelerated.

Copper Future:

Source: Bloomberg

Industrial metals are saying it is very premature to think this rally in the S&P 500, and risk assets alike has to do with the underlying fundamentals improving.

The Federal Reserve has completely capitulated and moved from three rate hikes to zero hikes plus altering QT in a matter of two months. It should be abundantly clear at this point that the Fed is stock market dependent rather than data-dependent.

Putting The S&P 500 Into Context:

Source: Bloomberg

As long as growth continues to decelerate globally and domestically, it is a risky time to buy the market as another large drawdown is likely in that scenario. If growth bottoms and starts to re-accelerate, I will be the first person to start adding equities to the long side as risk-assets love accelerating growth.

The trends in industrial metals and Dr. copper more specifically, while just one indicator, firmly suggest that there has been no substantial pick up in growth and this rally in the market is more than likely a bear market bounce as a result of a short-squeeze caused by a dovish capitulation by the Fed.

If the market continues to move higher and industrial metals stage a multi-week reversal and move notably higher, I will check the direction of global growth across all indicators and position accordingly. For now, I'd need to see a lot more evidence that things have changed between December and today before getting excited about this 10% bounce after a 20% decline.

0 comments:

Publicar un comentario