Feeling the heat

America is pushing the labour market to its limits

Low unemployment and inflation complicate economic policymaking

BY MANY measures, America’s economy is powering ahead. GDP is on track to grow at around 3% this year, and the unemployment rate is an impressively low 3.9%. For President Donald Trump, it is an unmissable opportunity to gloat. On September 10th he described the economy as “soooo good” and “perhaps the best in our country’s history”. But for others the very same figures present an economic puzzle.

The Federal Reserve has been raising its benchmark interest rate since December 2015, and will probably do so again this month, from a range of 1.75-2% to 2-2.25%. This is the central banker’s version of twiddling the bath taps, but on a national scale. It requires a delicate touch. Too much cold water, in the form of higher rates, will choke off demand and hence jobs. Too much hot, and rising inflation will eat away at people’s spending power. The aim is to find the perfect temperature, where employment is as high as it can be while inflation stays subdued.

But as Jerome Powell, the chairman of the Federal Reserve, reminded his listeners in a speech in Jackson Hole on August 24th, no one knows what that perfect temperature is. Policymakers must make their best guess of what “full employment” looks like, or when the “output gap” (the difference between where the economy is and its long-run potential) is zero. Inflation and employment are affected by temporary shocks and structural shifts, as well as by economic policy. Errors take time to show up. It is as if the rate-setters must adjust the flow of hot and cold water not only without knowing what temperature is most comfortable, but also without knowing how hot the bath is to begin with—or when they will be getting in.

Over time, those best guesses have changed. Six years ago the central estimate among members of the Federal Open Markets Committee (FOMC), the body that sets interest rates, was that in the long run, unemployment would settle at 5.6%. Now their estimate is 4.5%. Weak productivity growth has led them to cut their estimate of America’s long-run growth rate, too, from 2.5% in 2012 to 1.9%.

Whether they were right to do so is the subject of much debate. Some economists think policymakers have been too quick to conclude that dismal growth after the financial crisis indicates a new normal. A recent paper suggests that the standard ways of estimating an economy’s potential are overly influenced by blips in its performance. Others think that running the economy hot could spur productivity-enhancing innovation, as wage growth forces firms to economise on labour. Sceptics of that argument point out that the productivity slowdown started before the crisis, suggesting that it is unrelated to labour-market conditions.

As the Federal Reserve’s mandate refers to employment, not output, members of the FOMC must consider a narrower question: what does full employment look like? Here, the puzzle of the past few years has been why, even as the unemployment rate has plunged, inflation has been so stubbornly low. Hawks think that hidden inflationary pressures are building; doves, that behind that headline unemployment rate there is still excess labour capacity.

Until very recently, the doves have had the best of the argument. The most obvious interpretation of such a low unemployment rate is that the labour market could not improve much without pressing prices upwards. However, it has been soaking up not only job-seekers, but also people who reported that they had not been looking for work, or who had been working fewer hours than they wanted.

But arguing that the labour market still has hidden slack is becoming harder. Data released on September 11th revealed that Americans are quitting their jobs at the highest rate since 2001.

For each job opening, there are just 0.82 hires and 0.9 unemployed people hunting for a slot.

All of the main measures of labour underutilisation reported by the Bureau of Labour Statistics are at or below their pre-crisis trough, and near to where they were at the peak of the dotcom boom.

It is possible that still more people will be drawn into the labour market. The prime-age employment rate in August was 79.3%, a little below the pre-crisis peak of 80.3% and below the high of the past 70 years, of 81.9%. But those benchmarks may no longer be appropriate: male labour-force participation has been drifting downwards for decades.

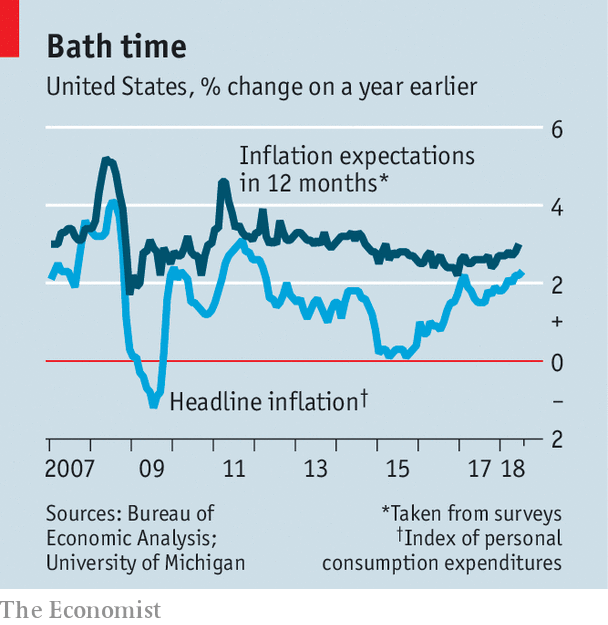

Recent data have also favoured the hawks. Headline inflation has been above target for five months. Inflation excluding food and energy prices, generally regarded as more useful than the headline figure when it comes to predictions, is rising. It hit 2% for the first time since 2012 in July. According to a survey by the University of Michigan, inflation expectations appear to be rising gently, too. Even average hourly earnings seem to be accelerating, up by 2.9% in August compared with 12 months ago (though admittedly, that is not much more than inflation, and still below the pre-crisis norm).

Olivier Blanchard of the Peterson Institute for International Economics points out that over recent decades, inflation has become less influenced by the jobless rate, and is therefore less useful as a signal of whether the economy has hit full employment. Nevertheless, he sees enough evidence from the labour market to conclude that the economy is very close to full employment, and predicts an end to all the head-scratching.

One way to interpret the recent trends is as a vindication of the FOMC’s approach to interest rates. As the economy seems to be heating up, they are twisting the bathtap to what they think is a neutral position. So far, they have managed not to overdo it. Some have called for faster action, fearing a repeat of the 1970s, during which inflation, and inflation expectations, rose in a mutually reinforcing spiral. But as Mr Powell pointed out in his speech, although inflation has recently moved up to near 2%, there are no clear signs of an acceleration above that.

Whether congratulations are warranted will depend on whether recent trends are sustained. If they are, the debate between hawks and doves will not end, but change. Central bankers have managed to train the general public to expect low inflation, meaning that, for now at least, any fears of spiralling prices seem unjustified. But that may imply that the risks of running the economy hot have fallen. In other words, the stronger central bankers’ promises to control inflation, the more tempting it may be to break them. It’s enough to make you want a long, hot bath.

0 comments:

Publicar un comentario