A Sober Look At Housing In The Middle Of All The Chaos

by: Eric Basmajian

- While prices are still rising, the housing market is starting to contract.

- Housing stocks are the worst-performing sector in the US equity market.

- The residential housing market is typically the first sector to decline in an economic cycle.

Is this a blip or something bigger?

- Housing stocks are the worst-performing sector in the US equity market.

- The residential housing market is typically the first sector to decline in an economic cycle.

Is this a blip or something bigger?

While the stock market continues to hit new all-time highs, the volatility in interest rate explodes, and political theatrics consume most media outlets, the housing market has had a very stealth slowdown that should start to be a cause for concern. The housing market has gone from a "yellow light" to a "red light" based on the recent data, and the housing-related equities support that view with the iShares U.S. Home Construction ETF (ITB) falling 26% since January 2018.

If the economic data doesn't suffice, perhaps housing stocks in a full-fledged bear market will garner some attention.

In this piece, I want to take a comprehensive, unbiased and data-driven approach to analyze the most popular high-frequency housing data and conclude by showing the impact to housing-related stocks.

I will start with the most leading of indicators in the housing market such as new construction measures and move on to the more significant existing home sales market and conclude with the price action in the housing market.

After the data-dump, I will turn over to the housing-related stocks for a look at their performance, and why the recent move makes sense in the context of the trending economic data on housing.

The first thing to slow in a housing cycle is new construction so that is where I'll begin.

New Construction Growth Is Contracting

The best place to find information on new construction is in the Census Bureau's report on New Residential Construction. The most reliable indicator is "Building Permits" which I prefer over "Housing Starts" due to the variability in weather conditions having an impact on breaking ground in a new construction. Building Permits simply measure the approval given to start a new project and are not impacted by the weather. If fewer building permits are issued or "asked" for, this is a good indication that the desire for new construction is slowing.

This is a leading indicator of economic activity. Existing projects will continue, but in the months ahead if a new project won't be started, that means fewer jobs, wages and economic activity.

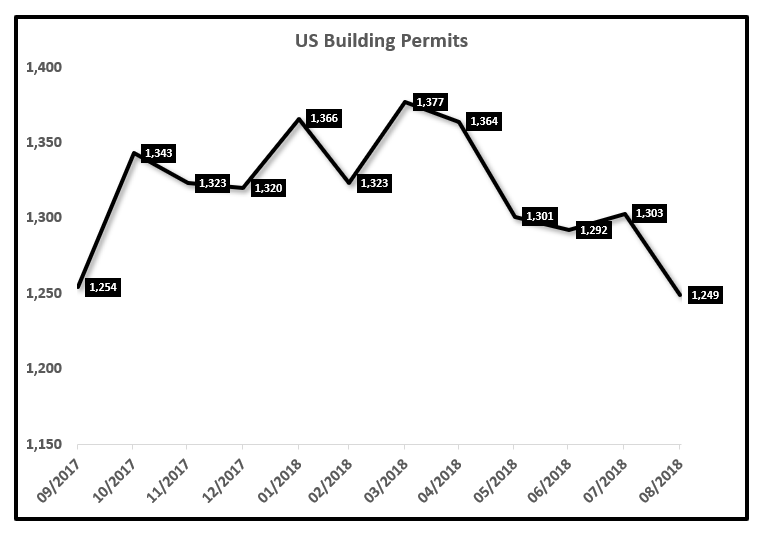

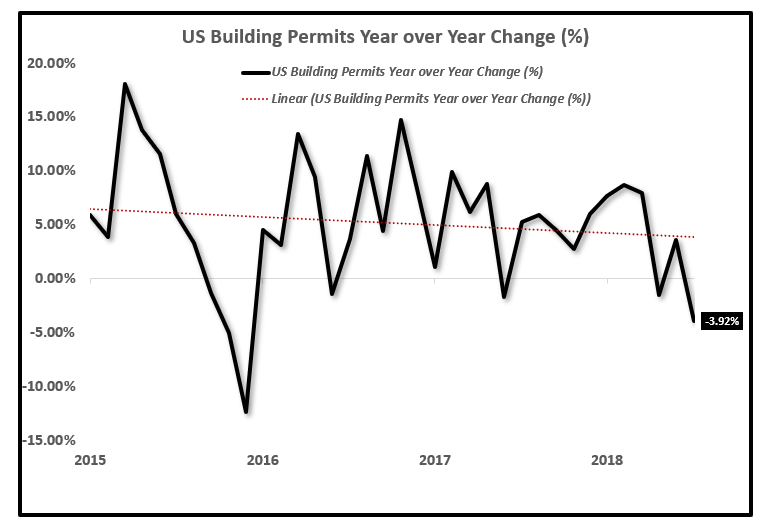

The number of Building Permits is down 3.92% compared to one year ago and down 9.3% compared to the peak in March of 2018.

US Building Permits:

Source: YCharts, EPB Macro Research

The growth rate in the number of Building Permits has been trending lower for the past three years and now sits in contractionary territory.

US Building Permits Year over Year Change (%):

Source: YCharts, EPB Macro Research

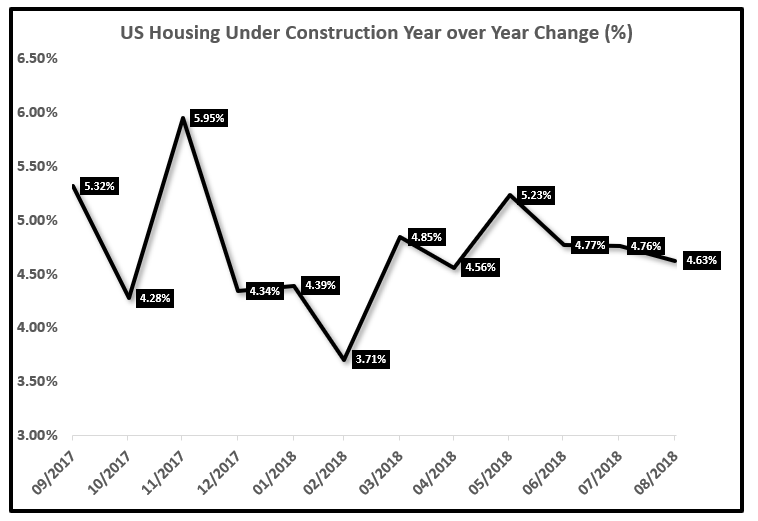

While Building Permits lead economic activity in the new construction segment of housing, the "Housing Under Construction" indicator is more of a coincident index of what level of activity is occurring at this moment.

The growth rate has been relatively stable in the number of houses under construction at roughly 4.5% over the past 12 months.

US Houses Under Construction Year over Year Change (%):

Source: YCharts, EPB Macro Research

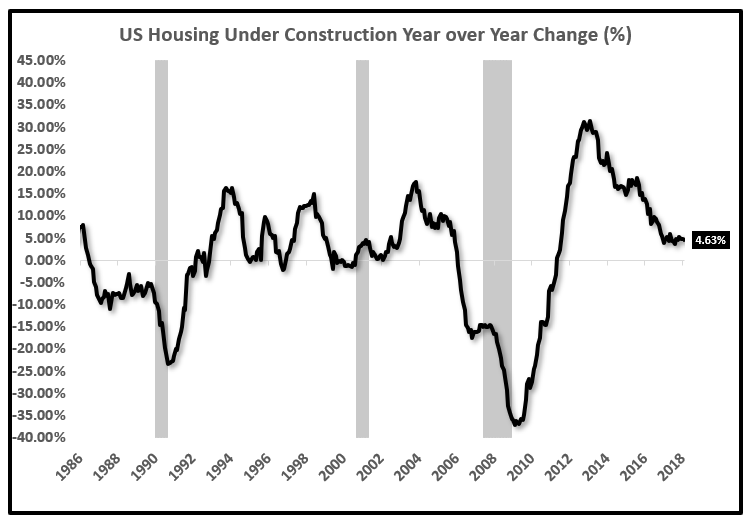

Pulling the chart back on the growth rate of Houses Under Construction shows a trend of deceleration.

US Houses Under Construction Year over Year Change (%):

Source: YCharts, EPB Macro Research

Given that the number of Building Permits is falling, we can expect the number of Houses Under Construction to continue to decelerate.

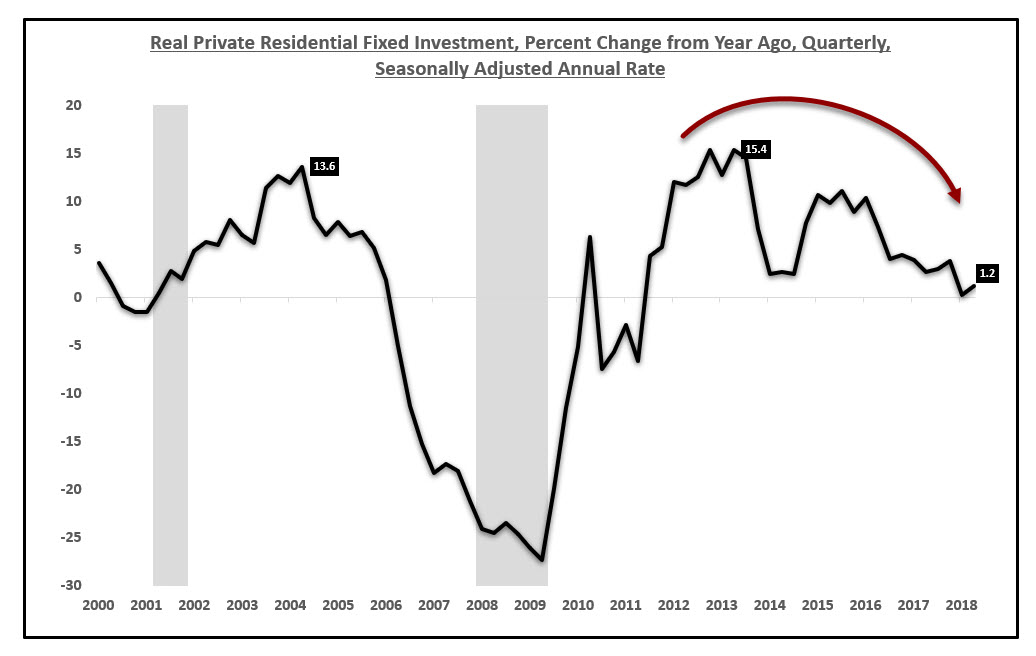

To finalize this stage of the analysis and prove that this level of housing activity is negatively impacting GDP, we can look at the Private Residential Fixed Investment component to GDP.

Private Residential Fixed Investment consists of purchases of private residential structures and residential equipment that is owned by landlords and rented to tenants.

Residential structures include "new construction of permanent-site single-family and multi-family units, improvements (additions, alterations, and major structural replacements) to housing units, expenditures on manufactured homes, brokers commissions on the sale of residential property, and net purchases of used structures from government agencies.

Residential structures also include some types of equipment that are built into residential structures, such as heating and air-conditioning equipment." - BEA

Residential Fixed Investment has been negative the past two quarters when looking at GDP on a quarter over quarter basis and trending towards 0% on a year over year basis.

Residential Fixed Investment Year over Year Growth (%):

Source: BEA, EPB Macro Research

The Atlanta Fed is estimating a third consecutive negative quarter for Fixed Residential Investment.

A "red light" in the housing market does not mean a crash but it does mean that the early signs of residential construction have turned negative.

The market for Existing Home Sales has held up slightly better but softened rather dramatically in recent months.

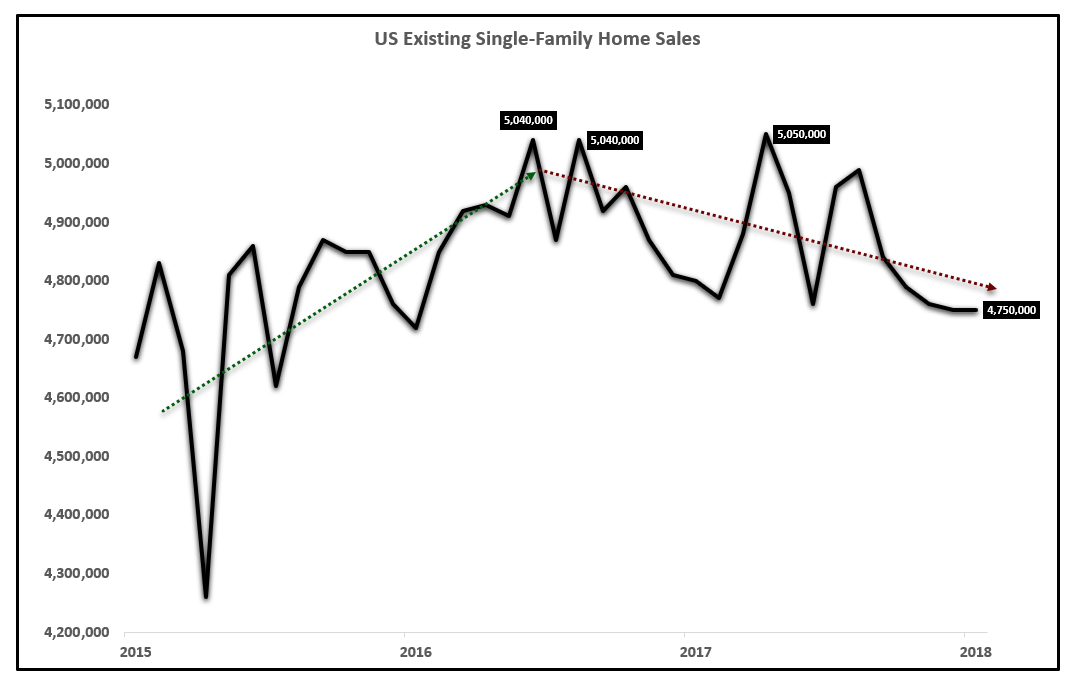

Existing Home Sales Volume Is Contracting

The volume for Existing Home Sales transactions comprises roughly 90% of the total transactions in the US residential housing market. The activity in the Existing Home Sales market, while larger, is less of a leading indicator of economic activity but still important nonetheless. The Existing-Home Sales data measures sales and prices of existing single-family homes for the nation overall.

The volume of Existing Home Sales transactions has also started to contract, dropping roughly 6% from the peak in November of 2017.

Existing Home Sales (Volume Of Transactions):

Source: YCharts, EPB Macro Research

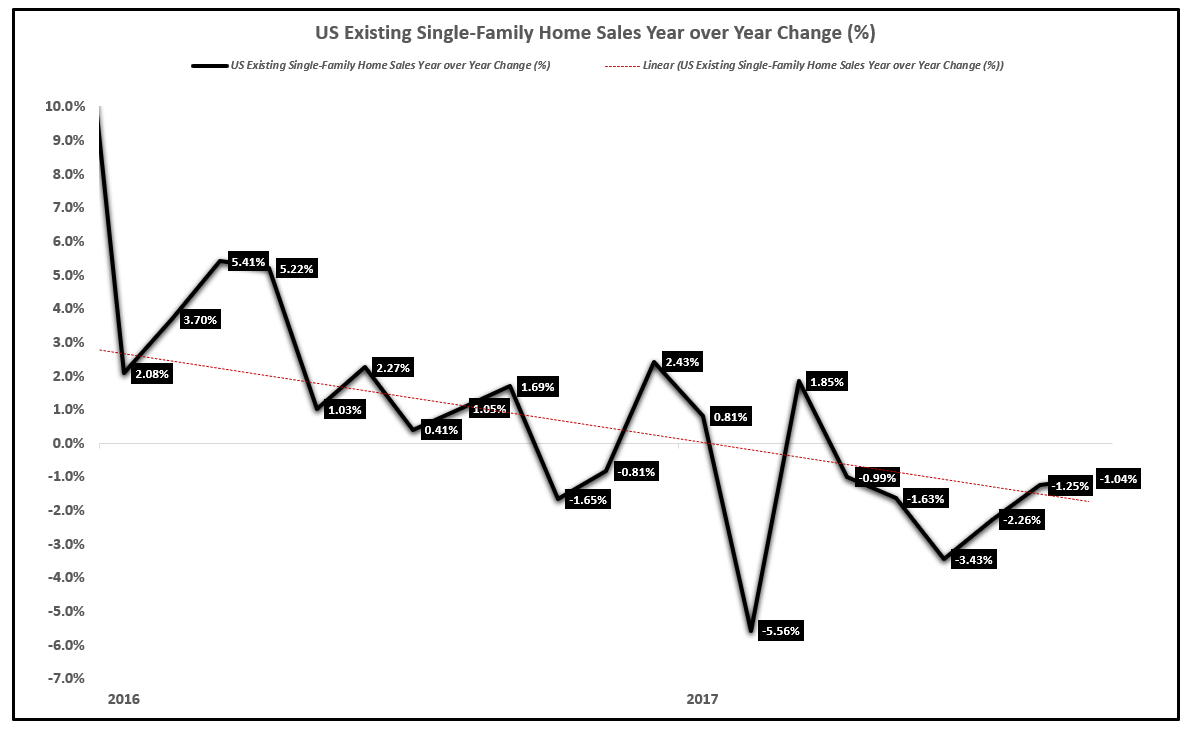

In year over year growth rate terms, the volume of Existing Home Sales transactions has been negative for six consecutive months and for nine of the last 12 months.

Existing Home Sales Year over Year Growth (Volume Of Transactions):

Source: YCharts, EPB Macro Research

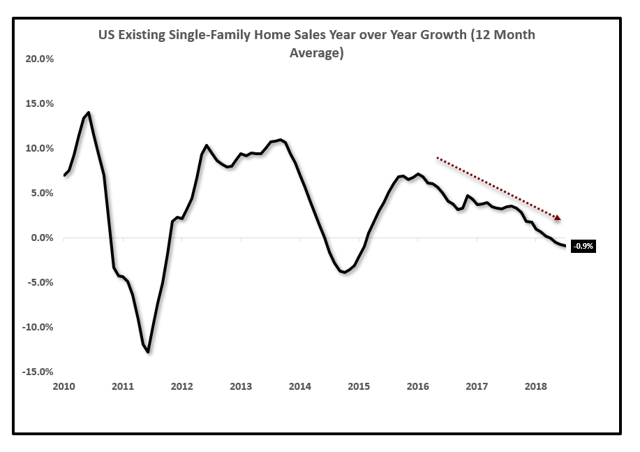

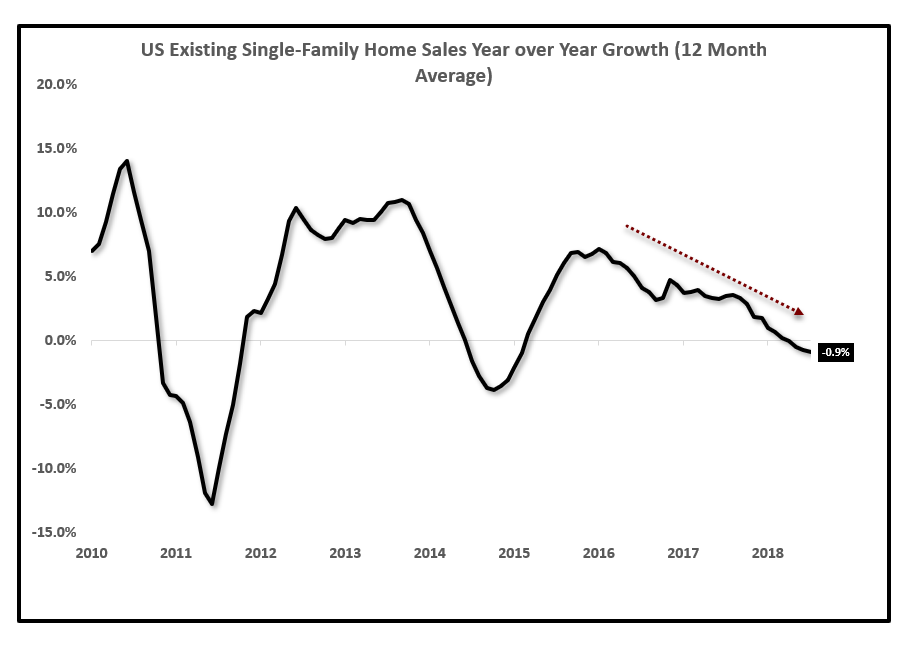

The 12 month moving average of Existing Home Sales is down 0.9% year over year.

Existing Home Sales Year over Year Growth 12 Month Average (Volume Of Transactions):

Source: YCharts, EPB Macro Research

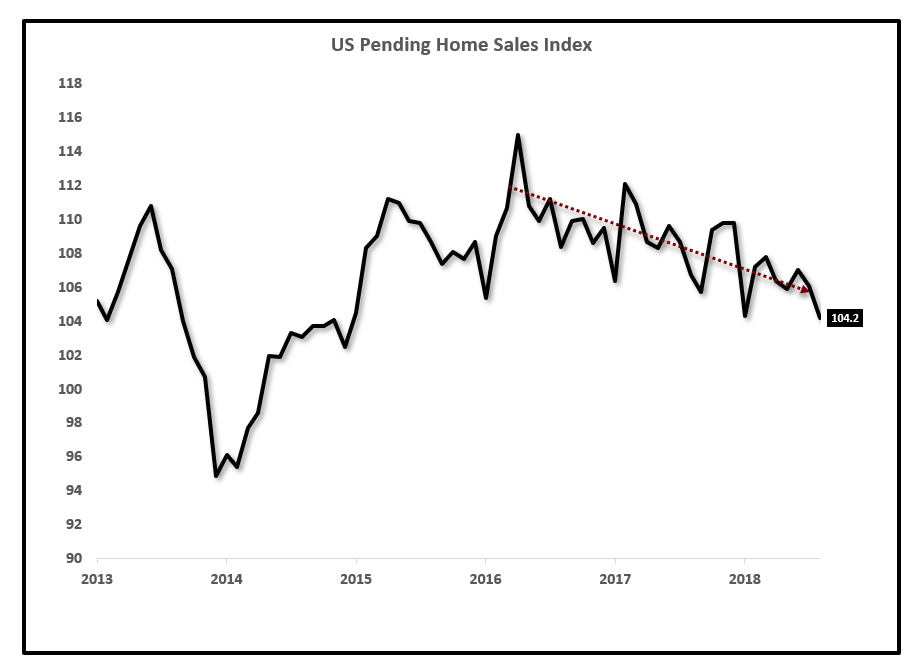

Pending Home Sales are a leading indicator of Existing Home Sales by about two months.

Pending Home Sales measure housing contract activity and is based on signed real estate contracts for existing single-family homes, condos, and co-ops. Because a home goes under contract a month or two before it is sold, the Pending Home Sales Index generally leads Existing Home Sales by a month or two.

The read on Pending Home Sales can give an indication if this weakness in the Existing Home Sales market should be expected to continue.

The Pending Home Sales Index has been contracting recently which provides evidence that this trend is likely to persist.

US Pending Home Sales Index:

Source: YCharts, EPB Macro Research

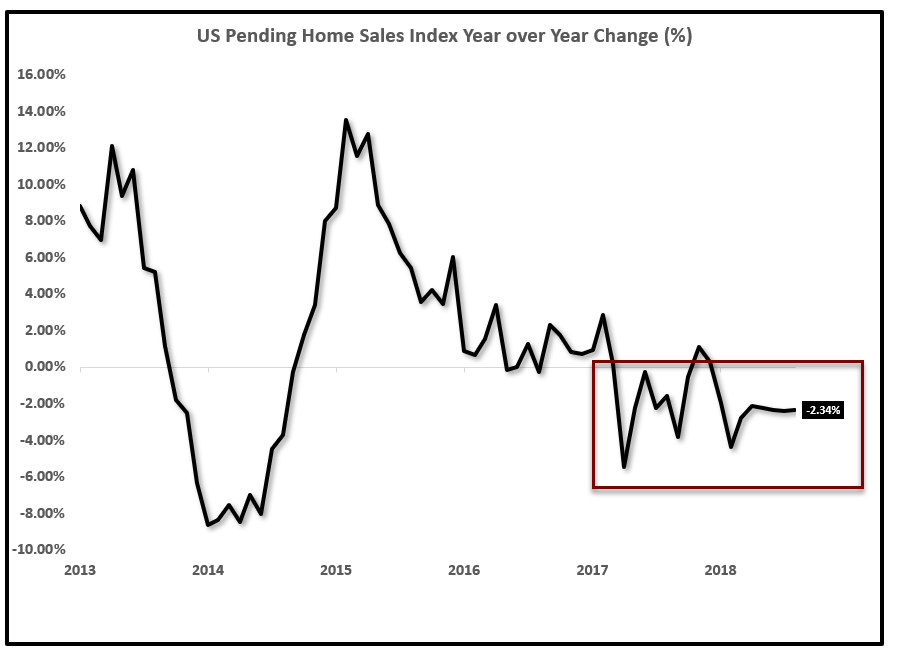

The US Pending Home Sales index has been negative in year over year growth rate terms for nine consecutive months and for 12 of the last 13.

US Pending Home Sales Index Year over Year Change (%):

Source: YCharts, EPB Macro Research

The data suggest that the slowdown emanating from the new construction market that has leaked into the existing home market will continue. How has this impacted real estate prices?

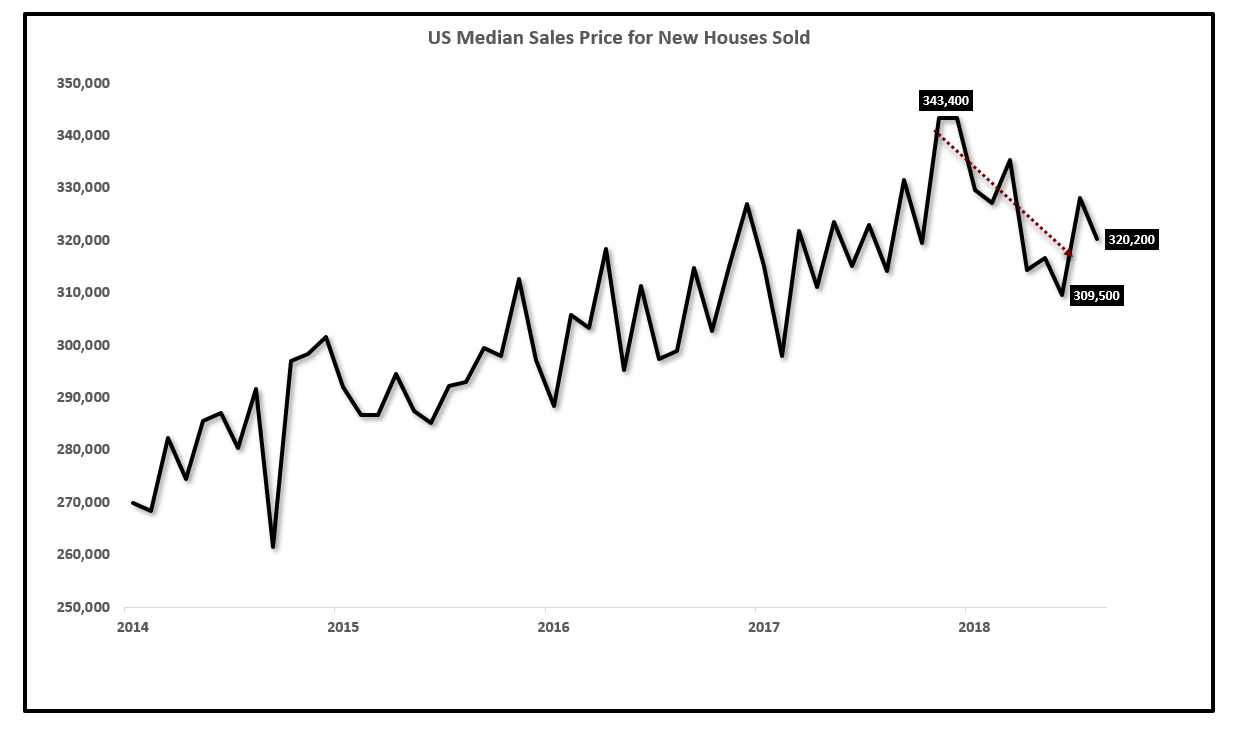

Home Prices Growth Is Still Positive

I should caveat the statement that home price growth is still positive by saying that existing home sales growth is still positive. The data on newly constructed homes shows the median sales price falling and down over 9% from the peak.

As the data on new construction, specifically Building Permits, shows, there is an empirical slowdown that has started in the new construction market that is making its way into the Existing Home Sales market.

Newly Constructed Home Median Sales Price:

Source: YCharts, EPB Macro Research

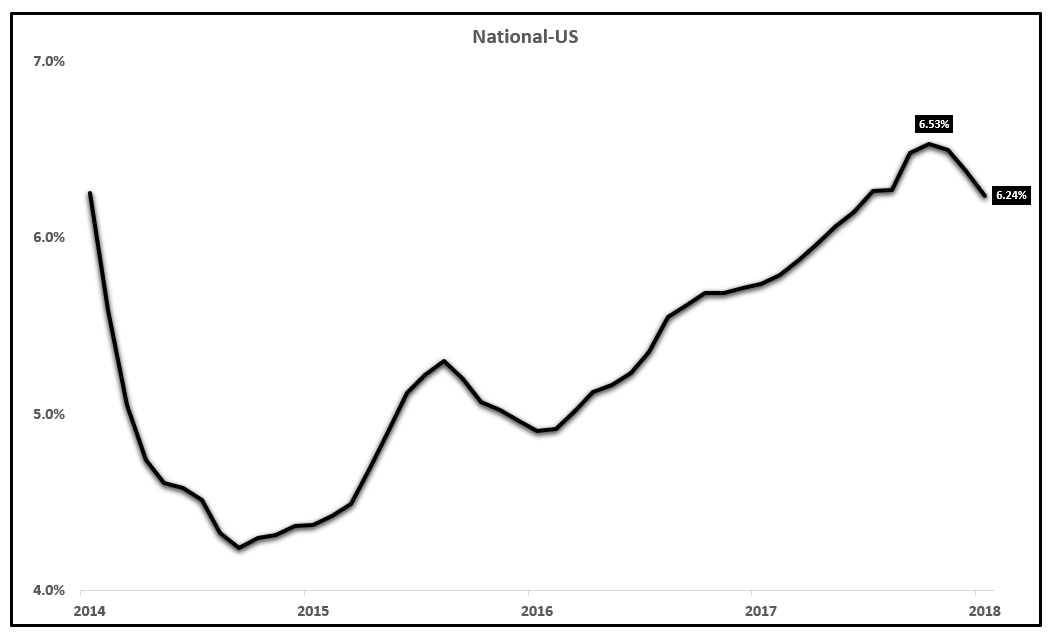

The most popular index on the home price movements of Existing Homes is the Case-Shiller Home Price Index. The Case-Shiller Index shows that home prices are still growing around 6.24% year over year but that the rate of increase has slowed,

Case-Shiller Home Price Index - National Average Year over Year Growth:

Source: S&P, Dow Jones, EPB Macro Research

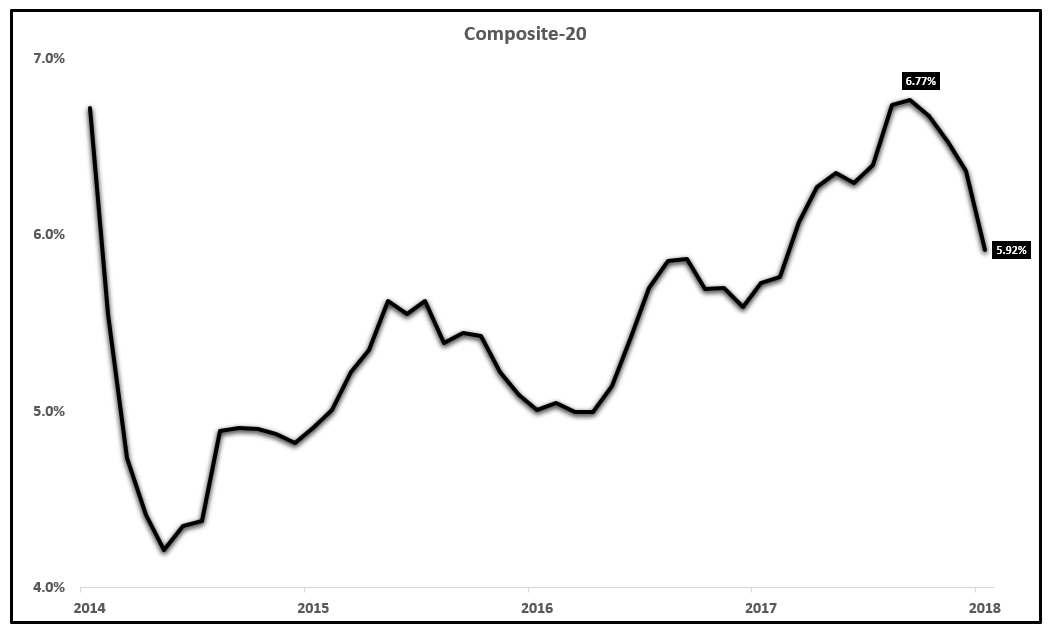

The price growth for the national average index has only dropped from 6.53% to 6.24% but the data on the 20-city composite is slightly more dramatic, falling from 6.77% growth to 5.92% growth.

Case-Shiller Home Price Index - 20-City Composite Year over Year Growth:

Source: S&P, Dow Jones, EPB Macro Research

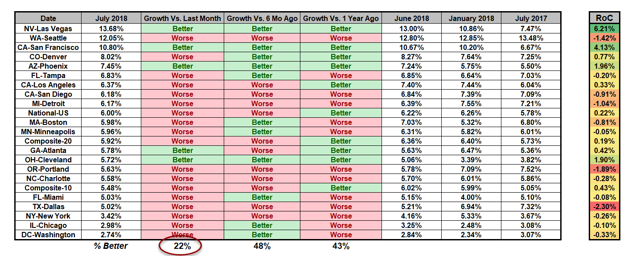

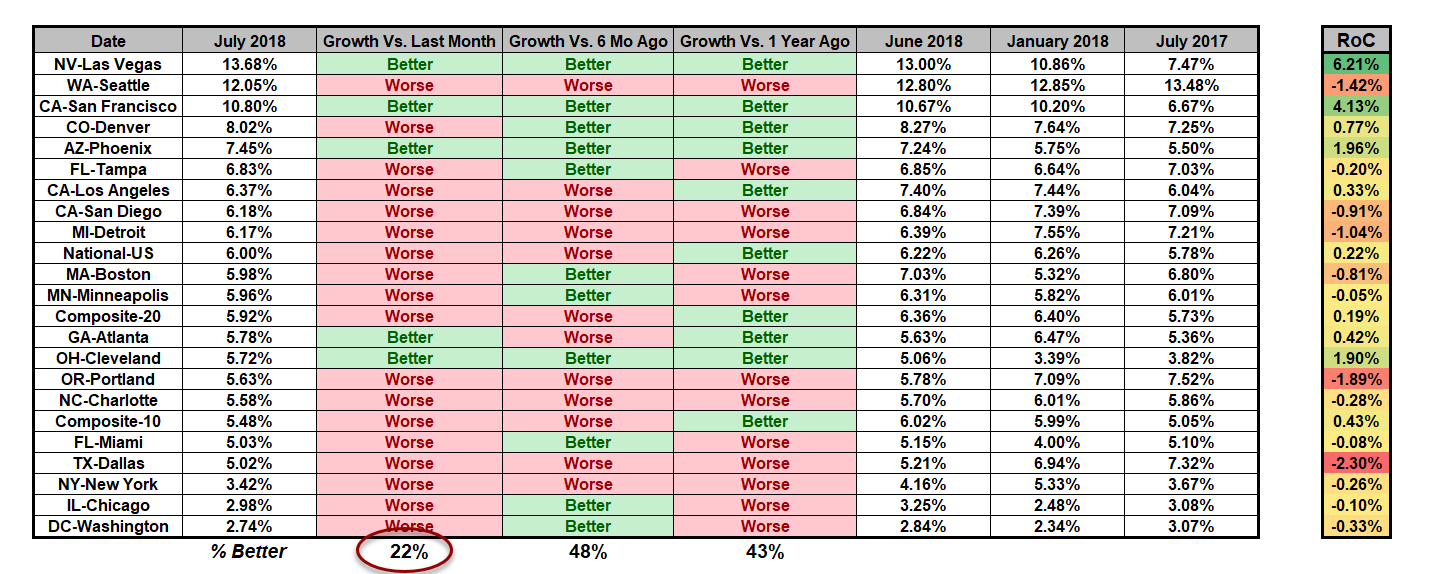

The two following charts are tables that I frequently publish to members of EPB Macro Research that show the 20 major cities and their home price growth as of the last month, one month ago, six months ago, and one year ago for a comparison.

The first table is sorted by the rate of acceleration or the price growth this month compared to the price growth one year ago.

Home Price Index Table By City (Sorted By Rate Of Acceleration):

Source: S&P, Dow Jones, EPB Macro Research

The second table is sorted by the fastest growing cities in terms of home price growth.

What is interesting to note is that only 22% of the cities are showing accelerating rates of growth compared to one month ago and 43% compared to one year ago.

Home Price Index Table By City (Sorted By Year over Year Price Growth):

Source: S&P, Dow Jones, EPB Macro Research

The deceleration in home price growth is not a nitpicky topic but rather an important data point. The previous sections provided evidence for a slowdown in the housing market, starting with the residential construction sector and newly constructed homes. This data was corroborated with decreased prices for newly constructed homes.

Home prices are the last to move so it makes sense that the home prices have not yet started to outright contract in the Existing Home Sales market but the decelerations in price growth are what we should continue to expect.

The data points towards more slowing in the residential construction sector and the existing home sales sector.

Interest Rates?

Isn't this all interest rates? I don't think it is fair to say that this entire move lower in the housing space is due to interest rates but it also wouldn't be fair to say that there is no correlation.

Of course, rising mortgage rates make housing, on the margin, less affordable and the recent rise in mortgage rates is very meaningful and contributory to the declines in the housing market and housing-related stocks.

30-Year Mortgage Rate:

Source: YCharts, EPB Macro Research

We haven't yet seen the impact of the latest move in rates on the housing market. About 100 basis points on a 30-year mortgage have so far caused a roughly 10% contraction in the housing market nationwide.

The data suggests there is more downside to come.

Impact To Housing Stocks - Will It Continue?

As mentioned in the opening section of this note, in-line with the slowing housing data, homebuilder and housing-related stocks have been tumbling, falling as much as 26% in this year alone.

I will be using the iShares Homebuilder ETF as a proxy for housing stock related performance.

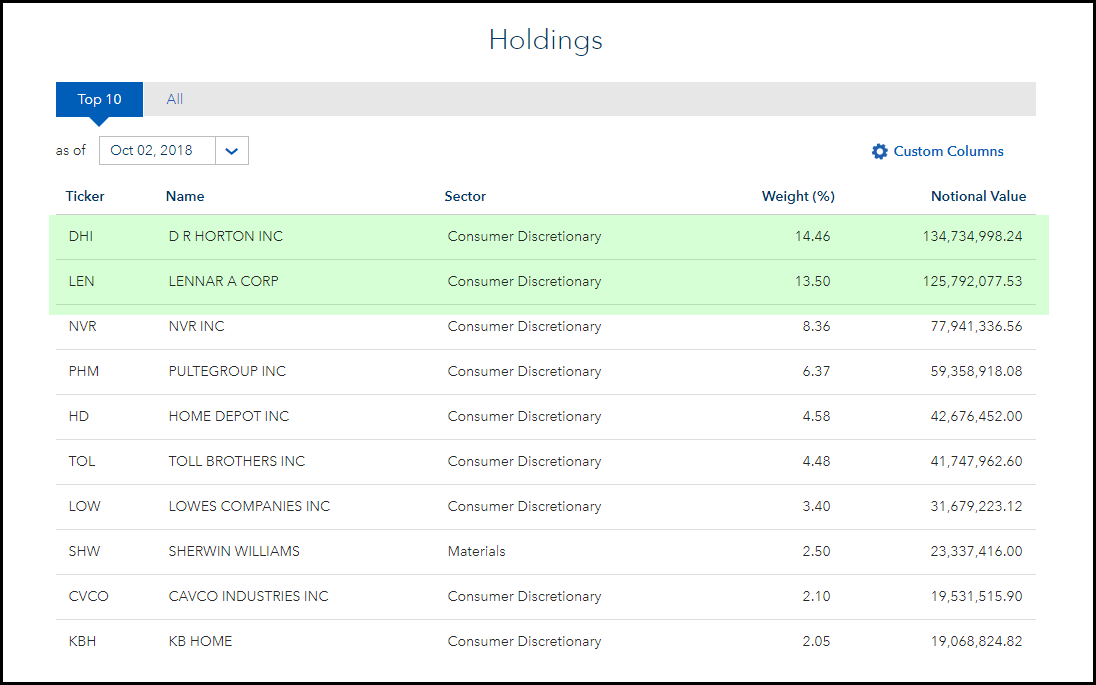

Below is a chart of the top 10 holding in ITB. Popular homebuilder stocks such as D.R. Horton (DHI) and Lennar (LEN) make up as much as 28% of the ITB ETF.

Other home services stores such as Home Depot (HD) and Lowe's Companies (LOW) are in the top 10 holdings as well.

ITB - Top Holdings:

Source: iShares

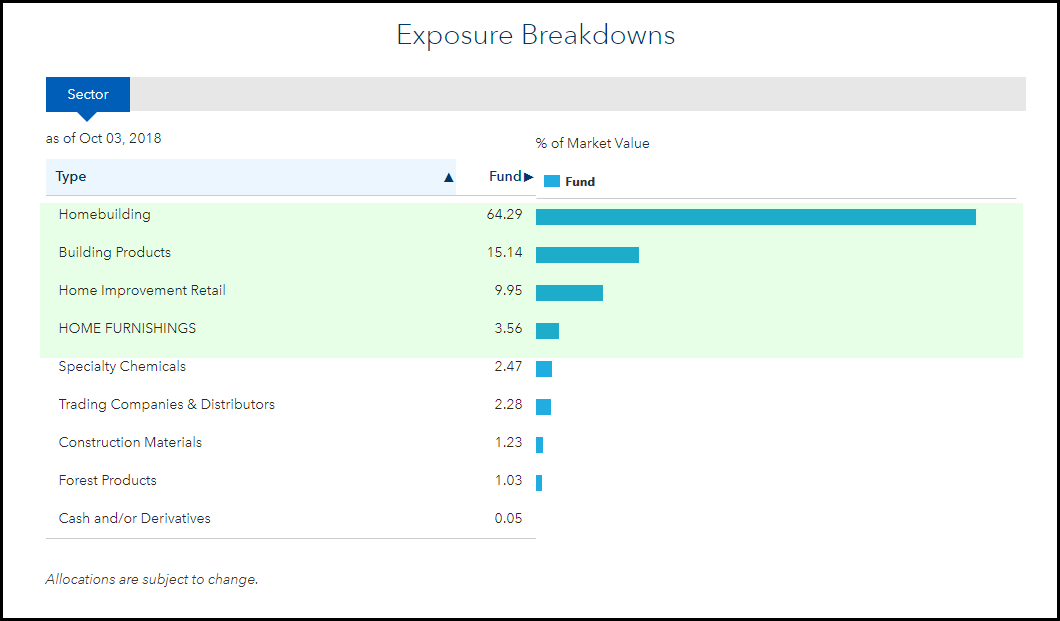

The ITB ETF has roughly 65% exposure directly to homebuilding stocks and less exposure to other housing-related categories.

ITB - Exposure Breakdown:

Source: iShares

The fact that ITB has the largest exposure directly to homebuilding companies explains why the ETF has performed so poorly. As mentioned in the first section on new construction, Building Permits are down. When Building Permits fall, homebuilding companies can post good earnings results but those are backward looking data points and the future then looks less optimistic with declining new construction activity.

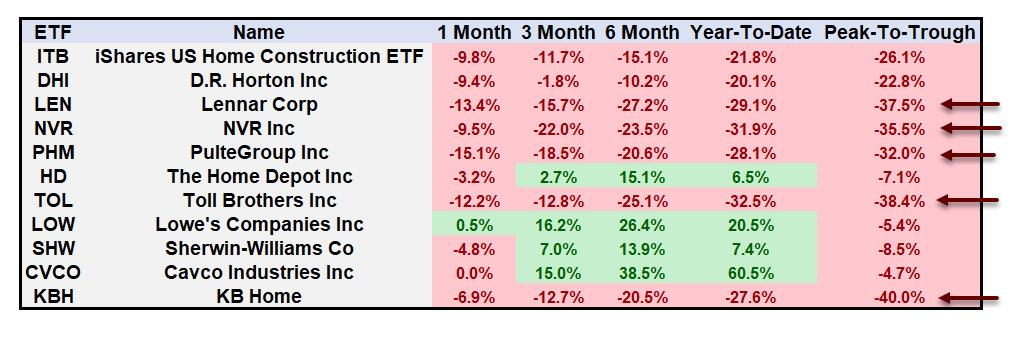

Below is a table that shows the performance of the top 10 holdings in ITB over the past one month, three months, six months, year-to-date and the peak to trough drawdown for this year.

At it sits today, five of the top 10 holdings in ITB are down more than 30% from their highest level this year. Stocks like KB Home (KBH) and Toll Brothers (TOL) are down roughly 40% from their 2018 high. There is real damage that has taken place in the homebuilding sector.

What Is Going On With Homebuilders?

Source: YCharts, EPB Macro Research

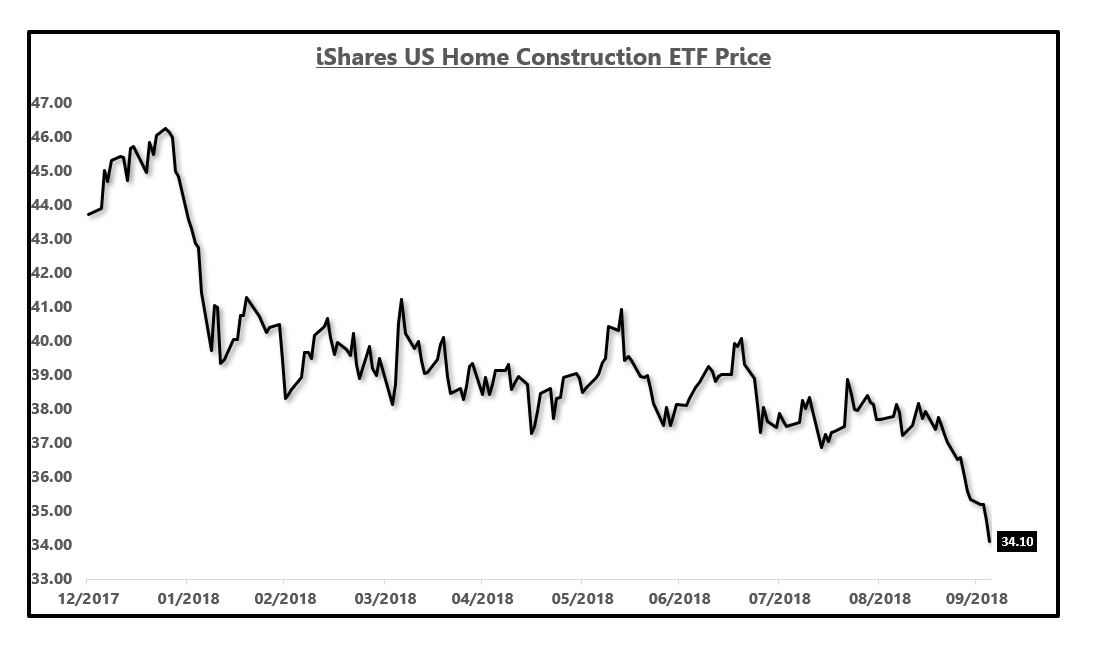

Below is a chart of the 1-year price of the ETF ITB which shows a steadily decline all year. The declines have accelerated in recent weeks.

ITB Performance:

Source: YCharts, EPB Macro Research

The performance relative to the S&P 500 is even more dramatic. The chart on the left is a relative performance spread. As the spread moves lower, ITB is underperforming SPY. As the spread moves higher, ITB is outperforming SPY. We are at the lowest level of relative performance this year for ITB compared to SPY.

The chart on the right shows the difference in 1-year total performance between SPY and ITB.

ITB Relative Performance To S&P 500 (SPY):

Source: YCharts, EPB Macro Research

The housing data is being corroborated by the price action in the homebuilder space, specifically through ETF ITB.

Summary

There is a clear and empirical slowdown in the housing market. Building Permits are contracting and the volume of transactions in the Existing Home Sales market is down.

The price of a newly constructed home has rolled off the peak while Existing Home Prices are rising albeit at a decelerating pace.

The leading indicators of the housing market suggest this trend will continue which then means there is likely more downside for the homebuilding stocks and more downside for ITB.

0 comments:

Publicar un comentario