What is behind the global stock market sell-off?

A mix of higher bond yields and growth worries take their toll

Robin Wigglesworth, US Markets Editor

The Wall Street fall carried echoes of February’s 'Volmageddon', when the S&P 500 suffered a 10 per cent correction © FT Montage

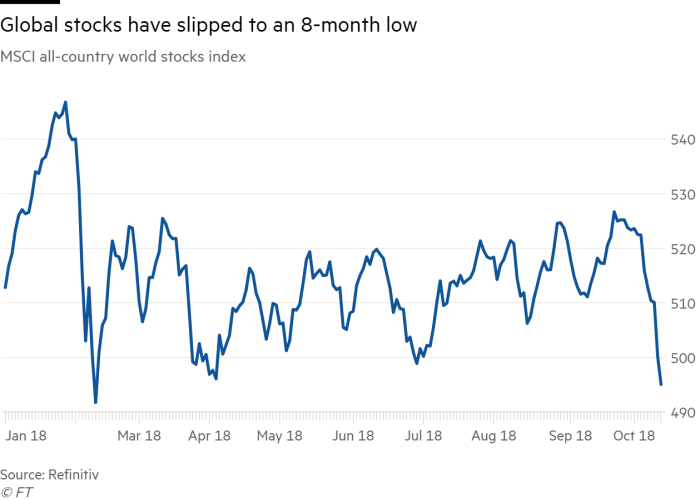

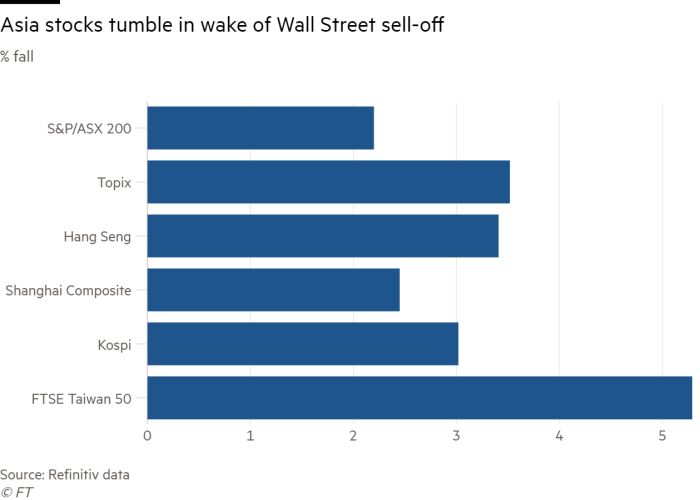

A sell-off that saw tech stocks drive the S&P 500 on Wednesday to its worst one-day drop since February rippled across global markets on Thursday.

The severe drop on Wall Street carried echoes of February’s “Volmageddon”, when the S&P 500 suffered one of its swiftest 10 per cent corrections and raised questions over whether the almost decade-long bull market was at risk. While there was no immediate trigger for the sell-off, here are some of the forces at play in the current market turmoil.

Rising bond yields

Undoubtedly the proximate cause of the stock market reversal. Last week’s bond rout was caused by rising economic optimism, but the severity of the reaction in fixed income — the 10-year Treasury yield raced to a seven-year high of 3.25 per cent — has been sufficient to unnerve equities as well.

Bonds have remained under pressure this week, but not nearly to the same extent. Analysts and investors say yields are not high enough to unduly worry them, and moves in the Treasury market were relatively muted until the equity rout worsened on Wednesday afternoon. The steepness of the drop prompted investors to dive back into the relative safety of US government debt. The yield on the 10-year bond was at 3.17 per cent in London.

“Higher interest rates typically bring on tighter financial conditions which could dampen growth going forward and equity markets are reacting to that,” noted Charlie Ripley, a senior investment strategist for Allianz Investment Management.

So rising yields might have set the stage for the sell-off, but probably cannot shoulder the blame for its ferocity.

Short-volatility bets

The February turmoil also triggered rising yields, but was exacerbated by the collapse of two exchange-traded notes that bet on stock markets remaining tranquil through complex derivatives contracts called Vix futures.

When volatility jumped these funds — and other traders that were “shorting” volatility — were ripped to shreds, and caused volatility to spiral even higher as they sought to cover their positions. That bled back into the stock market through S&P futures and caused further declines.

A similar dynamic might have come into play this week. Data from the Commodity Futures Trading Commission indicate that investors are once again shorting Vix futures to the greatest degree since January, and the CBOE’s volatility-of-volatility index has rocketed to its highest since February.

“The US market sell-off last night spooked sentiment and rekindled memories of similar trading sessions at the beginning of the year,” said Medha Samant, investment director for Asian equities at Fidelity International.

However, one of the Vix ETNs that fuelled February’s “Volmageddon” is dead and the other is a shadow of its former self, and derivatives traders say that the market is on the whole not quite the coiled spring it was at the start of the year.

Stock market rotation

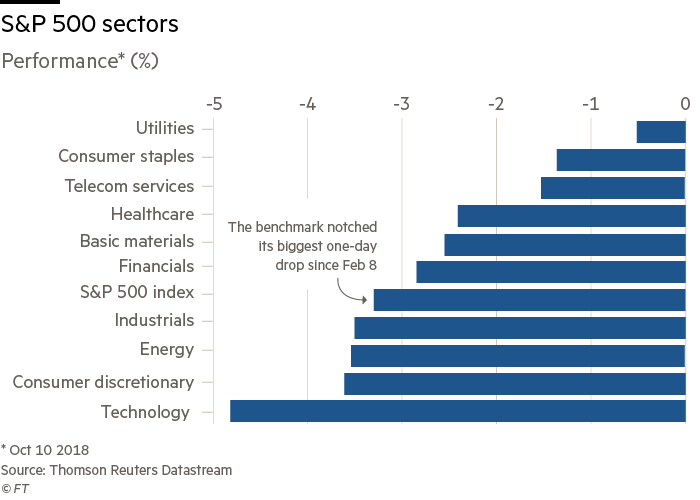

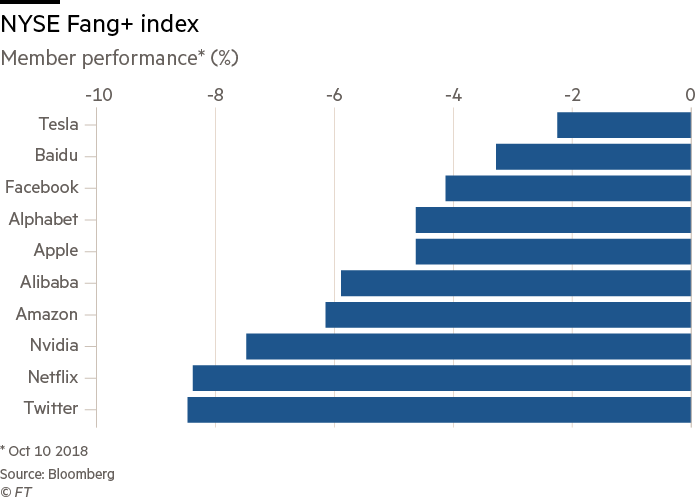

One of the most notable developments in the US of late has been the abrupt reversal of winners and losers. Unloved stocks that have lagged behind the 2018 rally have performed much better, while the biggest casualties have been previously high-flying companies and sectors.

Fast-growing technology stocks have been the go-to investment of fund managers in recent years, given that economic growth has been far from stellar. But with the US economy now strengthening, some investors appear to be rotating into cheaper “value” stocks that will benefit from the uplift.

Meanwhile, bond yields are used to discount the future value of cash flows. The lower they are, the better they are for assets with long duration — such as 30-year Treasuries, or equities, which are (in theory) perpetual securities.

Given the lack of dividends and higher valuations, many tech stocks are arguably the longest-duration asset in the world, “it’s perfectly reasonable that they would eventually succumb to rising rates,” strategists at Morgan Stanley note.

Global growth outlook

The extent of the praise that Fed chair Jay Powell heaped on the US economy last week surprised some, but the American economy’s outperformance has been one of the key trends for markets this year. However, it has come as much of the rest of the world has slowed.

Mario Draghi, president of the European Central Bank, has pointed to rising protectionism as the “major source of uncertainty” to the eurozone economy, where recent business surveys and official manufacturing data showed falling confidence and slowing export sales. The International Monetary Fund this week cut its growth forecasts for most countries for this year and in 2019.

“For much of 2018, the US economy has been oblivious to a turn in the global economic cycle, and the US equity market has been unaffected as emerging market equities and currencies have come under pressure,” noted Kit Juckes, a strategist at Société Générale. “This week has seen the S&P, and the Nasdaq, sit up and pay attention to what’s going on.”

While tech stocks led the sell-off, energy was the fourth worst performing sector as the oil price tumbled. Brent fell 2.2 per cent on Wednesday and was 1.2 per cent weaker on Thursday morning in London.

Systematic strategies

There are many computer-powered investment strategies that systematically scale their market exposure according to volatility. So when markets turn choppier they sell, and when turbulence simmers down they buy.

How quickly they respond to volatility varies greatly by strategy, and systematic fund managers insist that they barely respond to shorter bursts of volatility. But some analysts and investors argue that they can nonetheless exacerbate both routs and rallies.

The three main types are risk parity funds, commodity trading advisers — a kind of trend-following hedge fund — and “variable annuity” insurance accounts with a fixed volatility target. Numbers vary but analysts put their total assets under management at about $1tn. These funds tend to rebalance in the last hour of the trading day, which might explain why the sell-off seemed to accelerate into the closing bell.

But exchange traded funds and many other quant strategies also adjust positions at the end of the day, which pools activity into a narrow window and encourages other investors to do so as well, so the end-of-day tumble is not necessarily evidence of systematic, volatility-targeting funds exacerbating the turmoil.

0 comments:

Publicar un comentario