How to avoid the next financial crisis

Latest IMF data highlights the lasting damage done by the 2008 collapse

Martin Wolf

The financial crisis of 2008-09 and the resulting recession were a historical watershed. The pre-crisis world was one of globalisation, belief in markets and confident democracies. Today’s is a mirror image.

The economic impacts are certainly not the end of the story. But they are the beginning. The latest World Economic Outlook of the IMF provides a valuable empirical analysis of the effects. It brings out two big points: the impacts have been long lasting and have spread far beyond the countries that suffered banking crises.

The obvious way to measure the economic impact of crises is by comparing post-crisis performance with what would have happened if pre-crisis trends had continued. Yet pre-crisis trends were, to some extent, unsustainable. So, the IMF’s analysis adjusts pre-crisis trend growth for credit booms.

The IMF notes that “91 economies, representing two-thirds” of global gross domestic product in purchasing-power-parity terms, experienced a decline in output in 2009. This was the biggest negative shock in the postwar era. Moreover, the bigger the losses in the short run, the bigger they were in the long run, too. Countries with large immediate falls in output also showed larger increases in income inequality, relative to pre-crisis averages.

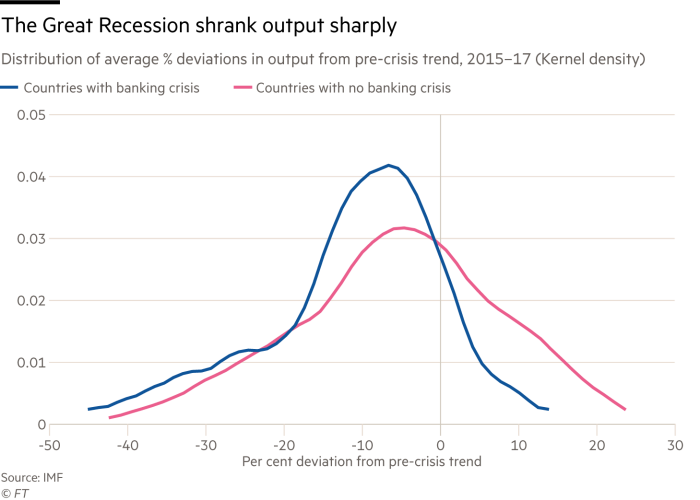

Which sorts of countries lost most and how much did they lose? To answer this question, the WEO divides its 180-country sample into ones that suffered banking crises and those that did not.

The former group contained 24 countries, 18 of which are high-income economies. It found that 85 per cent of them still show shortfalls of output relative to trend. For countries that suffered banking crises, the modal (most frequent) average shortfall of output between 2015 and 2017, relative to pre-crisis trends, was close to 10 per cent. But a number suffered losses of between 20 and 40 per cent. (See charts.)

Yet output also remains below pre-crisis trends in 60 per cent of countries that did not suffer banking crises. Modal losses here have been much the same as in crisis-hit countries, though the distribution is less skewed to the downside.

The pervasiveness of losses may not be that surprising: this crisis emanated from the core of the global economy and caused big declines in global demand. The results were deep recessions, which cast very long shadows into the future.

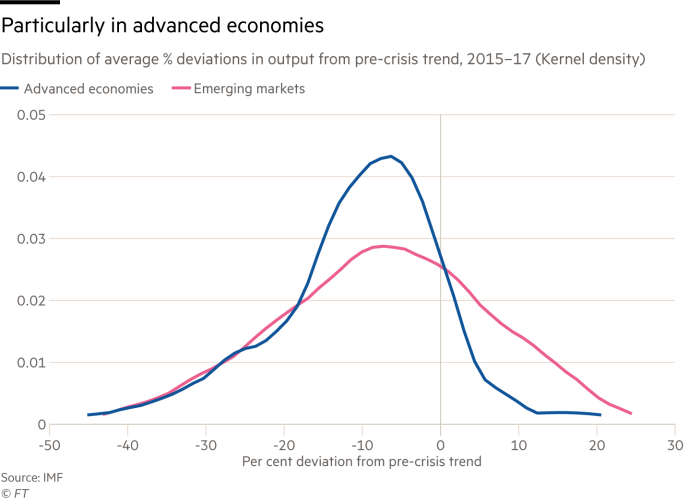

Again, while advanced economies were particularly hard hit, emerging economies did not do much better. This was a western financial crisis, but it was a global economic crisis. China’s stimulus programme of about 10 per cent of GDP greatly cushioned the impact.

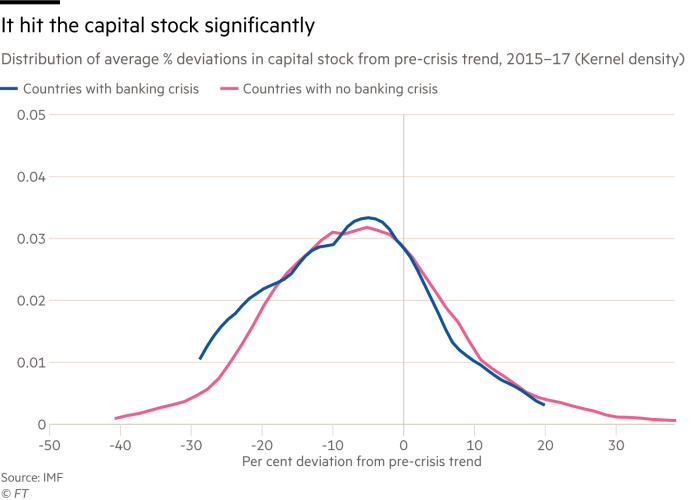

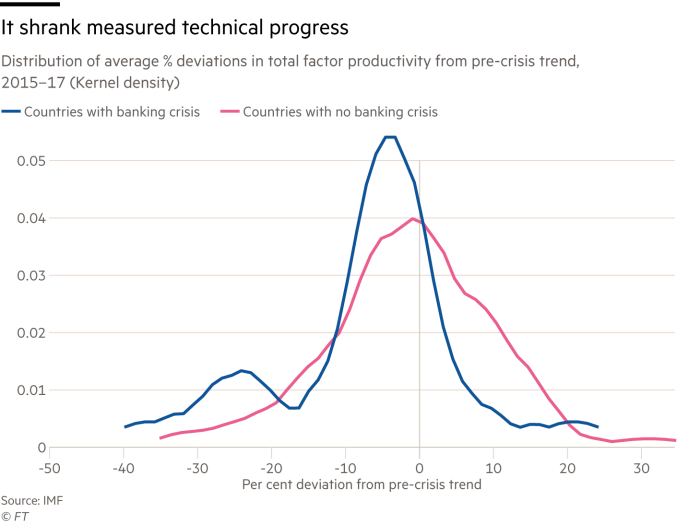

The proximate explanations for the huge shortfalls in output were collapses in investment: by 2017, on average, investment was a quarter below pre-crisis trends. This weak investment must also help explain low rates of innovation, which is particularly visible in directly-hit countries. New technology is often embodied in new equipment: take robots, for example.

On average, countries that experienced banking crises suffered a four percentage point bigger loss in output by 2011-13 than ones that did not. Those with large pre-crisis macroeconomic imbalances, notably unsustainable current account deficits, also suffered relatively large losses. So did those with relatively inflexible labour markets. Again, those whose exports were more exposed to crisis-hit markets were hit harder. Countries that were more exposed to the global financial system also suffered larger losses. Lack of fiscal policy space proved costly, as well, as did a lack of exchange rate flexibility. The last is certainly an explanation, albeit not the only one, for the terribly poor performance of the eurozone.

The monetary actions taken by the high-income countries in the aftermath of the crisis have been controversial in many emerging markets. Many in high-income countries have also argued that the dramatic monetary easing was a mistake. Yet the evidence that output shortfalls are cumulative destroys the argument against strong and sustained policy support. However, stronger fiscal policy responses would have reduced the need for so long a period of unconventional monetary policies.

Equally controversial were the capital injections and guarantees provided to the financial sector in the crisis. Maybe, ways could have been found to rescue banks without rescuing bankers. But the greater the support for the damaged financial sector, argues the WEO, the stronger the rebound. This evidence gives no support to “liquidationism” — the view that banking collapses and depressions are benign purgatives.

Here are three tasks and a lesson.

The first task is that of monetary policy normalisation in a world that has so much debt. Higher US policy rates have already revealed the vulnerability of a number of emerging economies. More turbulence seems highly likely.

A second task is how to respond to another big recession, when the policy space is so diminished.

The final task is coping with the political aftermath of the crisis. The decline in western credibility and relative power and the rise of demagogic forces are real, powerful and dangerous.

The lesson is that big financial crises are — no surprise — very damaging. Once they have happened, it is too late. The analysis of regulation in the October Global Financial Stability Report suggests that we must ignore bankers’ bleating against regulation: above all we must keep capital requirements up.

Recoveries could have been stronger with sustained fiscal and financial action, notably in the eurozone. But the costs of crisis would still have been high. “Never again” must be the watchword.

0 comments:

Publicar un comentario