Cash back in the spotlight as global bond yields fall

T-bill’s climb threatens headwinds for other markets

Robin Wigglesworth

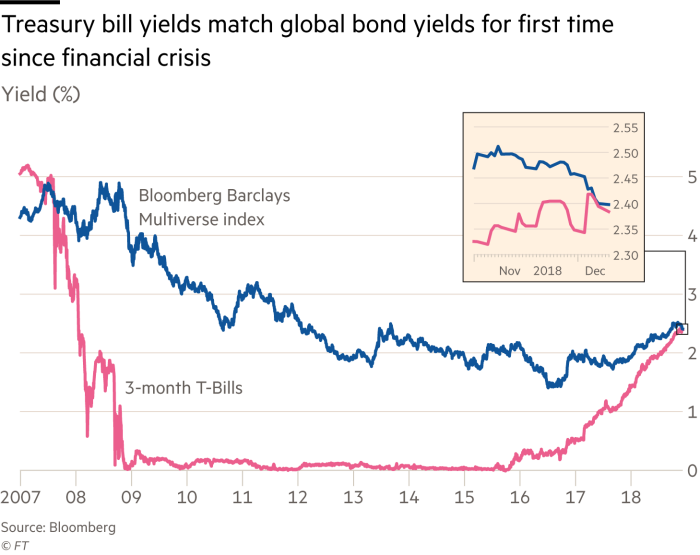

Short-term US Treasury yields have climbed to match global bond markets’ average yield for the first time since the financial crisis, with analysts and fund managers warning that the increasing attraction of cash will be a headwind for financial markets in 2019.

The yield of three-month Treasury bills — the financial system’s closest equivalent to cash — has climbed steadily since the Federal Reserve’s first interest rate increase in late 2015, to a nearly 11-year high of 2.42 per cent last week.

Bond market yields have climbed since their mid-2016 lows, propelled by tighter US monetary policy and expectations that the global economic recovery was broadening and strengthening.

However, the yield of the Bloomberg Barclays Multiverse Index — a broad $52tn benchmark of bonds issued by governments and countries around the world — dipped back to 2.41 per cent last week as investors became glummer on the growth outlook.

The market behaviour highlights how 2018 has become an inflection point in the post-crisis regime, with the era of quantitative easing being replaced by “quantitative tightening” as the Fed shrinks its balance sheet and lifts rates. Add to that the European Central Bank’s effort to trim and, by the end of 2018, end its own QE programme.

Treasury bills have already outperformed global stocks, bonds and commodities this year, an unusual occurrence that some analysts fret could happen again in 2019, as the monetary tide that lifted almost all boats since the financial crisis continues to recede.

“A common theme in this cycle has been the hunt for yield, with investors moving into unfamiliar asset classes searching for higher returns to offset the low yields in core bonds,” JPMorgan Asset Management wrote in its annual outlook. “This isn’t necessarily an incorrect strategy in the early or middle stages of an economic expansion; however, in the late cycle this approach becomes riskier.”

The danger is that the rising lustre of cash dims the allure of other asset classes. While there are currency aspects that mean that the broad, international Multiverse bond index is not directly comparable to short-term Treasuries — let alone equities — investors may be less willing to take on their additional risks when cash returns become more competitive.

While analyst opinions on the coming year differ significantly, most predict it will be even more challenging for financial markets, even as cash continues to do well.

Morgan Stanley’s analysts think government bonds will eke out a 1 per cent gain in the coming year, while equities tread water, and corporate debt loses 5 per cent. However, they predict that cash will return 4 per cent.

0 comments:

Publicar un comentario