Across the West powerful firms are becoming even more powerful

That could undermine public faith in capitalism, says Patrick Foulis

ONE BRIGHT morning earlier this year your correspondent travelled from New York to the University of Chicago to attend a conference on the threat to prosperity posed by monopolies. The journey began with an alarm beeping on a handset made by Apple (which has a 62% market share in America), then a bumpy taxi ride to the airport paid for using a piece of plastic issued by one of the three firms, American Express, MasterCard and Visa, that control 95% of the credit-card market. In the terminal, breakfast was scoffed from a supersized fast-food chain, while emails were checked using Google, which has 60% of the browser market.

The mobile signal was transmitted on one of the three networks that control 78% of the telecoms market. The flight was with one of the four airlines that control 69% of journeys within America. In Chicago your correspondent checked into the LondonHouse hotel, which looks like a boutique but turns out to be part of Hilton, which controls 12% of all rooms in America, and 25% of the new rooms being built. The booking was made on Expedia, which has 27% of the North American online travel market.

The firms involved in the journey made profits of $151bn and had a median return on capital of 29% last year. An equally weighted basket of their shares—call it the monopoly money portfolio—beat global stockmarkets by 484% over the past decade. Collectively, 17% of the companies’ shares are owned by just three investment mega-managers, BlackRock, Vanguard and State Street.

Described this way, America’s economy has become a capitalist dystopia; a system of extraction by entrenched giants. Europe shows signs of the same sickness. Growing protectionism and increased digitisation may make things worse. The stakes are high.

Competition is an elixir. It spreads wealth today by lowering consumer prices and giving workers more choice of jobs, reducing firms’ monopsony power over them. It boosts productivity tomorrow by pushing firms to create better products for less. If profits in America fell to historically normal levels thanks to more competition, and private-sector workers got the benefits, real wages would rise by 6%. If competition also revived productivity growth, wages could rise a lot further. Without competition, capitalism is torpid and favours the few, not the many.

This special report will examine the claim that big firms are too powerful and that they are stifling competition. It will look at Europe and America, arguing that competition has faded and that a carefully calibrated response is needed. Next, it will consider the tech sector—simultaneously a source of dynamism and monopoly power. Finally it will examine the intellectual decay of the antitrust establishment and explain why inaction is dangerous.

A wake-up call

The view that competition might be in peril extends beyond those travelling from New York to Chicago. It feeds into the public’s sense that the economy is rigged. Pension funds are making huge bets that the likes of Facebook and Hilton can crank out vast profits in perpetuity. Economists worry that powerful firms could distort interest rates; central-bank bosses debated this in August at their gathering at Jackson Hole. In Europe regulators are angry with Silicon Valley. America’s antitrust agencies are waking up from a decades-long slumber, rather like financial regulators after the shock of 2008. Into the vacuum has stepped a radical new antitrust movement that believes the ideal economy is made up of lots of smaller firms with fragmented economic power. It wants to smash concentrations of capital in the name of liberty.

But the story is more complex than big business unfairly crushing all before it. Powerful firms are often efficient and pass the gains to consumers; think of Walmart selling mountains of baked beans for peanuts. They are often innovative, too. Netflix is burning cash to entertain 130m binge watchers. Populists often claim that the West has been ravaged by Chinese competition and is full of lazy incumbents, but can both be true? If monopolies are causing prices to rise, why is inflation low? Go back to that journey to Chicago. Your correspondent chose to switch from Samsung to Apple. The breakfast was cheap. Three of America’s four big airlines have spent time in Chapter 11 protection from creditors since 2005, while its three biggest telecoms firms invest $45bn a year. Expedia’s margins are falling. It is hard to prove that big investors collude. And the LondonHouse is elegant and keenly priced.

“Competition is for losers,” writes Peter Thiel, an American venture capitalist, in his book, “Zero to One”. Monopoly is the goal, he says. But society benefits if successful entrepreneurs are constantly toppled by others. The levelling effect of competition means a constant struggle with vested interests that has played out for hundreds of years.

Adam Smith, a Scottish economist, attacked the guilds that stifled 18th-century Britain. As America boomed in the 19th century industrial empires were created that trustbusters later broke up. Cartels were instrumental in 20th-century totalitarianism. In 1946 American administrators dissolved Japan’s zaibatsu (large industrial and banking conglomerates), and Germany’s Christian Democrats made competition their first priority in their economic manifesto in 1949. Margaret Thatcher used competition to revive Britain’s economy in the 1980s. In the 1990s the European Union used the single market to prise open stuffy industries.

But after 2000 the West became complacent. Globalisation was assumed to guarantee competition. Over-mighty firms were judged to be a risk for corrupt emerging countries like Russia and the Philippines but not the rich world.

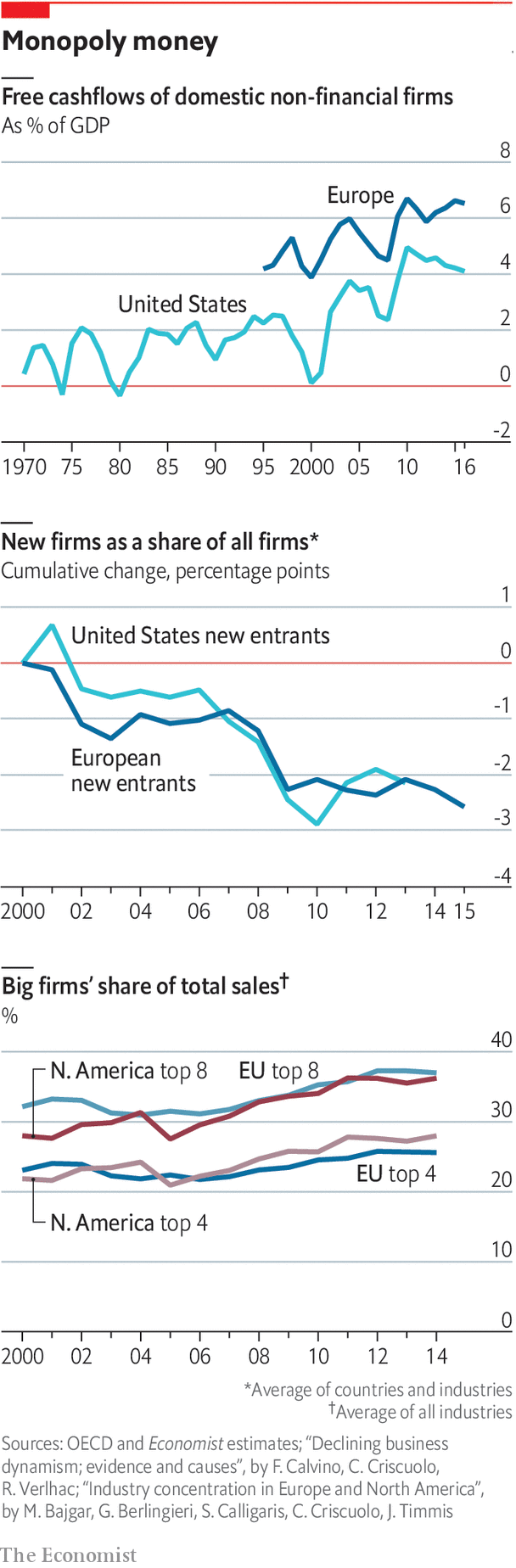

In fact powerful firms were gaining more clout in the West, for bad and good reasons. The bad reasons involve muffling competition. Some $44trn of takeovers have taken place since 1998, many aimed at creating pricing power or efficiency gains whose benefits are not passed to consumers. It has become fashionable for managers to build “moats”, or barriers to entry. That is reflected in the philosophy of Warren Buffett, who has built the world’s most valuable investment vehicle by betting on mature oligopolies in America. Clever firms found new ways to constrict competition. A fifth of all American workers are covered by non-compete clauses.

Patents are “evergreened”. Arbitration clauses and complex contracts are used to hobble competitors. A few fund managers own big chunks of most firms. They do not conspire but they do set the tone at the top, doing little to encourage price wars.

The good reason for more powerful firms is the rise of an innovative elite that is an engine of efficiency. Its members are companies that have mastered digital technologies and enjoy network effects that help them fend off slower competitors, says John Van Reenen of MIT. In the tech sector this is clear. In old-fashioned industries, however, particularly regulated ones, digital wizardry is less likely to explain powerful firms’ clout. Whether they were created by cronyism or genius, if extraordinary profits are maintained for many years with no sign of new entrants, it is a clue that competition may not be working. In America and Europe there is a growing body of evidence that this is the case.

0 comments:

Publicar un comentario