Oil Bull Thesis Attacked From All Sides As WTI Falls Below $50

by: HFIR

Summary

- WTI falls below $50/bbl as the oil bull thesis is attacked from all sides.

- We explain that these two variables cannot co-exist, U.S. oil production growth of 2 mb/d and sub $50 WTI.

- But the crazy thing is even if you assume a stellar U.S. growth figure, the world will still be in undersupply in 2019/2020.

- In the short-term, we can look stupidly wrong on our thesis, but fundamentals will matter. We stand by our numbers.

- We explain that these two variables cannot co-exist, U.S. oil production growth of 2 mb/d and sub $50 WTI.

- But the crazy thing is even if you assume a stellar U.S. growth figure, the world will still be in undersupply in 2019/2020.

- In the short-term, we can look stupidly wrong on our thesis, but fundamentals will matter. We stand by our numbers.

Welcome to the attack from all sides edition of the Oil Market Daily!

Since our ill-fated oil article titled, "Brent Breaks $80: The Oil Bull Thesis Enters The 7th Inning," oil bulls went from the White House to the s*** house. The oil bull thesis went from oil demand destruction is the only valid bear thesis to 1) will President Trump keep a lid on prices? Will trade war cause further demand destruction? Will U.S. shale oversupply the world? Will Iranian sanction waivers result in no decline in Iranian crude exports? Will OPEC cut of 1.2 mb/d be enough?

It's safe to say there are no shortages of worries in the market according to most market participants. Is it so wrong to assume that the whole market has it wrong on oil prices? No, and we would argue there are valid demand growth concerns, but the point the market is clearly ignoring yet again is that you cannot have these two variables co-exist:

- U.S. shale growth of 2 mb/d and

- Oil prices below $50/bbl.

The reality is that despite the craziness of U.S. oil production growth this year, U.S. shale is still at the whims of the volatility of the oil market. Since cost breakevens were already cut to a minimum in the last downturn, there won't be any new innovative cost reduction methods this time around. And since servicing cost inflation is already near cycle lows, there won't be any cost cut incentives from suppliers.

In addition, U.S. shale producers came into 2019 ill-equipped on hedges for next year making capex budgets extra vulnerable to price weakness.

What does this lead to?

It leads to U.S. shale potentially disappointing growth on the downside. But here's what's more ridiculous and this is the point we tried to get across in our article, "U.S. Oil Production Likely To Grow 2 Mb/D In 2019 But Crude Quality Issue Will Get Worse."

Even if you pencil in +2 mb/d from U.S. total liquids growth, we still have a supply deficit in 2019.

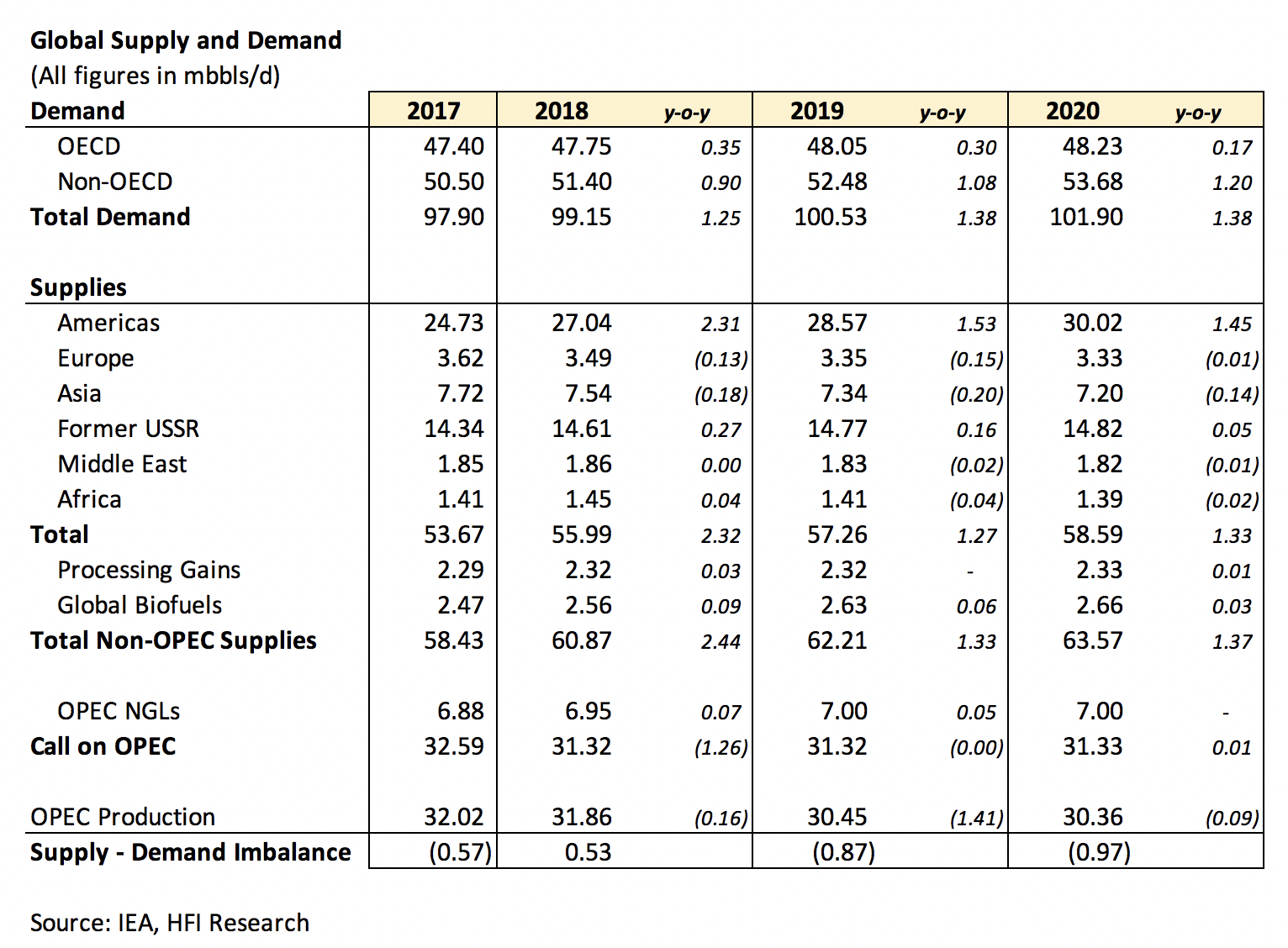

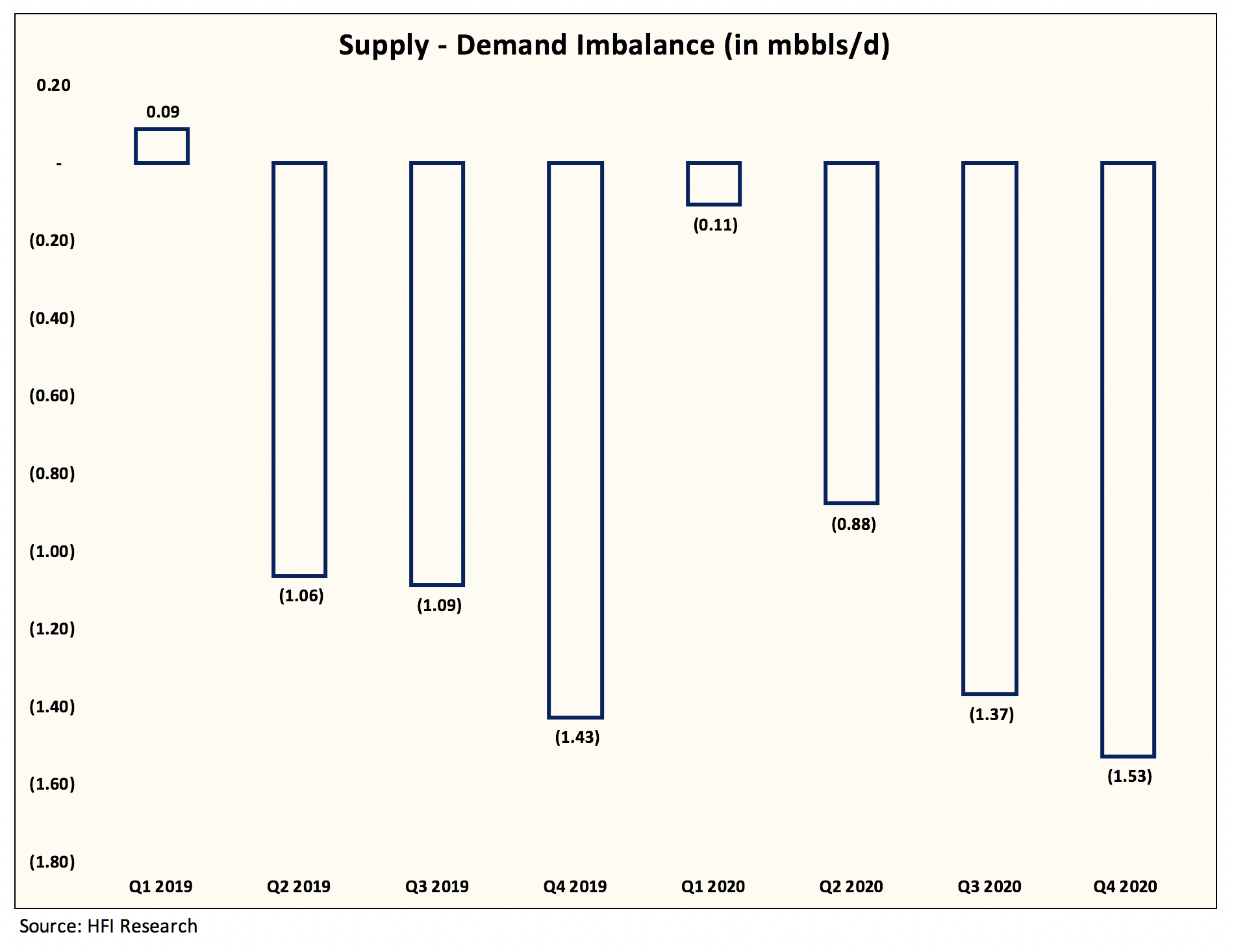

But given the real possibility of U.S. shale at least just stalling in H1 2019, this is what the global supply and demand balance is:

And keep in mind we are using global oil demand growth of ~1.38 mb/d for 2019 and we have global oil demand growth falling y-o-y in Q1 2019 by 1 mb/d.

What this ends up being is a market that will be in serious supply issues by the second half of 2019.

Now of course, OPEC can surprise to the upside with higher production levels, but low oil prices result in more geopolitical chaos. Libya just announced force majure on its largest field resulting in ~400k b/d of loss supplies. But the oil market took that in strides and pushed prices lower by another 5%.

At the end of the day, what we are saying is that yes prices can keep falling for whatever reason that currently grips the market today. But it will eventually have to revert back to fundamentals and the global oil supply/demand outlook for 2019/2020 is that of a market in severe deficit.

With the world ever increasingly reliant on U.S. shale to deliver, just a stalled growth outlook for a mere 6-months will cascade into a deeper deficit down the road. This is why U.S. shale will never be a swing producer because prices can impact its growth.

So yes, we got the Q4 outlook incredibly, massively, disgustingly wrong, but the fundamental outlook has not changed. And while the oil bull thesis is attacked from all sides, we are standing our ground behind our numbers.

0 comments:

Publicar un comentario