The Brewing Fight Over the Yuan

The Chinese government doesn’t want its currency to fall too much, but hedge funds are betting they can’t stop it

By Jacky Wong

Hedge funds betting the yuan will fall below 7 to the dollar. Photo: Reuters

Investors and the Chinese government are gearing up for a fight over the yuan, with hedge funds betting the Chinese currency will fall below 7 to the dollar for the first time in more than a decade and Beijing essentially saying, “no way.”

China’s yuan stands at 6.9270 against the dollar, 1% above the psychologically important level of 7. The yuan last traded at that level in 2007, when the Chinese economy was far smaller and its currency was rising rather than falling. The one-year foreign-exchange forward contract on offshore yuan briefly spiked above 7 last week.

There is nothing magical about the number 7, but it seemed to be the do-not-cross line when China’s central bank defended its currency in 2016.

This time around, Beijing may find it harder to hold that line because interest rates in the U.S. are rising while China needs to ease to counter the economic slowdown at home. The difference between China’s 10-year government bonds and the U.S. Treasury note of the same tenor has shrunk to 0.5% from 1.7% late last year. The divergence in the two country’s monetary policies mean the gap will continue to narrow or switch so that U.S. bonds yield more than Chinese.

That draws money into dollars and out of yuan, pushing up the dollar and pushing down the yuan.

The 7 level is especially important now because China is under pressure from the U.S. not to depreciate its currency to offset the impact of trade tariffs. China’s central bank Gov. Yi Gang stressed over the weekend that the country wouldn’t engage in competitive devaluation.

Another concern for China is capital flight. The yuan depreciation in 2015 sent billions flowing out of the country, and China’s central bank eventually needed to spend around $1 trillion of its foreign-exchange reserves to defend the yuan.

Hedge funds share none of those worries and see the yuan as vulnerable. Beijing has made clear that this view is unacceptable. The interbank lending rates on the offshore yuan in Hong Kong spiked last week, an indication that Chinese authorities have tried to squeeze out the shorts by making it more expensive to borrow the yuan.

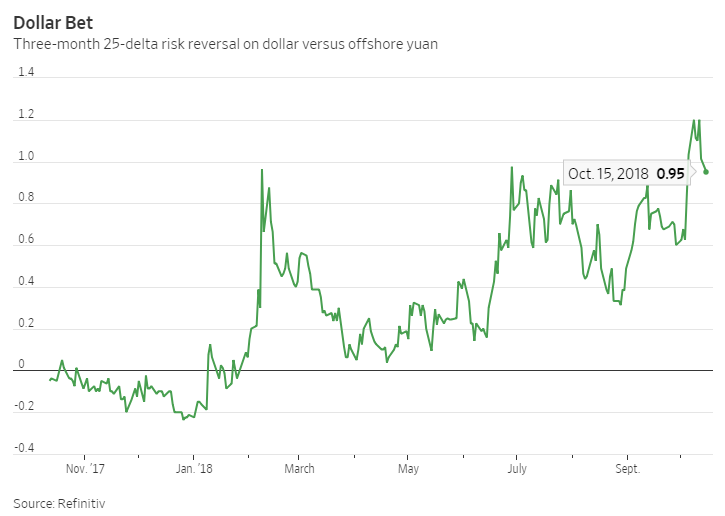

But speculators don’t seem to have been deterred. Three-month 25-delta risk reversal on the dollar versus the offshore yuan—a gauge of bearish versus bullish bets—has stayed higher. A higher number means investors are willing to pay more for bearish bets on the yuan versus the dollar.

China’s capital controls, tightened after 2016, seem to be working well this year, as capital outflows are minimal even though the yuan has dropped 10% against the dollar since February. Foreign inflows into China’s bond and stock market, in part because they have recently been included in popular indexes, has also helped. But as China’s housing market—a major investment for Chinese—starts to feel a little shaky recently, the real test is ahead.

0 comments:

Publicar un comentario