I Called A Currency Collapse

by: The Heisenberg

- On Friday, the market witnessed one of the worst currency collapses in recent memory as the lira suffered an outright meltdown.

- I have warned about this explicitly for months and what happened this week is "Exhibit A" in why it's important to understand the intersection of geopolitics and markets.

- This episode is one for the history books, so I think it's important for me to go through it for my readers on this platform.

- This is a comprehensive take with all the usual trenchant analysis and every chart you need to understand it.

- I have warned about this explicitly for months and what happened this week is "Exhibit A" in why it's important to understand the intersection of geopolitics and markets.

- This episode is one for the history books, so I think it's important for me to go through it for my readers on this platform.

- This is a comprehensive take with all the usual trenchant analysis and every chart you need to understand it.

I thought long and hard about how I wanted to frame this post, and on Saturday morning, I settled on an angle I hope will convey everything I want to convey to readers here in a reasonably concise manner.

Readers on this platform often characterize me as a "popular" financial blogger. Some authors on this platform have used that same characterization in their own articles when they mention me favorably or unfavorably, whichever the case may be.

Here's a reality check: I am not a "popular" financial blogger. My follower count on this platform is paltry compared to, say, the social media follower counts of even reasonably well known financial reporters from mainstream media outlets. The most "popular" financial bloggers have hundreds of thousands and in some cases millions of followers on Twitter. As far as my own site goes, it's "popular" as far as finance-focused blogs written by one person are concerned, but that's not saying a whole lot. I'm reminded of a friend of mine who's "famous" in the photography world. Just to give you an idea, his second biggest collector is Elton John, but as he often jokes, the words "photographer" and "famous" aren't really compatible outside of Ansel Adams. The irony is, I'd almost invariably be more "popular" if I didn't use the pseudonym. Contrary to what most readers seem to believe, I do not use the nom de plume to attract followers.

Ok, so what's the point? Well, the point is, if I were really a "popular" financial blogger, I would have been asked to show up on every mainstream financial media outlet on the planet on Friday morning and maybe even on media outlets that don't generally focus on finance, because I called the collapse of the Turkish lira - full stop.

Obviously, the lira's Friday plunge was the biggest story in the financial universe and it catalyzed a bout of risk off sentiment across assets and across markets. Turkey's plight is the most poignant example in recent memory of why it's important to understand the intersection of geopolitics and finance. That intersection is my raison d'être.

As the title here suggests, this isn't a case where there's room for interpretation or where it's possible to argue that I didn't provide folks with unequivocally actionable information. I've warned for months on this platform that Turkey was in trouble and I'll give you some examples below, but first let me say that like any good webmaster, I monitor referral traffic on my personal site (i.e., how visitors who don't come in directly end up reading my stuff). In the short history of my site, a sizable amount of that referral traffic has come from this platform, which by definition means that some readers here have read my work over there. Well, I've been writing breathlessly over there about the likelihood of a collapse in the Turkish lira since the beginning of the year and actually, well before that. The bottom line is that the Turkey archive on my site is a veritable museum of bearish lira articles with calls that are as overt as overt gets.

I've deployed sarcasm, dark humor, in-depth analysis of the underlying economic fundamentals, exhaustive political commentary, and pretty much every tool at my disposal while pounding the table on this.

To be clear, it doesn't matter one way or another to me if anybody besides a handful of my analyst friends acknowledges how prescient those calls were. If I were looking for recognition, I obviously wouldn't use a pseudonym. You know how people like to use obsequious praise in the "testimonials" sections of their websites, ostensibly to impress new readers? Right, well here are two of the quotes I use in my "testimonials" section (and these are real reader comments, by the way):

You are a dark cloud on a sunny day.

May Santa leave you an extra lump of coal in your stocking.

Fun stuff, no?

But while I don't care about the recognition, what I do care about is making sure the relatively small number of readers I do have understand what went on with the lira on Friday, what it portends for markets going forward, and what it says about why it's important to understand markets in the context of geopolitics.

I'm going to try and strike a reasonable balance here between rigor and conciseness. Clearly, this is a long and winding tale and I've given you a link to all the analysis and information you could ever want, so I don't feel like I need to hit every possible angle in this post. What I will do, though, is summarize the important events and put them in the context of the broader market discussion.

Over the course of 2018, the Turkish lira has depreciated rapidly thanks to idiosyncratic internal factors and a less favorable external backdrop for emerging markets. The idiosyncratic internal factors mostly stem from President Recep Tayyip Erdogan's ongoing quest to consolidate power. Erdogan harbors a set of famously unorthodox views about interest rates, the currency and inflation. Specifically, Erdogan is the self-declared "enemy of interest rates", which he calls "the mother and father of all evil." To be sure, the market is used to that kind of rhetoric from Erdogan, but as inflation started to spiral out of control, his antics acted as gasoline on the fire by reinforcing the notion that the Turkish central bank would be loath to hike rates in order to shore up the flagging currency and arrest the rise in inflation.

I told you earlier in this post I would give you some examples from articles I've penned for this platform warning about the lira. Let me do that now. On May 13, when the lira was at 4.30, I said the following in the first of what would end up being a series of posts centered around comments Jerome Powell made about emerging markets at an IMF/SNB event:

In case you were under the impression that Erdogan is going to be inclined to moderating his stance on interest rates (which, in his bizarre version of economics, cause inflation if they're too high) he is going out of his way to ratchet up the rhetoric and disabuse you of that idea on a daily basis. "If my people say continue on this path in the elections, I say I will emerge with victory in the fight against this curse of interest rates", he said in Ankara on Friday.

You’re reminded that he is saying that amid an acute run on the currency that’s seen the lira make fresh all-time low after fresh all-time low over the past couple of months. It is insane that he would continue to parrot his "I'm the enemy of interest rates" line when the currency is in free fall, especially considering the iron grip he has over the country's institutions (i.e., the central bank isn't really independent).

A week later (so, on May 19), in the second installment of the series of posts mentioned above, I said this:

Do you know what Erdogan did this week? He went on Bloomberg TV and all but confirmed that once next month's election is out of the way, he's going to effectively commandeer monetary policy. You can watch that interview for yourself here, but suffice to say it pushed the beleaguered lira to a fresh all-time low and confirmed everyone's worst fears about what's going to happen once he officially consolidates power.

I'm going to spare you further examples because I imagine you get the point. Do keep in mind that those comments are from mid-May, when the lira was trading at roughly 4.40. At one point on Friday, it breached 6.80.

Key to this story is understanding that to anyone who has followed Erdogan over the years, it was abundantly clear that his April decision to bring forward a landmark election aimed at consolidating power by some 18 months was a decision based on expediency. The lira was already down sharply on the year and it seemed as though he was keen to get the election out of the way in case things got worse.

Unfortunately, traders and investors didn't appear to understand that. Rather, the Turkish lira actually rallied on April 18 when Erdogan set the date (June 24) for the elections. The excuse traders cited for that rally (and I just had to hold my tongue when speaking to a few FX traders) was that getting the election over with would "reduce uncertainty". That was true in a sense. The problem, though, was that traders didn't seem to understand what it was that would be "certain" after the election. For one thing, it was "certain" that Erdogan was going to win, one way or another. More importantly, it was "certain" that he would immediately move to effectively commandeer the central bank and as noted above, he said as much (explicitly) on Bloomberg Television in May.

In the lead-up to the election, Erdogan countenanced a series of measures by the central bank to try and rein in the lira. I lampooned every, single one of them. For instance, the first line of my April 25 post commenting on a 75 bps hike to the late liquidity window (which at the time was still the preferred policy tool) read as follows:

Yeah, I could be wrong, but I don’t think this is going to be sufficient.

A month later, the central bank delivered a 300 bps late liquidity window hike. Commenting on Turkish officials' characterization of that hike as "powerful monetary tightening" I said this:

To say that’s debatable would be an understatement and much like Kuroda’s “very powerful” easing has failed to engineer a sustainable rise in Japanese inflation, one imagines CBT’s “powerful” tightening will fail to arrest double-digit inflation in Turkey.

A week later, the central bank "simplified" monetary policy, which essentially entailed restoring the one-week repo rate as the policy tool. On June 7, they hiked that rate by 125 bps. The lira rallied sharply and the title on my post documenting that speaks for itself:

Market Super ‘Impressed’ With Rate Hike From Turkey As Everyone Temporarily Forgets Who Is Really In Charge Over There

Fast forward to June 24 and Erdogan of course prevailed in an election that consolidated his power in a new executive presidency. Having learned absolutely nothing, traders bid up the lira. On July 9, Erdogan installed is son-in-law Berat Albayrak as head of the economy and the reshuffle left no room for market favorite Mehmet Simsek, generally seen as the last bastion of discipline in Erdogan's inner-circle.

At the same time, Erdogan amended the central bank's articles of association to give himself more sway. Markets were incredulous. Here's what ABN Amro’s Nora Neuteboom said at the time:

This is absolutely not what we hoped for. Markets were awaiting the cabinet appointed and the signal is clear: it is not market-friendly, but rather Erdogan-friendly.

Somehow, consensus was still betting on a ~100 bps hike from the central bank on July 24 and guess what? It didn't happen. They stayed on hold despite runaway inflation.

Playing out in the background was a worsening diplomatic row between Washington and Ankara over the detention of North Carolina pastor Andrew Brunson. It is critical that anyone who fancies themselves a keen observer of macro trends understand the Brunson story for what it is. This is just another episode in Erdogan's long-running quest to secure the extradition of his arch nemesis Fethullah Gulen, the Pennsylvania-based cleric who Erdogan blames for everything under the sun including, of course, the failed coup attempt in 2016. When the Trump administration threatened sanctions on Turkey in connection with Brunson's detention, I penned a short history of the Gulen story and at the end of that post, I said this:

For traders and, perhaps more importantly, for asset managers, this is just further evidence that Turkish assets are anything but attractive following last month’s election.

While EM fund managers will claim to understand all of this, it still feels like there’s a generalized unwillingness to accept the reality of this situation.

Accepting idiosyncratic, country-specific risk is part and parcel of investing in emerging markets, but this has gone well beyond that. This is Erdogan–specific risk and he has shown time and again that betting on him to abruptly step out of character and demonstrate some semblance of rationality is fool’s errand.

That was on July 26. Predictably, Erdogan refused to budge when it came to releasing Brunson precisely because Turkey is using him as leverage in an effort to secure three outcomes:

- the extradition of Gulen

- the return of jailed banker Mehmet Hakan Atilla

- lenient treatment of Halkbank

Those latter two demands are tied to the infamous Reza Zarrab case. Zarrab is the former gold trader implicated by the U.S. in a Turkish plot to skirt U.S. sanctions on Iran. Atilla, his co-defendant and a Halkbank employee, was convicted earlier this year for his role in the scheme and sentenced to 32 months in prison in May.

According to multiple media reports, the U.S. and Turkey had reached a tentative deal that would have sent Atilla back to Turkey and ensured the Treasury would go easy on Halkbank, in exchange for the release of Brunson. For whatever reason, that fell apart late last month.

Then came the sanctions.

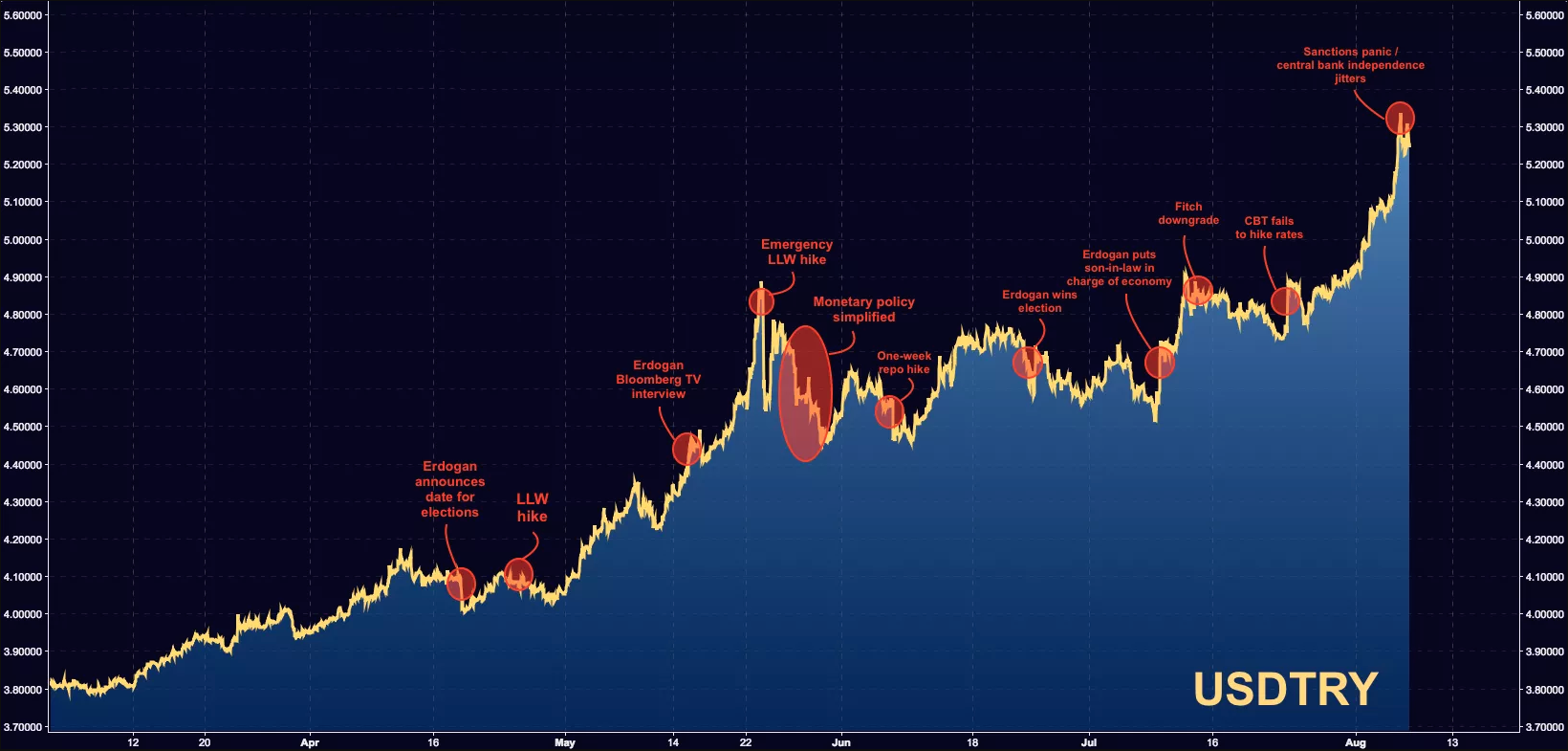

Ok, now let's get to some charts. Here is the definitive annotated lira chart that shows you when everything noted above happened (for the sake of scale, this only runs up to the beginning of this week, when the chart went parabolic):

(Heisenberg)

As all of this was unfolding, 10Y yields in Turkey surged above 20%:

(Bloomberg)

Want to see what panic looks like? Take a gander at yields on Halkbank's June 2020 dollar bonds:

(Bloomberg)

Yeah. That's trouble right there.

So that was the setup for Friday's collapse in the lira. Thursday was rough for the currency, but it started to go further off the rails on Friday in Asia when Japanese traders were stopped out of TRY/JPY positions. That was a repeat of a similar episode on May 23.

Well, just after midnight in New York, the Financial Times reported that the ECB is starting to get concerned about the exposure of Banco Bilbao (BBVA), UniCredit (OTCPK:UNCFF) and BNP Paribas (OTCQX:BNPQF) to Turkey. That catalyzed a sharp drop in the euro (FXE) and concurrent rally in the dollar.

(Heisenberg)

(Heisenberg)

Hours later, the bottom fell out for the lira, which careened a truly harrowing 13% lower ahead of an expected speech from Erdogan. When Erdogan took the stage in Turkey (around 7:30, New York time) he said precisely the opposite of what the market wanted to hear.

Specifically, he railed against higher interest rates, characterized FX volatility as "artificial" and, worst of all, implored Turkish citizens to reach under their "pillows" and trade in their dollars, euros and gold for lira.

Erdogan would go on to make a similar speech later, and while he was between rallies, Donald Trump announced on Twitter that the U.S. will double metals tariffs applicable to Turkey.

By the cash open on Wall Street, the lira was basically no-bid.

(Heisenberg)

(Heisenberg)

I realize those day charts are sometimes hard for folks to wrap their heads around, so let me pan out and put this in context. Here's a two-year chart:

(Heisenberg)

(Heisenberg)

The iShares MSCI Turkey ETF (TUR) traded some 1 million shares in the pre-market on Friday, the most ever. In regular trading, the product crashed as much as 22% early on, before paring losses. Still, the vehicle ended up logging its worst week in history. If you invested in this product at the highs in 2018 without understanding the extent to which your investment depended on the evolution of Turkish politics, you are probably scratching your head right about now.

(Heisenberg)

(Heisenberg)

So what does all of this mean going forward? Well, for one thing, it means you need to watch BBVA, UniCredit and BNP Paribas. You can debate the extent to which they're exposed, but it's worth noting that late last month, Steve Eisman (of “The Big Short” fame) told Bloomberg Television that he’s shorting BBVA and UniCredit based on their “fairly large exposures to Turkey.”

More broadly, watch the European banks as a group. The Stoxx 600 banks index was already nursing a 16% loss off this year's highs prior to Friday. I'm not sure the prospect of a European "operation twist" bodes particularly well for margins and the market is still extremely concerned about Italy's fiscal path.

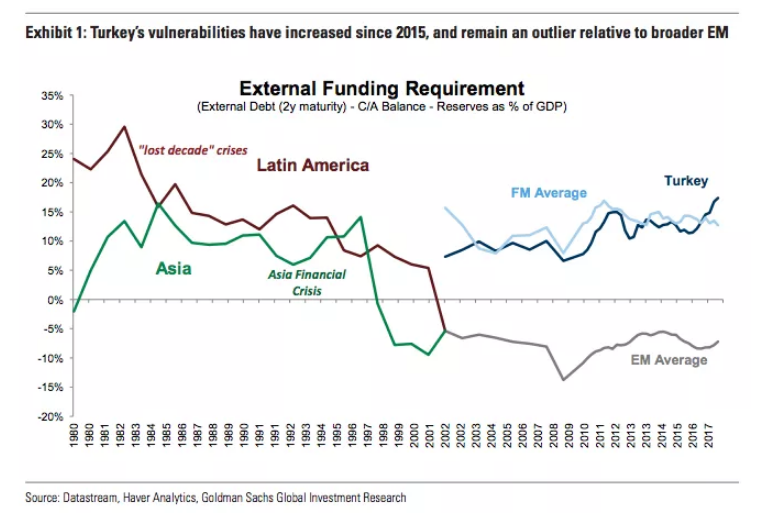

For emerging markets, analysts were out in droves on Friday in an effort to remind everyone that Turkey is not an emerging market bellwether. Probably the most important chart in that regard is this visual from Goldman:

(Goldman)

(Goldman)

Essentially, Turkey is a frontier market when it comes to its reliance on external funding, so extrapolating to the broader EM complex probably isn't warranted.

That said, do keep in mind that this is playing out against an exceptionally unfavorable external backdrop. An unapologetic Fed continues to hike rates and on Friday, the latest CPI data showed core inflation in the U.S. rising at the fastest pace since 2008. In short, Jerome Powell is probably going to keep hiking, which means emerging markets are going to be under pressure.

The MSCI EM Currency Index fell the most since May of 2017 to close the week:

(Heisenberg)

(Heisenberg)

As far as the lira and Turkey in general are concerned, it's now deteriorated to the point where there are basically two options: an IMF bailout or capital controls. We're past the point of no return when it comes to whether a rate hike would work to arrest the slide in the currency. It would probably take a hike of at least 1,000 basis points to make a dent in this. The idea that Erdogan would allow that seems laughable.

On Friday evening, Bloomberg reported that banks in Turkey were struggling to meet customer demand for foreign currency. In short, Erdogan needs to do something right now, this weekend, or risk next week being a tipping point.

Although the fundamentals in the broader emerging market space are much better than they are in Turkey, you want to keep in mind the Fed (as mentioned above) and also the fact that the U.S. is pursuing a tougher sanctions regime on Russia. The ruble just had a rough week and the threat of sanctions on sovereign debt bodes particularly ill for the country's assets. If Erdogan imposes capital controls, it would almost invariably create a crisis of confidence in emerging markets considering the current environment of a hawkish Fed and an administration in Washington that's increasingly prone to leaning on sanctions and tariffs when it comes to foreign policy.

For anyone caught up in this (which, by the way, was everyone on Friday considering how the lira collapse rippled across markets), do remember that this was entirely predictable.

And so is what comes next if something doesn't get done over the weekend.

0 comments:

Publicar un comentario