China’s debt threat: time to rein in the spending boom

In the first piece of an FT series, Martin Wolf explains why the risks of a destructive slowdown are growing even within Beijing’s managed system

Martin Wolf in London

“If something can’t go on forever, it will stop.” This statement by Herbert Stein, chairman of the US council of economic advisers under Richard Nixon and Gerald Ford, tells us that debt cannot grow faster than an economy forever.

That is going to be true for China, too. What we do not know is when and how it will end. Will it be sooner or later? Will it be easy to cope with or will it be devastating? The manageability of China’s enormous domestic debts will be of great importance, not just for China, but for the many economies whose exports depend on it.

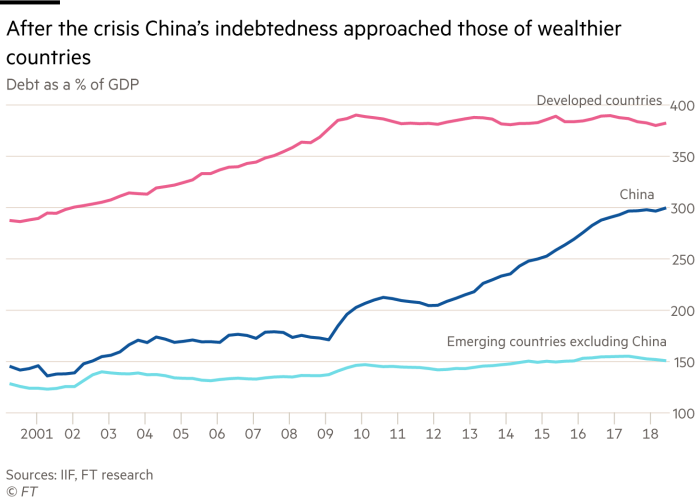

We cannot yet know how the debt surge will end. but we do know how it started. The trigger was the global financial crisis. Between early 2004 and late 2008, Chinese gross debt was stable at between 170 and 180 per cent of gross domestic product. This was higher than in other emerging countries, but not much higher. This seemed manageable.

Then, in 2008, came the meltdown of the western financial system and subsequent deep recession in high-income countries. China responded with a huge investment programme amounting to some 12.5 per cent of GDP, probably the biggest ever peacetime stimulus.

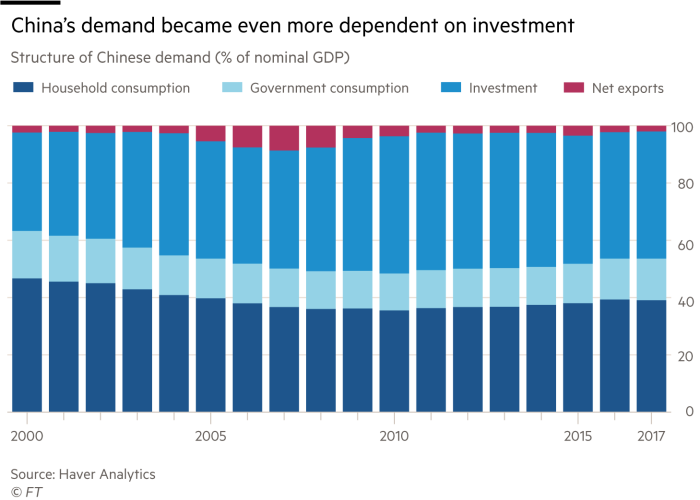

The challenge confronting Beijing was to offset the impact on demand of a fall in China’s net exports of 6 per cent of GDP between 2007 and 2011. In 2007, net exports had been close to 9 per cent of GDP. Since this was neither economically nor politically sustainable, the fall was permanent.

Such a decline in net external demand needed a permanent offset. Given the structure of the economy and the levers in the hands of the authorities, only investment could be increased quickly enough and on a large enough scale.

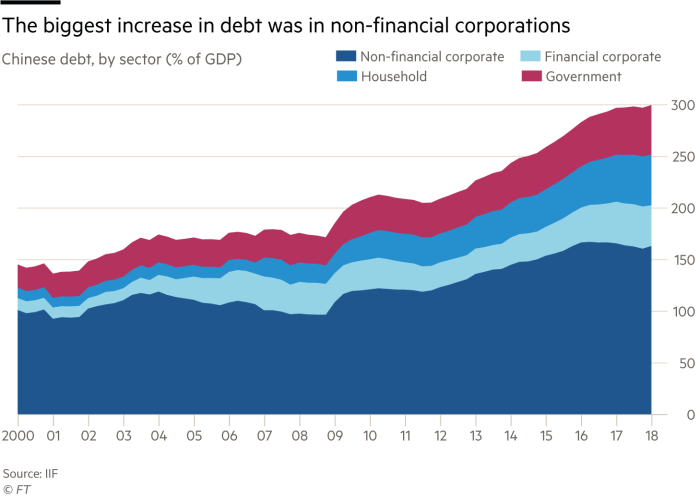

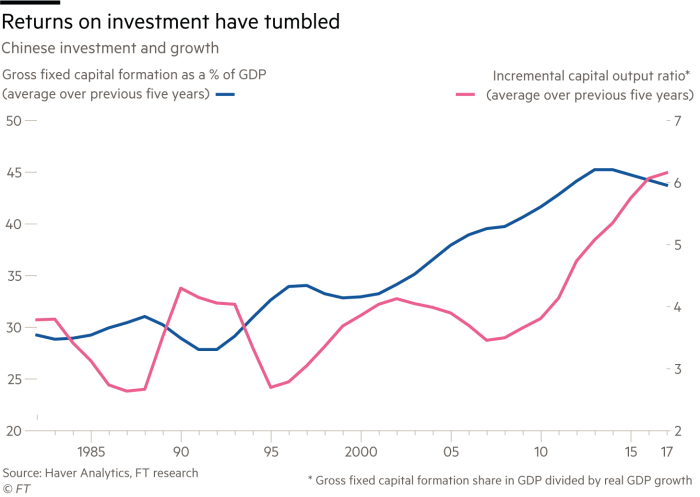

As a result the share of gross investment in GDP soared from an already extremely high 41 per cent of GDP in 2007 to 48 per cent in 2010. This huge investment boom maintained measured growth at close to 10 per cent after the crisis. It also led to a huge and sustained surge in debt, predominantly to non-financial corporations, including off-balance sheet local government financing vehicles. But ominously, far from raising China’s underlying rate of growth, a marked slowdown followed.

In the longer term, China’s raised investment rate has delivered the disturbing combination of more debt and slower growth.

According to the Institute for International Finance, between the fourth quarter of 2008 and the first quarter of 2018 China’s gross debt exploded from 171 to 299 per cent of GDP. A simple measure of the efficiency of the investment is the incremental capital output ratio, which measures the ratio of the investment rate to the growth rate. Until the crisis, the ICOR had not exceeded four for any sustained period. Ever since 2011, it has been close to six.

It was as though the high-income countries had passed the credit baton to China. For Beijing, this response to the financial crisis had an additional drawback — distracting it away from a necessary rebalancing of its economy.

In 2007, then premier Wen Jiabao declared that China’s growth was “unstable, unbalanced, uncoordinated and unsustainable”. In that year, net exports were 9 per cent of GDP, up from 2 per cent in 2000, investment was 41 per cent of GDP, up from 34 per cent in 2000, public and private consumption were a mere 50 per cent of GDP, down from 63 per cent in 2000, and gross debt was 174 per cent of GDP, up from 146 per cent in late 2000.

By 2017, net exports were back down to 2 per cent of GDP: that did represent a rebalancing. But investment was still higher than in 2007, at 44 per cent of GDP, private and public consumption was still only 54 per cent of GDP and debt had soared to three times GDP. In sum, the rebalancing of China’s external accounts came at the cost of still greater domestic imbalances.

So what happens now? There are four conceivable possibilities: a crisis, followed by lower growth; a crisis, not followed by lower growth; no crisis, but reduced growth; and no crisis and no reduction in growth.

In a paper published in 2010, Moritz Schularick of the Free University Berlin and Alan Taylor of the University of California Davis argued that “credit growth is a powerful predictor of financial crises”. This finding was from a database of 14 high-income countries. Yet a paper by Sally Chen and Joong Shik Kang of the IMF, published this year, argues that the evidence also applies to China, saying: “China’s credit boom is one of the largest and longest in history. Historical precedents of ‘safe’ credit booms of such magnitude and speed are few and far from comforting.”

This analysis suggests that a crisis of some kind is likely. The salient characteristics of a system liable to a crisis are high leverage, maturity mismatches, credit risk and opacity. China’s financial system has all these features. Among other things, China has a shadow banking sector, though a study by the Bank for International Settlements argues that “securitisation and market-based instruments still play only a limited role”. It is, in all, less complex and more directly connected to the banks than the US system was.

So why might the outcome in China be different than elsewhere?

One answer is that the high indebtedness is just a result of China’s extraordinarily high savings rates. But its national savings rates were already very high before the crisis, when the levels of indebtedness were not exploding.

Another proposition is that the rapid credit growth simply reflects normal expansion in the provision of financial services. But the IMF paper notes: “The leverage ratio in China is significantly higher than in countries with similar levels of development.”

It could also be argued that China is a creditor nation with a controlled capital account. That makes it relatively invulnerable to a run by foreign lenders of the kind familiar to observers of financial crises in emerging economies. Yet financial crises are possible in countries that are relatively immune to such runs: Japan in the 1990s is an example.

Another response is that China’s banking system has a lower ratio of credit to deposits than those of most countries that have experienced funding crises. But this ignores the system’s non-loan assets. In China the ratio of non-loan assets — assets other than conventional bank loans — to total assets was 50 per cent in 2016, a relatively high level. This is one indicator of the scale of China’s shadow banking system.

It is also asserted that the financial system’s assets are relatively sound. True, lending to non-financial corporate borrowers accounted for just over a half of the increase in debt between late 2008 and early 2018. But the quality of much of this lending is questionable. Moreover, “if debt is rising, but GDP is not, then the payment capacity is deteriorating”, the IMF paper argues.

The strongest reply is that the government is powerful and has a well-run central bank, effective control over the banking system, ownership of vast domestic and foreign assets, untapped fiscal capacity and tight controls over transactions with, and by, foreigners. If it were determined to protect the financial system from collapse it could do so. But if gross debt were to rise above 400 per cent of GDP over the next decade, even that would be less certain.

Imagine, however, that there is a financial crisis. Would it be followed by lower growth? The answer is: yes, in both the short and long term.

In the short term, a financial crisis would be followed by weaker investment. Given the decline in the trend rate of growth, the economically justified rate can hardly be higher than it was in 2000, when it was 34 per cent of GDP. That is 10 percentage points below the actual rate in 2017. If this adjustment were to come quickly, in the aftermath of a crisis, such a decline would generate an outright recession.

The extent and duration of such a recession would depend on how far and how quickly other spending would rise. China might be tempted to revert to a weaker exchange rate and a big increase in net exports. But the Trump administration would not tolerate this. The alternative would be much higher private and public consumption.

The constraints on the former are persistently high household savings rates and the low share of household disposable incomes (incomes after taxes and transfers) in GDP. The latter fell from 67 per cent of GDP in 1997 to 57 per cent in 2007. This has reversed a little, to an estimated 61 per cent in 2015, but estimates by the World Bank suggest it has fallen a little since then.

A surge in consumption sufficient to offset the impact on domestic demand of a big cut in investment spending would be impossible without a far bigger shift in incomes towards households. Moreover, that would squeeze profits, which would reduce investment still further. Ultimately, the only plausible offset to the impact of a big crisis in demand would be a huge increase in spending financed by central government.

A crisis then would probably mean a recession in the short term. In the longer term, growth would also slow from current reported levels. That would be largely because a significant part of the credit-fuelled investment spending had been wasted, partly in building unneeded dwellings and excessive industrial capacity.

Liu He is thought to be the unnamed senior official who called for a clampdown on debt © Bloomberg

What about a more palatable world with no crisis? This would represent a soft landing. The longer the authorities take to get control over debt trends the more difficult it will be to achieve such an outcome. But this is clearly the animating principle behind current policy, which is aimed at strengthening the financial system and halting the trend towards higher debt. Just how difficult it will be to stick to those principles is shown by this week’s announcement of another round of infrastructure spending, in order to stimulate demand. That implies more investment and debt. But the trade war with the US may make such backsliding inevitable.

How likely is success? The encouraging feature of the relatively recent past is that debt has stabilised, relative to GDP, since early 2017. Yet officially reported growth has held up. An obvious question then is whether the economic policy team, now under the leadership of vice-premier Liu He, has already found a way to sustain growth without increasing indebtedness.

The rapid economic expansion of China stuttered when the west was hit by the financial crisis © Reuters

It is reasonable to be sceptical. After all, China has only achieved this one period of stable debt ratios since 2008. Given its reliance on high investment, debt might need to rise rapidly again. Furthermore, the slowdown in credit growth could be an example of Goodhart’s law, named after Charles Goodhart of the London School of Economics. It states that “when a measure becomes a target, it ceases to be a good measure”. This has long been true of GDP in China. Might it now be true of reported debt?

The People’s Daily, the flagship newspaper of the Communist party, reported in May 2016 that an “authoritative figure” — widely believed to be Mr Liu — said “high leverage is the ‘original sin’ that leads to risks in the market for foreign exchange, stocks, bonds, real estate and bank credit”. Furthermore, “according to the authoritative figure, the country should make deleveraging a priority, and the ‘fantasy’ of stimulating the economy through monetary easing should be dropped. The country needs to be proactive in dealing with rising bad loans, rather than hiding them.”

China's traditionally high levels of household saving make it difficult to fuel consumption to the levels that may be needed © Bloomberg

The authoritative person was right. China has a choice between a whimper today and a destructive bang tomorrow. It can curb the debt surge and allow growth to slow now, or risk a crisis followed by a more severe slowdown later.

Making the needed changes will be difficult, particularly now, when a trade war has begun.

Yet, if President Xi Jinping’s apparently unlimited authority allows him to do anything, it has to be this. The time has come to halt China’s debt surge.

0 comments:

Publicar un comentario