Italy’s investors adjust to bond market’s new normal

Debt demand stutters as Brussels and Rome face drawn-out dispute over Budget

Kate Allen in London

After six months of turbulence, investors in Italy’s bond market are acclimatising to the new normal as Brussels and Rome prepare for a prolonged stalemate over the country’s budget.

Earlier this week Brussels announced that Italy’s budget plans were in “particularly serious non-compliance” with previous commitments the country had made, and justified the opening of an “excessive deficit procedure” against the country. That process will last long into next year before any resolution emerges.

Meanwhile this week’s poorly subscribed retail bond sale has dashed the governing parties’ hope that Italian households would provide a fresh source of debt market demand for government paper. The sale raised just €2.2bn over four days, far lower than the usual €7-8bn that BTP Italia sales fetch.

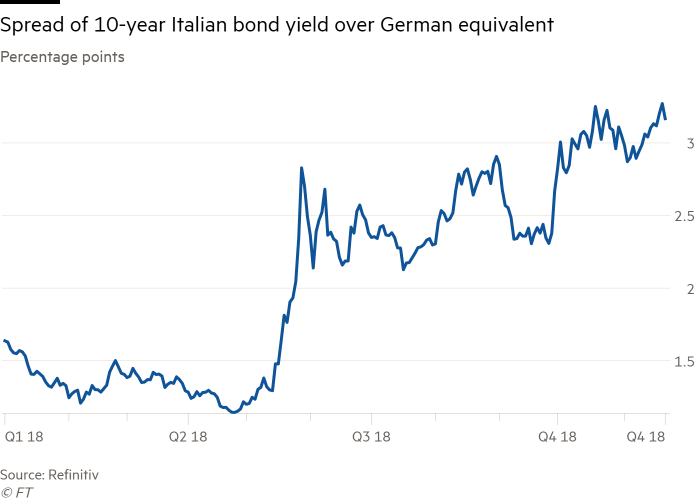

Despite this yields have edged down since the start of the week, with 10-year paper seeing a 7 basis point drop to 3.41 per cent, while its spread over the equivalent German bond yield — a widely watched measure of eurozone risk sentiment — is down 5bp at 306bp.

Yields’ failure to take another significant step higher is being taken by some investors as an indication that the market is settling at around its current level, or could even retrench.

“The excessive deficit procedure will be a long process, and we have probably seen most of the negative headlines that could push spreads wider,” said Adam Kurpiel, head of rates strategy at Société Générale. “In the absence of a major re-widening of global credit spreads, the 10-year BTP-Bund spread should be closer to 200bp than 300bp.”

The next steps in Rome and Brussels’ tango have been well flagged. And for now the questions over investor demand for Italian debt can be postponed, as the country has already raised more than 95 per cent of this year’s funding needs.

With little further drama expected in the coming weeks, investors are in a position to take stock.

“We expect Italian tail risks to abate,” said Peter Chatwell, head of rates strategy at Mizuho, who said that this week’s move by the European Commission “marks the end of this phase of the Italian budget saga”, and the prospect of less intense headline risk “would support BTPs going forward”.

As a result, some investors are venturing back into the market.

Stéphane Monier, chief investment officer at Lombard Odier Private Bank, said there were “good reasons for looking at owning Italian debt right now” given “the market’s overly conservative pricing of Italian political risk and our assessment is that there is no solvency risk for Italy”.

“A lot of the risk is already priced in, with yields closer to those of some emerging economies than other developed economies,” he said.

Lorenzo Codogno, founder of LC Macro Advisors and former chief economist at the Italian Treasury, puts a 70 per cent likelihood on Italy “muddling through until the European elections” next May.

“Interest rates will keep moving higher, amid high volatility, with the 10-year government bond spread within a 300-400bp range, high enough to produce a slow-burning banking and economic crisis but not a major accident,” he said. “After the European elections, the Italian government may well start adopting a more constructive attitude and gradually become more mainstream — however, this is far from granted.”

That leaves investors focused on the economic outlook as one key source of any potential bad news in the coming months.

Italy’s growth prospects have caused heated debate. The country’s premier Giuseppe Conte this week wrote to the European Commission to insist that the country was sticking to its much-disputed forecast for next year of 1.5 per cent.

The IMF forecasts that the Italian economy will grow 1 per cent in 2019, while on Wednesday Italy’s statistics agency cut its economic growth forecast, saying that Italian gross domestic product would grow by 1.3 per cent in 2019.

“If Italy’s growth environment starts to show signs of strain” in the early months of next year, the BTP-Bund spread could face fresh upward pressure, Mr Kurpiel said.

Another risk that Mr Codogno flags is the substantial supply of fresh Italian government debt that bond investors will be asked to soak up next year.

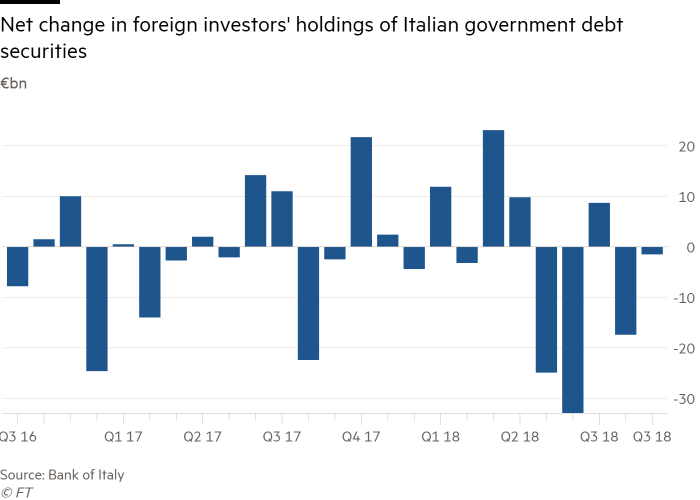

Rome needs to raise about €260bn of bonds in 2019, of which about €200bn will refinance existing paper that is due to mature. That is likely to pose a challenge, as foreign investors have been shedding their Italian bond holdings in recent months.

Foreign investors in Italy’s bond market reduced their holdings by a net €1.5bn in September, taking their total scaling-back since the coalition government took power in May to €68bn, according to figures from the Bank of Italy.

And this week’s bond sale has provided further evidence of the weakening demand for Italian paper.

“There is no risk of an immediate liquidity crisis, but there is a huge issue about flows on a three- to-six month horizon,” Mr Codogno said. “This is not only due to shrinking foreign demand for government paper but also to creeping capital outflows; demand and supply of government paper can only match at much higher yields.”

As a consequence, Italy’s regular debt sales may become investors’ most closely watched indicator — and any plateau in the country’s bond yields may not be long-lived.

0 comments:

Publicar un comentario