No hiding place for investors in markets wobble

Almost every major asset class has fallen into negative territory for the year

Robin Wigglesworth, Steve Johnson and Katie Martin

Nerve-racking conditions in markets have left traders treading a thin line © Getty

Global markets have suffered plenty of post-crisis wobbles, but the latest one is unique: for the first time in a very long while, almost every major asset class has fallen into negative territory for the year.

The US stock market and US junk bonds were the last two corners to still hold on to narrow gains for 2018. But this month even high-flying technology stocks have been pummelled, and this week the last of the S&P 500’s advance evaporated and left investors facing a sea of red.

The markets’ bounce on Thursday proved shortlived, as investors who had started scouring the detritus for bargains were wrongfooted by the third-quarter results of Amazon and Alphabet, which reignited the sell-off. The S&P 500 only fell 3 per cent or more twice in 2012-17, but has now done so four times in 2018 — and twice just this month.

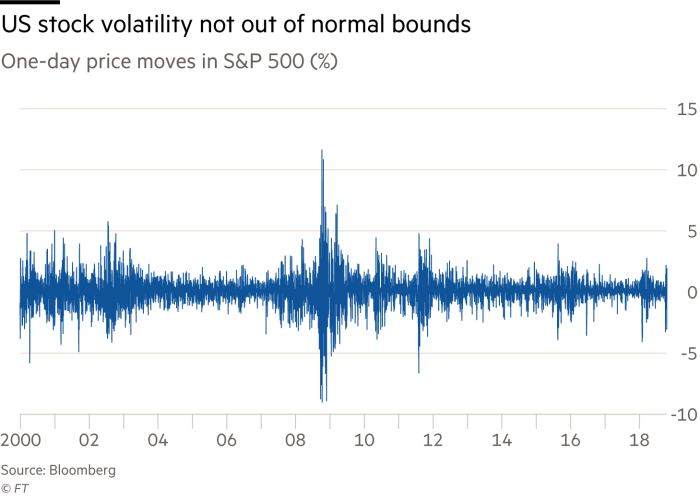

However, analysts and investors insist they are not panicking yet. While October has been a bad month, the sense of its severity has been amplified by the calm stretch that preceded it. The US stock market has historically averaged more than four falls of 5 per cent (or more) a year, and suffers a 10 per cent correction roughly once a year.

US equity funds took in $1.8bn for the week ending October 24, according to data from EPFR, indicating that some investors are looking to take advantage of the rout. “It’s never enjoyable when markets fall this far, but I don’t think any investors are jumping ship,” said Andrew Scott, head of US flow strategy at Société Générale.

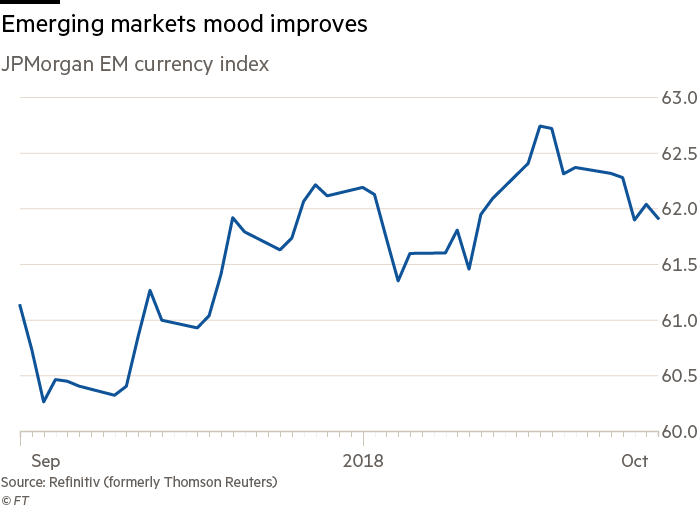

Even the mood in emerging markets — hit harder than anywhere else since the summer — is also starting to improve. The JPMorgan EM currency index has bounced 3 per cent from its September nadir, enabling both hard and local currency EM debt to recover from its lows, even if equity markets have continued to sag lower.

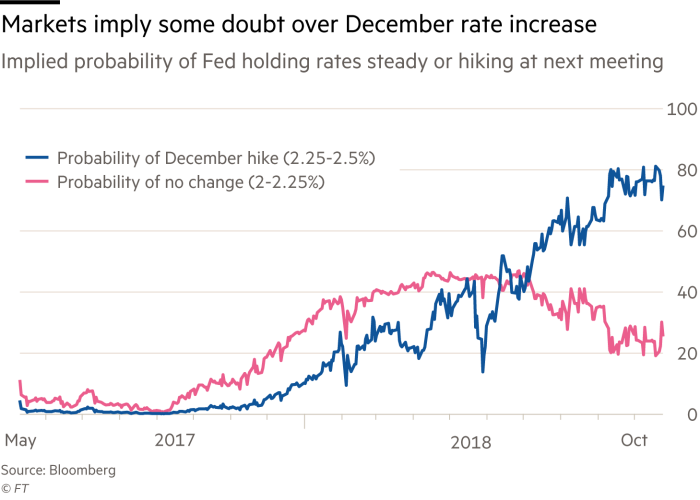

Nonetheless, the abruptness of the sell-off — global equities are on track for their worst month since mid-2012 — and its breadth has sparked some speculation the US Federal Reserve could hold fire at its next meeting in December. A fourth interest rate increase for the year has long been considered a foregone conclusion, but some doubt is creeping in.

Fed Funds futures, derivatives that allow traders to bet on US interest rates, now imply a 33 per cent chance the central bank will blink and hold steady in December, up from just 19 per cent last Friday.

The yield of two-year Treasuries, the most rate-sensitive corner of the US government bond market, has slipped to a one-month low of just under 2.8 per cent. Financial conditions, a measure of how supportive or restrictive markets are for growth, have also tightened abruptly this month. Goldman Sachs’ index of how stressed conditions are has jumped to its highest since March 2017.

However, most investors remain very sceptical that the Fed will blink, given the increasingly hawkish tone from policymakers in recent months.

“They remain data-dependent, and they seem convinced that the US economy is fine,” said Jim Sarni, managing principal at Payden & Rygel. “It will take more than this to push them off course.”

The European Central Bank also seems unperturbed. In his latest press conference on Thursday, ECB president Mario Draghi said the market volatility was a “persistent” cause for concern. But he stopped far short of suggesting that they would derail the ECB’s plans to reel in its stimulus, stressing that interest rates would remain extremely low even after the bond-buying programmes start to unwind.

The biggest danger confronting investors is therefore that the “rolling bear market” — as Morgan Stanley has dubbed the expanding sequence of asset classes suffering losses this year — continues to rumble on, and plays havoc with many popular portfolio construction methods.

What is so nerve-racking about this rolling bear market is that it leaves even big, diversified investors few places to hide.

Typically, bond investments offer some relief when equities are tumbling. And fixed income tends to sag lower when stock markets are soaring. But in 2018, almost nothing has worked out, which undermines one of the foundational principles of how most investment portfolios are designed – the importance of diversification.

The lack of insulation from fixed income has exacerbated the sell-off, as investors who want to prune their market exposure have no choice but to simply sell, notes Salman Ahmed, chief investment strategist at Lombard Odier Asset Management.

US high-yield debt has stayed surprisingly resilient, but is only barely in positive territory for the year, and the global bond market as a whole has lost more than 3 per cent in 2018, setting in on course for its third-worst year since at least 1998. At the same time, the FTSE All-World has tumbled nearly 10 per cent just this month.

If historical correlations continue to go haywire then it could cause an “utter bloodbath” for investors that don’t seek to protect their portfolios in more imaginative ways, Société Générale’s Mr Scott predicts.

“The whole portfolio diversification argument doesn’t work when everything is selling off,” Mr Scott said. “That’s why this will be such a fascinating time for markets.”

0 comments:

Publicar un comentario