GLD Options Are Looking Quite Attractive

by: Lyster Analytics

- Gold is currently realizing unusually low volatility, which is unlikely to last very long.

- I see various serious risks seemingly unaccounted for by Mr. Market.

- On an implied vol basis, gold options are a cheap and effective hedge against these risks.

- I see various serious risks seemingly unaccounted for by Mr. Market.

- On an implied vol basis, gold options are a cheap and effective hedge against these risks.

Investment Thesis

Long-dated tail options on GLD are looking like a very cheap hedge against monetary and political risks, many of which loom on the horizon. If (or when) these risks become glaringly obvious to markets over the next few years, price movements in gold are likely to react accordingly.

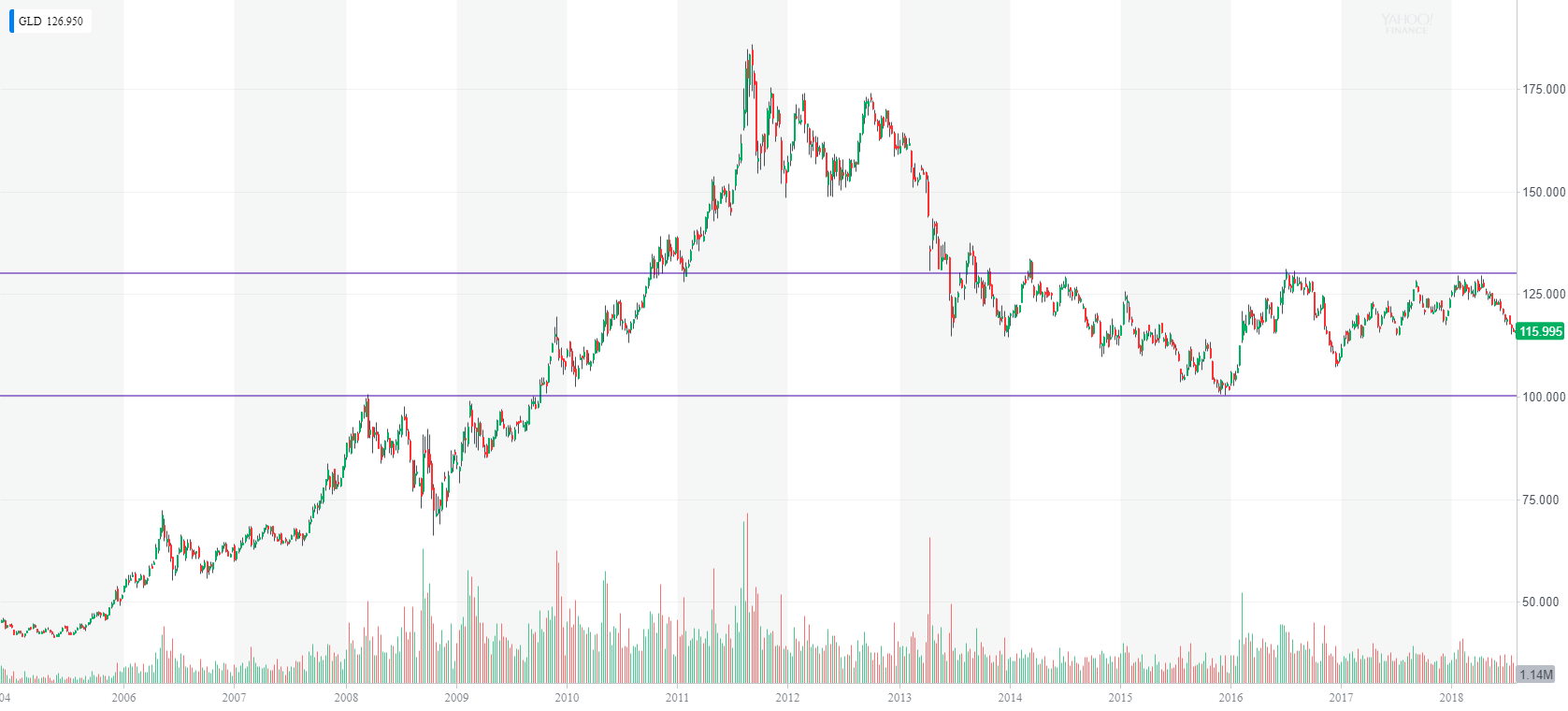

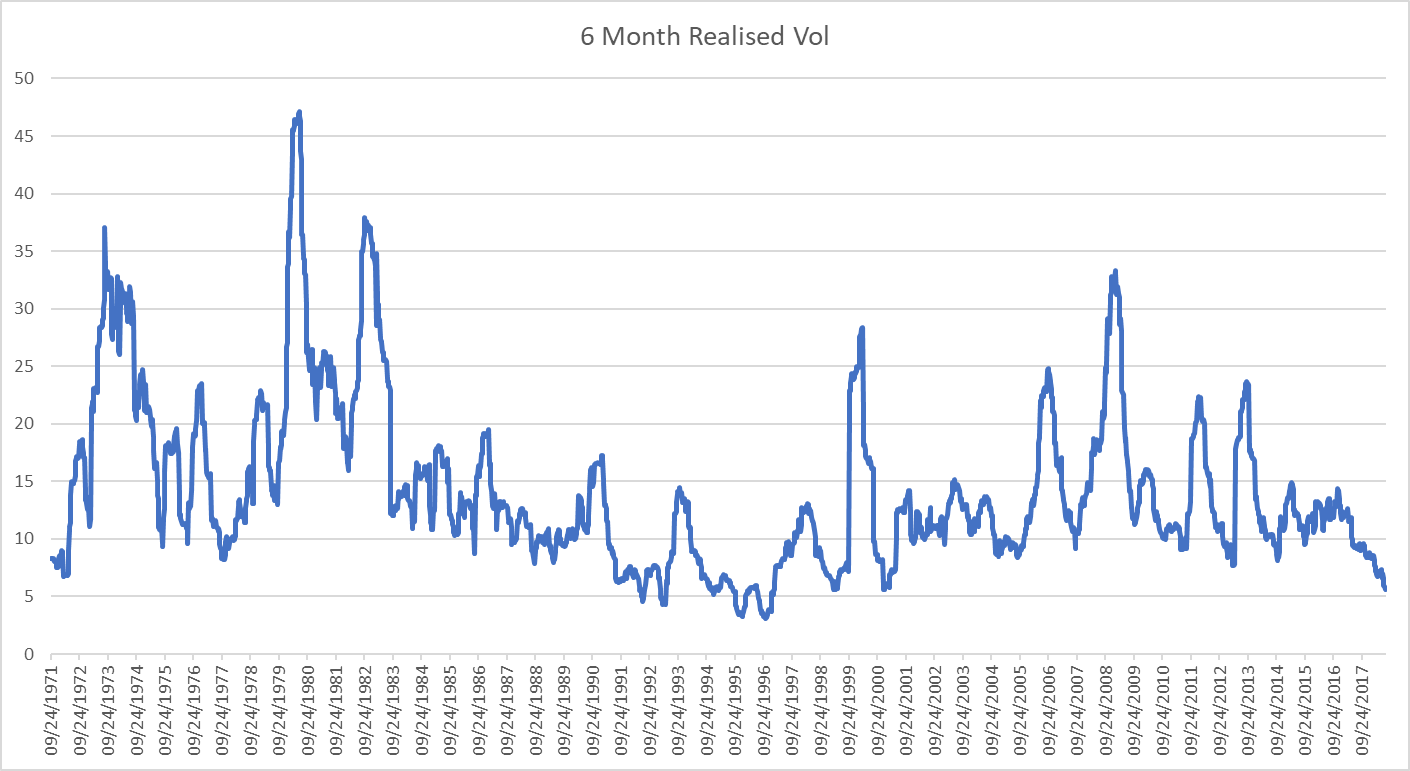

Gold and precious metals in general, have received very little attention in mainstream financial media in recent years and rightly so: In the current Goldilocks period of strong economic growth, low inflation and sturdy financial markets, there seems to be very little potential for either large upside or downside movements in the price of gold. Post 2012/2013 correction, the SPDR Gold Shares ETF (GLD) has been hovering around the 100-130 level with low volatility, historically low volatility to be clear. Trailing 6-month realized volatility of gold currently stands at 5.63% annualized, well below the historical average of around 14% - the lowest it has been since 1997 (FRED).

Source: Yahoo Finance, Available: GLD Interactive Stock Chart | SPDR Gold Shares Stock - Yahoo Finance

I believe, however, that the macro environment is setting the stage for what may be a period of global monetary shenanigans that should beget significantly higher vol in the price of gold. Setting aside the stew of non-US risks such as the risk of Italy’s new regime to the Euro, China’s dangerous debt situation, trade wars, divergent monetary policy and various geopolitical risks (all of which I believe pose a great threat to stability in financial markets) - my bold prediction for the US macro environment going forward, is as follows:

The fed has turned on auto-tightening, draining dollar liquidity and raising short end rates (long-term rates too, just not nearly at the same pace - hence the gradually inverting yield curve). The treasury is planning to issue new debt to finance Trump’s $804 billion deficit (bearish for bonds, i.e. higher yields) This has been strong for the dollar, and will quite likely be for as long as the Fed keeps auto-tightening engaged (which is likely given that strong economic data continues to roll in and inflation has been ticking higher).

The double whammy of a strong dollar and attractively yielding treasuries will continue to be a short-term downer for the price of gold. Higher rates will have a bite on the real economy and at some point (nobody knows when, but my feeling is sooner rather than later) US equities will take a hit (then of course global equities will too). When equities do unfold, they will do so rapidly (if you would like to know why, I recommend reading Volatility and the Alchemy of Risk by Chris Cole of Artemis Capital Management).

Central bankers will be caught off guard (as they always do) and therefore it is likely that in response to financial turmoil of this kind, the Fed and CB’s globally will resort to a second wave of unorthodox stimulus/QE/money synthesis that will test the market’s trust in central bankers (and fiat currency) in a very real way. Ultimately, as this scenario begins to play out and the atmosphere in markets will shift from elation to uncertainty/fear as CBs and governments try pull a rabbit out of a hat. A significantly higher price of gold should reflect this, as it did in the years succeeding the GFC.

To summarize, there is great potential for both: A) significantly higher treasury yields and a stronger dollar in the short term (which I believe provides a great entry point for this trade) and B) a market crash/recession/monetary policy freak out and U-turn that will ensue. It is this potential that does not seem to be priced into GLD options.

To buy pure long-term volatility exposure, with no directional bias one would buy an equal quantity of both ATM calls and puts on GLD at a given expiry date far into the future (a straddle). Analysis of return data, along with some intuition, would suggest that owning tail options on the right tail of the distribution makes more sense. Statistical analysis of the monthly return data of USD-Gold since 1971 (sourced from FRED) suggests there is a positive skew to the return distribution of Gold, with a moment coefficient of skewness of +1.163.

This makes sense intuitively as gold is a commodity that is thought of as a safe haven asset that some investors keep as an important “keep and hold” part of their portfolio and others rush to buy in times panic or uncertainty. In other words, those who own gold are usually in no rush to sell it but those who do not own gold, in times of panic every so often, do rush to buy it.

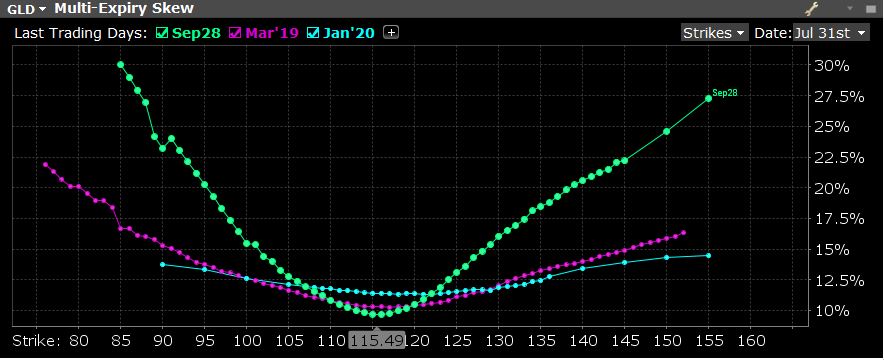

In options markets, return distributions with a negative skew such as that of the S&P 500 (coefficient of just over -1) result in a “smirking” or skewed volatility curve where far out of the money put options (options that mitigate risk of large sudden draw downs in price) are priced higher in terms of implied volatility than call options equidistant from the underlying price. As for options on GLD, you do not see a volatility curve that reflects the positive skewness of historical returns. In fact, the volatility profile of GLD options is unusually flat.

If a truly adverse scenario does play out in global markets, one would expect to see gold right tail options reprice to meet higher forward expectations of potential gold price movements in the positive direction. In that sense, owning long-dated OTM calls on GLD could serve as a decently cheap hedge (as opposed to S&P options, VIX futures, etc.) against the kinds of risk mentioned prior. January 2020 and March 2019 tail options are trading at an implied vol of about 15%, which is very attractive, considering gold’s historical average vol of circa 14%.

Gold has a lot to offer in times of stress, and in times of stress, you want to be hedged. It is my opinion that buying long-dated (Jan 2020), OTM calls on GLD are an effective and cheap hedge for any global and systematic tension in financial markets that we may face in the future. In the meanwhile, it would be silly not to expect gold to sink lower in the present strong-dollar dominated, Fed tightening environment.

So, it may be shrewd to be a little patient and wait for Gold to truly bottom out before you begin to accumulate a tidy position in these instruments. But I wouldn’t be too patient. Hedges are used to prepare you for the unexpected and so waiting patiently to hedge against an unforeseen event sort of defeats the purpose of hedging.

0 comments:

Publicar un comentario