Oil majors switch on to a future in power generation

Electricity deals by global groups gather pace amid shift to gas and renewables

Anjli Raval in Madrid

© FT montage

A fuel station on Madrid’s Calle de Alberto Aguilera offers a glimpse into the future. Customers can pick up Amazon packages and gourmet groceries, drop off their hybrid car-share or sip a café con leche as they wait for their electric vehicle to charge.

While regular petrol-guzzling cars are welcome, Repsol — the Spanish oil major that operates the station — is preparing for a global shift in energy consumption as people turn away from dirtier fuels. This is forcing the majors to reimagine their businesses.

“Power is going to be one of the main drivers of new low-carbon business models for all major energy companies,” said Antonio Brufau, Repsol’s chairman, in an interview with the Financial Times. Electricity would “account for most of the primary energy growth”, he added.

Repsol and European rivals Royal Dutch Shell and Total are now making deals along the electricity supply chain — from power generation to electric charge points — echoing the existing drilling rig-to-petrol-pump model.

Penetrating the market for household energy supply, which has previously been dominated by utilities, is where they see future growth.

“It’s a hedge for these companies. No one knows how the energy transition plays out or at what speed,” said Tom Heggarty, of consultancy Wood Mackenzie’s power and renewables division.

“There is a belief they need to evolve with the market so they do not fade away into obscurity.”

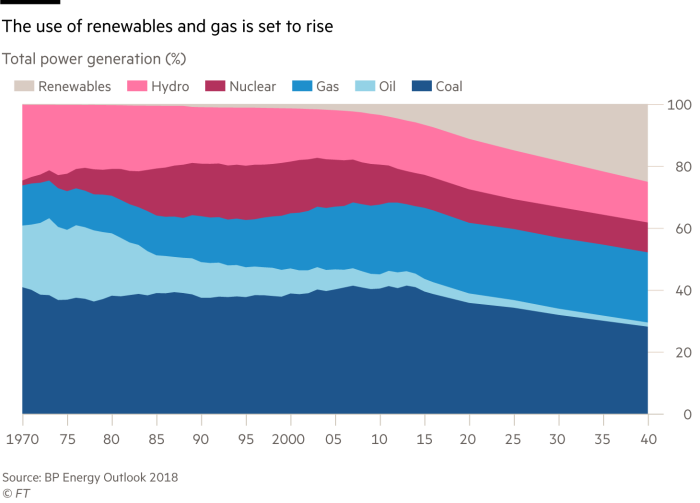

BP, in its long-term energy outlook to 2040, expects almost 70 per cent of the increase in primary energy to be the power sector, with electricity demand growing three times quicker than other energies. Electric vehicles are a small proportion of the global car fleet today but the segment is growing rapidly, with autonomous cars and ride sharing also promoting the trend.

“As oil is so linked to mobility, it is more exposed to changes in consumption,” said Mr Brufau. “We need to figure out how we manage this.”

Repsol’s strategy has seen it invest in a network of rapid charge points for electric cars; set up a joint venture called Wible in Madrid with South Korea’s Kia Motors for a fleet of 500 hybrid vehicles; and make a €750m acquisition for the gas and hydropower assets of Spain’s Viesgo.

Shell also expanded its gas business after the $50bn acquisition of BG Group. It acquired UK power supplier First Utility in February, giving it direct access to retail electricity consumers for the first time, and New Motion, one of Europe’s largest electric vehicle charging companies.

Repsol's modern petrol station in Madrid. The company's strategy to expand into both mobility services and electricity production has seen it invest in a network of rapid charge points for electric cars

Maarten Wetselaar, head of integrated gas and new energies at Shell, said electrification would “underpin” the energy transition.

For Shell, not only will gas displace coal and become more dominant in power generation, it provides a back up for renewables on overcast or windless days. As electricity grows as a proportion of energy consumption, Mr Wetselaar said Shell had “to play in that if we want to be a major”.

Shareholders have also been propelling this investment focus in preparation for an energy transition, concerned that spending on long-term oil projects could be uneconomical in years to come and increasingly over the sector’s contributions to greenhouse gas emissions and global warming.

European groups such as Total, Shell, Equinor, BP and Eni have so far made more low-carbon investments than their US, Chinese and Russian rivals, according to a study by environmental non-profit group CDP. Out of 24 companies, European majors rank as being best prepared for the transition to a low-carbon economy.

However, it is still unclear what success looks like and some investors want oil companies to manage the decline of their businesses — concentrating on generating cash rather than power.

“Finding, developing, producing and transporting hydrocarbon molecules is fundamentally a different business from generating and transmitting electrons,” said Nick Stansbury, head of commodity research at Legal & General Investment Management.

“Does the oil and gas industry need to transform itself into something that more clearly resembles a utility to future-proof its business? [The] answer is probably no.”

But the shift is happening. Total has said it is “allergic” to the word utility even as it builds a retail energy business in France while sidestepping the regulated market.

It bought US solar company SunPower, power vendor Lampiris, battery specialist Saft and took a stake in renewable energy group Eren before acquiring French electricity retailer Direct Energie for €1.4bn this year. This has enabled it to develop a portfolio of gas-fired and renewable energy power plants.

“The potential to combine gas and renewables for power generation is big,” said Philippe Sauquet, Total’s head of gas, renewables and power.

As the power generation world changes “rapidly” towards a more competitive market, he said Total would benefit. “We don’t have legacy assets and privileges in this space. We can be more efficient. We can offer better prices.”

Unlike traditional utilities with a single-facet relationship with customers as a household power supplier, Mr Sauquet believes energy majors want multiple interactions.

“While electrons should be seen as a new commodity, how you provide them to the customer is not,” Mr Sauquet said. “We can make more money from added value services, from smart-meters to monitor consumption and lower bills to electric vehicle charging.”

However, some industry analysts say there is a difference between stepping into adjacent businesses — such as installing electric charging points at existing fuel retail networks — versus areas where they are not leading players, for example, in generation.

Danish wind giant Orsted or Spain’s Iberdrola might be much better suited to develop clean power projects, while crunching data about how and when customers use electricity is more the domain of tech groups such as Google or Microsoft.

The oil majors are also reluctant to spend huge sums until they can make financial gains. Typical returns on investment for wind or solar would be 5-9 per cent versus more than 20 per cent for traditional oil and gas projects, Wood Mackenzie has said.

While Shell has said it plans to spend 80 per cent of its $2bn “new energy” budget on the power sector until 2020, it remains a small proportion of its $25bn capital expenditure total.

Even Mr Brufau at Repsol admitted the money spent on power and clean technologies was “peanuts”.

How to sell electricity profitably is crucial, particularly given the sector’s history when it lost billions of dollars trying its first transition into renewable power. BP made a long retreat after a big move in the 2000s into solar module manufacturing, under its “Beyond Petroleum” mantra. Since then it has trod lightly — investing in another solar company Lightsource; the UK’s largest electric vehicle charging network Chargemaster; and battery start-up StoreDot.

Wood Mackenzie’s Mr Heggarty warned: “Returns will just not be anywhere near what they see in other parts of their business.”

0 comments:

Publicar un comentario