Buttonwood

The agony of the value investor

A contrarian strategy fares badly much of the time

.

IN APRIL 1962, Joan Whitney Payson watched the New York Mets, a collection of cast-offs from rival baseball teams, lose their first ever game. Mrs Payson, the Mets’ owner, soon left for a summer in Greece. News of further defeats reached her by telegram. So she asked that she be told only when the Mets won. “That was about the last word I heard from America,” she recalled. The Mets lost 120 of their games that year.

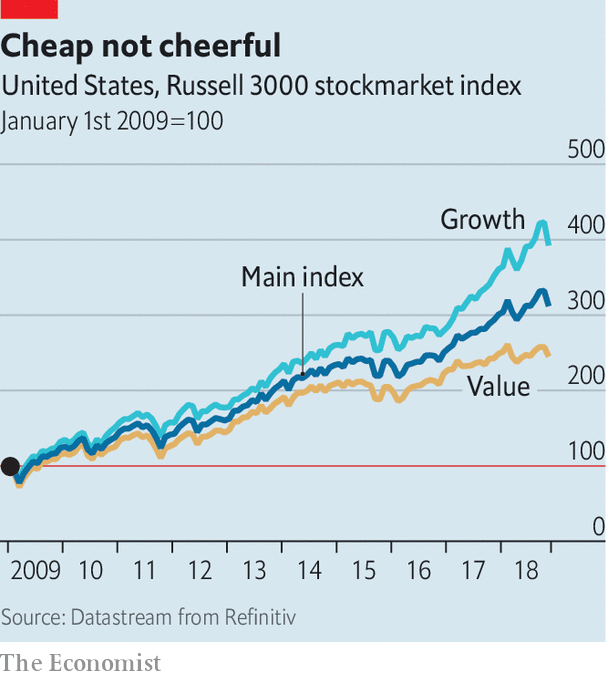

One of the worse things about a losing streak, noted Mrs Payson, is you can never tell when it will end. Investors in “value” stocks know the feeling. These stocks, which are distinguished by a low price relative to the book value of a firm’s assets, have fared badly in the past decade (see chart). A longer run of history, as well as intuition, suggests that buying shares that are cheap relative to their intrinsic worth should eventually pay off. But it can be a long wait before the telegram arrives.

A bad run also breeds doubt. Perhaps the growing importance to the economy of intangible assets, such as brands and ideas, makes book value an unreliable signifier. Similar arguments were made during the late 1990s dotcom boom, only for the value approach to be vindicated.

The truth is that value is a contrarian strategy. That means it fares badly much of the time. Suffering and doubt are the price value investors must pay.

The cardinal distinction between a share’s price and its value goes back to Benjamin Graham, the father of value investing. Price is a creature of the market’s mood, he wrote. In booms, it is set by the greediest buyer; in busts by the most fearful seller. A stock’s value, in contrast, is enduring. It is anchored by the worth of a firm’s assets. The enterprising investor can profit from finding stocks that sell for much less than their value, said Graham. There have since been countless studies showing that value stocks do better than “growth” stocks, their antithesis, over the long haul.

In Graham’s day, the value premium was the prize for finding truly cheap stocks. But computing power has made it easier to compare company accounts. So why might the strategy still work? One reason is that the profits of firms with tangible assets suffer in economic downturns, when costly plant and buildings cannot be redeployed. The value premium is thus a reward for bearing business-cycle risk. Another reason is the mistakes of other investors. They giddily extrapolate the initial success of new and exciting growth stocks. Frumpy value stock gets left behind—until sanity returns.

Still, the recent losing streak is testing the value faith. Perhaps the strategy has stopped working because it is so well known. This idea is dismissed by Cliff Asness, of AQR Capital Management, in a recent essay. The value gap between cheap and dear stocks has not been whittled away. If it had, where was the windfall?

Perhaps the flaws lie with book value. Under accounting rules, factories or office buildings count as capital assets on a firm’s books, because they yield benefits over a long horizon. But spending on R&D and advertising is treated as a running cost, like wages or electricity, even though firms’ know-how and brands are assets, too. That means a lot of real, but intangible, value is missed by price-to-book ratios. Yet serious value funds will rely on a broader set of metrics than just book. And still they suffer.

How much is evident from their anguished letters to investors. Their verdicts are blunt. “Our results have been far worse than we could have imagined,” wrote David Einhorn, of Greenlight Capital, a value-oriented hedge fund, in a recent example of the type. The self is flagellated (“the market is telling us we are wrong, wrong, wrong about almost everything”). And then faith in the investment “process” is sworn afresh. As Mr Asness wryly notes, there is a pinch of “we’re losing because everyone else is an idiot” to all this. But where faith is, there is always doubt. When your strategy loses money, writes Mr Asness, you feel like Casey Stengel, the Mets’ coach in 1962, who, after surveying his team, was moved to ask himself, “Can’t anybody here play this game?”

This agonising is not for most people, says James Montier, of GMO, a fund-management firm: “They don’t want to be wrong for as long as it takes.” Value investors hope to be rewarded for being so out of step with everyone else for so much of the time. But a select few can endure—and even enjoy—it. People of this sort could be heard, a few months into that disastrous first season, saying, “I’ve been a Mets fan all my life.”

0 comments:

Publicar un comentario