Jeff Bezos and Jamie Dimon: Best of Frenemies

The JPMorgan chief and Amazon founder have found their companies’ fortunes increasingly entwined, but the balance of power between their firms has shifted

Nigel Buchanan

JPMorgan JPM 3.69%▲ Chase & Co. Chief Executive James Dimon assembled a team in 2017 to answer a question that had been nagging at him for a while: “How should we think about Amazon?”

The team explored the ways Amazon.com Inc. AMZN 5.01%▲ could muscle into financial services and where JPMorgan could fit in, according to people familiar with the matter. And what if, as Wall Street has long feared, the tech company were to become a bank itself?

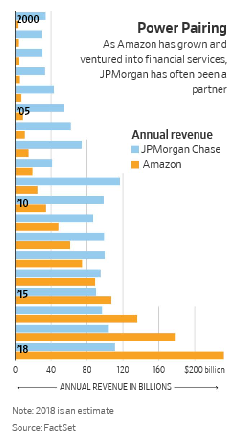

Industries from pharmaceuticals to logistics are grappling with the Amazon question, as the retailer relentlessly expands into new business areas. But in many ways, the online retail giant and the nation’s largest bank by assets have a special relationship.

The fortunes of the two companies have become more entwined over the years. They are closely connected through a credit-card deal struck when the retailer was still mostly selling books and CDs on the internet. JPMorgan is in talks to partner with Amazon on a number of financial ventures, and the bank lends to the tech company. With Warren Buffett’s Berkshire Hathaway Inc.,the companies are working on a first-of-its kind venture to lower health-care costs for their hundreds of thousands of employees. Increasingly, JPMorgan has begun to emulate some of Amazon’s signature management practices.

Mr. Dimon and Jeff Bezos, Amazon’s founder and CEO, have also become friendly over the past two decades, even as their business interests have at times been at odds, and despite some differences in their personal styles.

Mr. Dimon, 62, has spent most of his career in finance. At JPMorgan, he’s focused on maintaining a fortress balance sheet meant to protect the bank from big shocks. Detail-obsessed and focused on keeping costs in check, he often tucks a follow-up list in his pocket.

Mr. Bezos, 54 years old, worked in finance at D.E. Shaw early in his career before founding Amazon in 1994. Mr. Bezos is an advocate of small, independent teams pursuing individual mandates, and emphasizes constant action and long-term thinking. He says his primary job each day as a senior executive is to make a small number of high-quality decisions.

As the relationship between the men and their companies deepened, the balance of power shifted in Amazon’s favor. The retailer’s market value—at $770 billion—now dwarfs JPMorgan’s $335 billion. The bank, used to being the heavyweight in the room, is trying to figure out how Amazon fits into its world and how to avoid becoming its latest casualty.

JPMorgan has adopted Mr. Bezos’s “Customer Obsession” mantra, which commands employees to start with the customer and work backwards when developing products and services, employees said. In September 2017, the bank hired Amazon executive Marbue Brown to oversee customer experience in its consumer bank and wealth-management business as part of its internal Customer Obsession initiative.

Mr. Bezos notoriously banned slide presentations to keep Amazon in startup mode as it grew, instead asking employees to craft six-page documents complete with a press release and FAQs. Over roughly the past 18 months, JPMorgan has started a similar practice in its consumer businesses under Gordon Smith, the bank’s co-president and co-chief operating officer, those employees said.

JPMorgan’s relationship with Amazon stretches back to at least 2002, when Chase began issuing the online retailer’s co-branded card. The deal predates Mr. Dimon, who joined JPMorgan in 2004.

A few years earlier, Mr. Bezos had tried and failed to hire Mr. Dimon to be Amazon’s president. Mr. Dimon, recently fired from Citigroup Inc.by his mentor, Sanford “Sandy” Weill, flew to Seattle to have lunch with Mr. Bezos. Mr. Dimon has said it wasn’t the right time to make such a dramatic change.

“I had this vision I’d never wear a suit again, I’d live in a houseboat like Tom Hanks” in the movie “Sleepless in Seattle,” Mr. Dimon told CNBC in July.

Over the two decades that followed, Amazon’s sales exploded. So did its clout.

About two years ago, when it came time to renegotiate the card agreement, Amazon was in a position to extract painful concessions.

The Amazon Prime Rewards Visa Signature Card—one of two Amazon credit cards issued by JPMorgan—pays 5% cash back on Amazon purchases to members of the retailer’s Prime service (Whole Foods was added later). The bank agreed to share a far higher percentage of card revenue with Amazon than it had previously, according to people familiar with the matter.

The bank’s executives knew the card wouldn’t be a big money-maker, and some internal projections even showed short-term losses on cards issued in the months following the deal, some of the people said. After a lengthy debate, Mr. Dimon signed off on the deal; the relationship with Amazon—one of JPMorgan’s top five corporate clients—was simply too important.

The two companies worked closely to boost card spending, both on and off Amazon. A 2017 holiday-season spike in Amazon sales put the card closer to the red for JPMorgan. The card is currently profitable, people familiar with the matter said.

Underlying these shifting power dynamics is the question of whether Amazon might someday make its own move into financial services. So far, Amazon largely has stayed off Wall Street’s heavily regulated turf, and it’s not currently plotting an entry into the banking business, people familiar with the matter said.

Still, Mr. Bezos and other Amazon executives have long realized that financial services are key to the company’s success, in large part due to the company’s core online retailing business, according to people familiar with the matter. Early on, executives realized they were at a key disadvantage to brick-and-mortar rivals because merchants tend to pay lower fees on in-person credit-card purchases.

For years, Amazon has worked to find ways to cut down on those fees, and executives have been focused on evolving the future of payments, making it as frictionless as possible, the people said. Mr. Bezos has stressed the importance of financial services and payments to some senior executives, according to some of the people.

In 2017, it introduced Amazon Cash, which allows customers to load cash onto their account balance account at thousands of convenience, grocery and drug stores, as well as Coinstar kiosks. The move was seen as key to helping it acquire low-income and so-called underbanked consumers, who would otherwise have difficulty shopping on its site. It’s also been exploring the development of its AI-assistant Alexa to offer more payment options, like telling it to pay for gas at the pump or send money to a friend—something executives see as key to the way consumers will bank in the future, according to the people. And it’s loaned more than $3 billion to small businesses selling on its site via its Amazon Lending arm.

Most importantly, the company has been building out Amazon Pay, its digital wallet that consumers use at outside merchants for payment on their sites. Amazon has quietly been trying to convince merchants to add it to brick-and-mortar locations, according to the people, something that could allow it to one day challenge Apple Pay. Amazon is looking to Asia, where mobile wallets like Alipay and WeChat Pay are commonly used. Amazon executives want to gobble up the U.S. market while the competition remains fairly minimal, according to the people.

It’s part of a broader battle playing out between technology companies, including Amazon, Apple Inc.and Alphabet Inc.’sGoogle, to become bigger forces in consumer payments. Amazon’s efforts could result in new competition among these companies and could also be a challenge to PayPal Holdings Inc.’sVenmo and big banks that have been trying to boost usage of their own person-to-person payments service Zelle.

While the balance has shifted in Amazon’s favor, JPMorgan has some things the tech company wants: an extensive payments infrastructure and a financial relationship with half of all U.S. households.

In an on-stage interview last year at Southern Methodist University, Mr. Bezos was asked about business role models and pointed to Mr. Dimon.

“If I were a big shareholder in JPMorgan Chase, I would just show up every Monday morning with, like, pastries and coffee for Jamie, and I’d be like, ‘So you happy? You good?’” Mr. Bezos said. “Because I think he’s a terrific executive in a very complicated company.”

Amazon has partnered with the bank to expand Amazon Pay, which allows consumers to use the credit card or other payment option they have stored on their Amazon.com account to pay for purchases at non-Amazon merchants, joining ChaseNet, the bank’s own payments network under a years-old deal with Visa Inc.,according to people familiar with the agreement. Merchants that are a member of ChaseNet can also receive preferable pricing terms from Chase.

That means, for instance, if a consumer shops with a merchant outside Amazon using a Chase credit card loaded into Amazon Pay, the merchant will pay lower transaction costs as long as it also uses Chase to clear its transactions. These types of perks are meant to encourage merchants to adopt Amazon’s wallet, one of the people said.

JPMorgan also has been in talks with Amazon about building a checking-account-like product the online retailer could offer its customers, The Wall Street Journal reported in March. The service would build on Amazon Cash’s efforts to target younger customers and those without bank accounts.

The lure for JPMorgan is access to Amazon’s enormous user base, including its tens of millions of U.S. Prime members. Amazon, meanwhile, wants to forge a deeper connection with customers who already use its platform to shop, read and stream videos.

Regulatory queries have complicated the project, according to people familiar with the negotiations, and it’s unclear if it will materialize with JPMorgan or any other bank.

Amazon’s virtual assistant, Alexa, is a sensitive spot in the relationship. Capital One Financial Corp., American Express Co., US Bancorpand some other banks allow customers to access their financial information through Alexa, but privacy concerns have kept JPMorgan largely on the sidelines.

JPMorgan began talking to Amazon about developing an Alexa voice application, or skill, related to retail banking customers a few years ago, but the discussions stalled last year, according to people familiar with the matter. Bank executives are concerned about how Amazon might use some of the data gathered from Alexa, which transcribes user conversations with the AI system, the people said.

Amazon already allows certain developers to remove sensitive information from the Alexa app for things like voice passwords. The company has said it undertakes rigorous security reviews and encrypts communications for its devices and does not use the data to target ads or make product recommendations.

Still, some recent Alexa mishaps have raised concerns. Last year, for example, an Echo device accidentally sent a recorded conversation to a user’s contact without permission. Amazon said at the time that, as unlikely as the event was, it was working to make it less likely.

0 comments:

Publicar un comentario