Who's Left?

by: The Heisenberg

- One persistent question keeps popping up lately in some of the analysis I spend my time perusing.

- That question is this: "Who will be the marginal buyer of equities?"

- There's a sense in which that only matters if the two pillars (buybacks and earnings growth) of the current rally crumble.

- Here's a hopefully useful assessment of equity demand.

- That question is this: "Who will be the marginal buyer of equities?"

- There's a sense in which that only matters if the two pillars (buybacks and earnings growth) of the current rally crumble.

- Here's a hopefully useful assessment of equity demand.

I don't have children, but if I did, I imagine I'd love them all equally, but like some of them more than others.

In that respect, my posts are like my hypothetical kids - I love them all, but I like some more than the rest. That preference shows up in the number of times I refer back to some posts relative to others.

One recent post I find myself linking to pretty often is called "When A Walk To The Park Isn't A Walk In The Park". I chose to present that originally on this platform, but I've written several riffs on it for my site since it was published early last month.

The overarching point in that unnecessarily long piece is that back in January, the trek higher for U.S. equities (SPY) could be properly characterized as a dead sprint. In late January, the Conference Board survey (which goes back some three decades) showed that a record percentage of Americans thought equities would rise in the year ahead. Here's what the chart on that looked like at the time:

(Bloomberg)

That ebullient sentiment was fueled in part by the assumption that the tax cuts in the U.S. would fuel a final, glorious leg higher in stocks - the fabled "blowoff top".

For a minute there, that assumption was borne out, as the S&P blew through half of Wall Street's year-end targets in the space of just three weeks. Global equities were similarly buoyant. For instance, at one point the Hang Seng China Enterprise Index rose for a record 19 consecutive sessions (H-shares are now in a bear market along with their counterparts on the Chinese mainland).

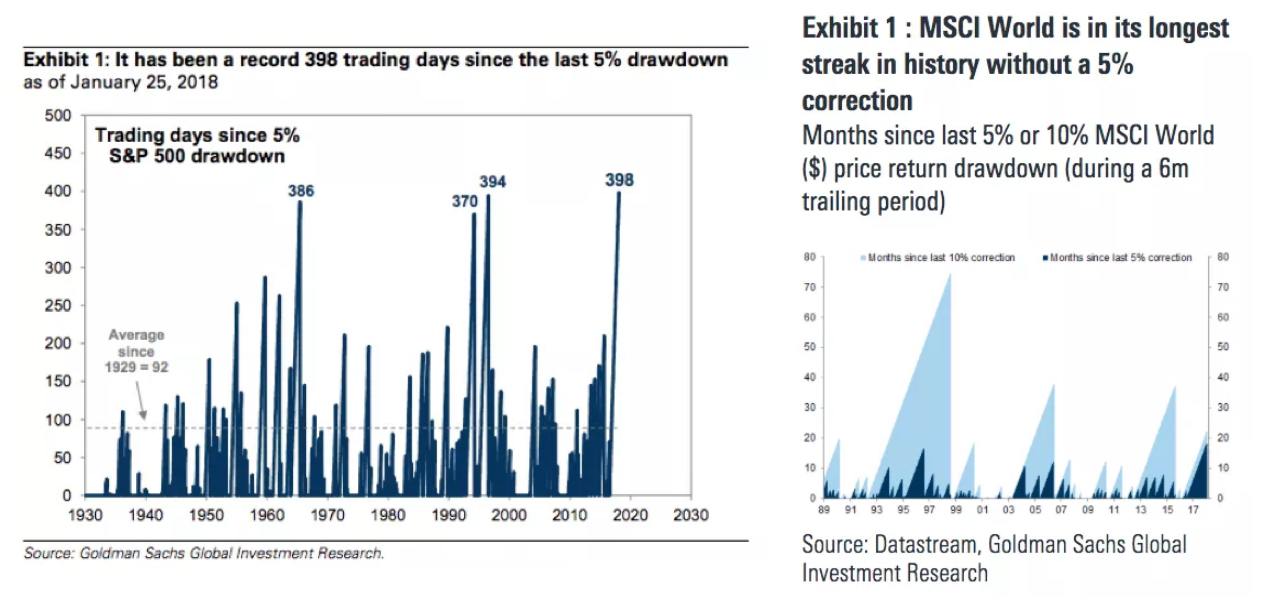

I recounted the evolution of markets in 2018 in a chart-heavy, first half review called "Requiem For A Rally", so I'm not going to subject the folks who read that post to a paraphrased version here. But just to drive the point home about January marking peak euphoria, do note the following two charts I highlighted in that piece which show, from left, that through January 25, the S&P had gone a record 398 days without a 5% pullback and the MSCI world broke a similar record:

(Goldman)

(Goldman)

In the five months since January, the trek higher for U.S. stocks has morphed into a slow, arduous affair akin to trudging uphill, against the wind, where the "wind" is comprised of seemingly incessant headlines about, to name a few, regulatory risk in tech, worries that inflation in the U.S. will accelerate forcing the Fed to lean more hawkish than the market anticipates, emerging market woes tied to the tightening of U.S. monetary policy and, of course, trade wars. The trek higher for ex-U.S. stocks has halted altogether and, depending on the locale, gone into reverse.

Amid the headline risk, one question which has come up time and again, is this: Who will be the marginal buyer of U.S. equities?

Honestly, I'm not a huge fan of that question because it's only relevant if you assume the corporate bid (i.e., buybacks) disappoints and if you believe that earnings growth in the U.S. is likely to decelerate meaningfully in the near term. I don't think either of those things are particularly likely.

Let's take buybacks first.

I don't normally quote mainstream media outlets other than Bloomberg, but I think it's notable that CNN Money has made it a point to highlight the buyback story. They've hardly been the only national news outlet to point out the discrepancy between, on one hand, what was implicitly (and in some cases explicitly) promised by the GOP in terms of what the tax cuts would entail for corporate cash usage and, on the other, reality. I'm not going to get into the political debate for the purposes of this post, but suffice to say the media is pretty keen on letting the public know that while wage growth is still stubbornly refusing to reflect what the Phillips curve would dictate, corporations have not hesitated to plow money into buybacks. The following is from a CNN article published earlier this week, and again, the reason I use it is to illustrate how this has become a national discussion:

Corporate America threw Wall Street a record-shattering party last quarter. Flooded with cash from the Republican tax cut, US public companies announced a whopping $436.6 billion worth of stock buybacks, according to research firm TrimTabs.

Not only is that most ever, it nearly doubles the previous record of $242.1 billion, which was set during the first three months of the year.

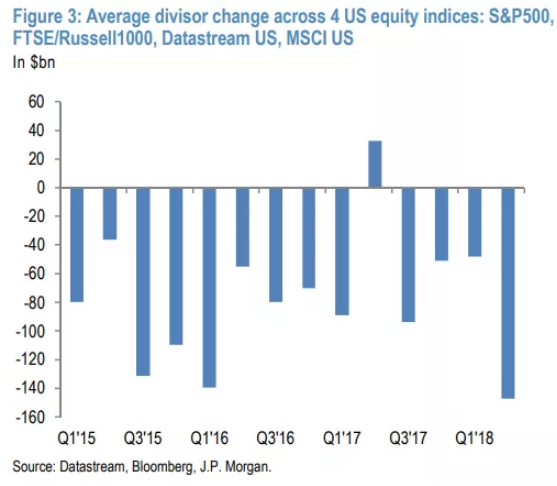

There's an argument to be made that if you're looking to explain how it is that U.S. equities held up in Q2 amid all the headline risk, buybacks are a good place to start. I highlighted the following chart from JPMorgan in a previous post, but I'll use it again here in the interest of backing up that contention:

(JPMorgan)

(JPMorgan)

Normative discussions aside (that's another way of saying I'm not going to debate the social utility of buybacks here), the corporate bid is in place and that's a form of real-life "plunge protection". You don't need any conspiracy theories to employ the "plunge protection" characterization. Recall that back in February, amid the equity rout, Goldman's buyback desk had its second busiest week in history. Here's a quote from a note dated February:

The Goldman Sachs Corporate Trading Desk recently completed the two most active weeks in its history and the desk’s executions have increased by almost 80% YTD vs. 2017.

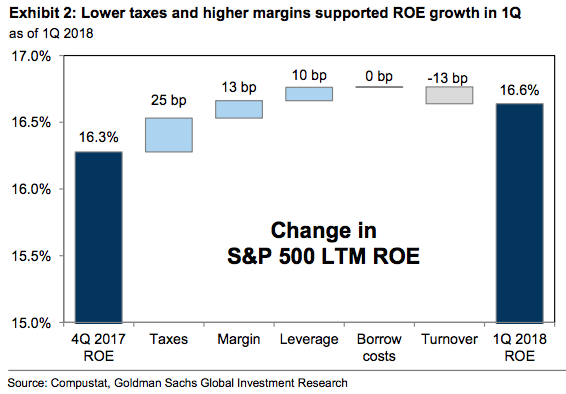

Moving on to earnings growth in the U.S., you should already know the story: Q2 is likely to reflect well on corporate profitability. That's thanks in no small part to the tax cuts. Consider these excerpts, from a Goldman note published on Friday:

Despite valuation risk, strong corporate profitability continues to support equity prices.

S&P 500 return on equity (ROE) increased by 36 bp to 16.6% in 1Q, its highest level since 2011. Profitability is even more impressive excluding Financials. ROE ex-Financials rose by 44 bp to 19.9%, the highest level on record except for 4Q 1997.

Three of the five DuPont factors were tailwinds to S&P 500 ROE in the first quarter.

Lower corporate taxes was the largest tailwind to S&P 500 profitability following the enactment of tax reform in December. A lower tax rate accounted for 25 bp of the total 36 bp increase in ROE in the quarter. Margins also continued their upward climb, providing a 13 bp tailwind to index-level return on equity.

The point here, is that when it comes to the "who will be the marginal buyer of U.S. equities?" question, I'm not entirely sure it needs answering in the near term as long as buybacks continue and as long as earnings continue to come in strong. Additionally, you can expect the buyback bid to be even more pronounced in the event there's a selloff.

So that's my effort to balance things out with the bull case.

With that out of the way, it's entirely possible that corporate profitably has either peaked or is close to peaking. Eventually, margin pressure is going to show up (it's already here in Consumer Discretionary), and if trade frictions end up denting the outlook for growth and prompting guidance cuts from management, well then, the earnings tailwind could abate, even if it doesn't disappear entirely.

On the buybacks, it's important to remember that what incentivized the latest iteration of a years-long bonanza was the tax bill. Once that incentive rolls off, it's likely that the pace of authorizations and executions will slow in the absence of further incentives to employ financial engineering. The backlash against buybacks will gather steam in the event of a Democratic sweep in the midterms.

That's not a prediction about how the midterms will turn out, it's just to say that if they turn out well for Democrats, the issue of corporate cash usage will be a hot topic on Capitol Hill.

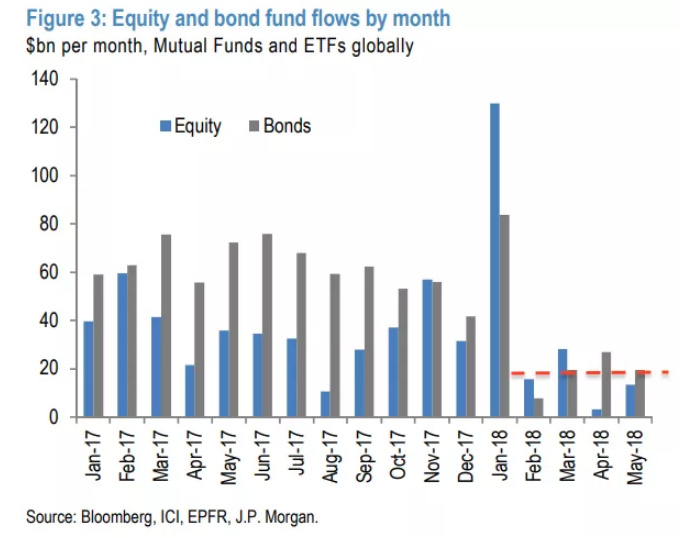

It's therefore possible that the "marginal equity buyer" question will become relevant more quickly than some folks think, and if it does, the following chart and accompanying color from JPMorgan doesn't bode particularly well:

This sharp downshifting in equity and bond fund flows can be seen in Figure 4 which shows the monthly flows across both ETFs and mutual funds at a global level. What Figure 4 also shows is that June was even weaker relative to previous months with practically close to zero flows for both equity and bond funds.

That's a proxy for retail and "hot" money, but what about institutional investors and systematic re-risking?

One thing worth noting is that the idea of trend followers adding to exposure depends on momentum signals and also on volatility. While an in-depth assessment of that is well beyond the scope of this post, the bottom line is that sideways markets pose a challenge to the systematic re-risking thesis. Here's SocGen, from a note out last month:

Markets are pulled by the promises of late stage economic growth boosted by monetary and fiscal stimulus. They are also contending against the risks of rising geopolitical tensions and the likelihood of potential recession. So they end up moving up and down with no clear direction. Such sideways markets are challenging for convex strategies such as trend following systems.

Meanwhile, from an asset allocation perspective, there's reason to believe that globally, investors are bumping up against the limits of their prospective equity exposure. This is another one of those instances where I'm not sure how much detail readers on this platform are prepared to stomach, but what I've discovered recently is that people here seem to appreciate it when I hit the high points and provide a reference link for anyone interested in exploring things further.

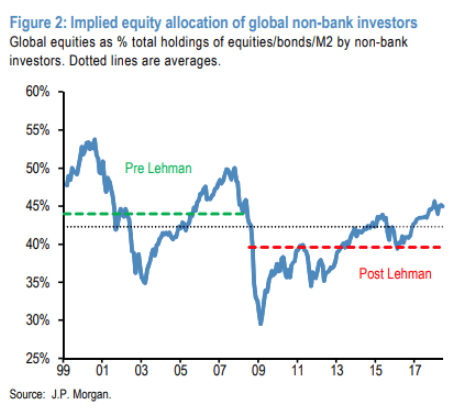

Here's the short version. According to a recent analysis by JPMorgan's Nikolaos Panigirtzoglou, global non-bank investors have an equity allocation of about 45%, which he reminds you is “well above both the 40% post Lehman average and the 43% longer term historical average”.

(JPMorgan)

(JPMorgan)

That, in turn, means that non-bank investors' allocation to bonds and cash is below the post-Lehman average. With the burden on private investors vis-à-vis absorbing fixed income supply set to rise as G4 central banks normalize their balance sheets, it's not clear that it's realistic to expect global equity allocations to have much upside from here.

Coming full circle, what's needed for U.S. stocks to get back to the dead sprint higher that characterized the January rally is a resumption of steady retail flows, a decisive shift in momentum indicators coupled with a durable collapse in realized volatility that together green-light systematic re-risking and, perhaps, a sign from Jerome Powell that the Fed is prepared to slow the pace of rate hikes in the event trade frictions warrant a rethink of policy.

In the absence of those conditions, you're left to lean on buybacks and earnings growth.

The good news, for now, is that those two pillars have virtually never looked stronger.

0 comments:

Publicar un comentario