Can factor investing kill off the hedge fund?

Data-driven funds that systematically exploit human weaknesses are disrupting traditional asset management

Robin Wigglesworth in New York

In 2001 Clifford Asness, a cerebral but fiery-tempered hedge fund manager with a penchant for comic book memorabilia, penned a paper arguing that his industry’s skills were “overstated”. Understandably, it went down like a lead balloon.

Mr Asness was inundated with irate calls from some of the industry’s biggest names, and even got the occasional glower at school events attended by other hedge fund fathers. “I got yelled at by a lot of famous people,” he recalls.

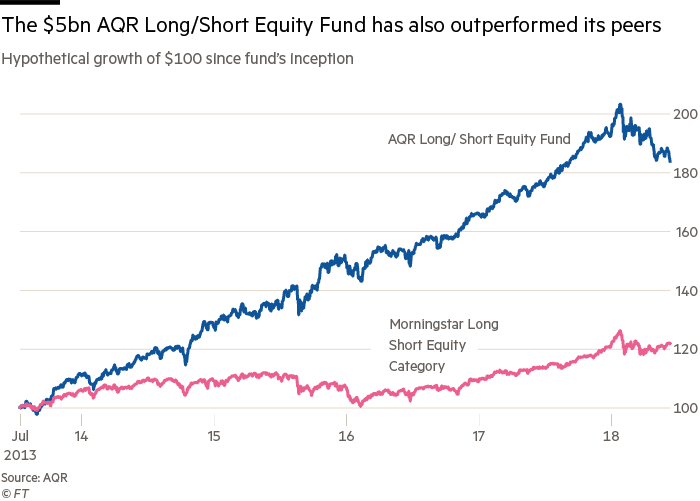

He survived the opprobrium. Mr Asness’s company AQR is today a major player in the hedge fund industry. Its $226bn of assets under management outstrip even Ray Dalio’s Bridgewater Associates. But rather than a hedge fund, AQR could now arguably be better described as a hedge fund killer.

AQR is at the vanguard of a revolution quietly sweeping through the asset management industry: “ Factor investing”, which in theory breaks down market returns into their basic components, researching what drives them and trying to systematically exploit their characteristics.

Factor investing is part of the broader world of computer-powered “quantitative” finance. But rather than scour markets and oceans of data for fleeting signals, factors are the big, persistent market drivers that in theory exploit timeless human foibles, such as our tendency to favour glamorous stocks over solid ones. Financial academics argue that a lot of what asset managers do is take advantage of these well-known patterns, anomalies and inefficiencies. But if one can do so systematically and cheaply, why pay for an expensive fund manager?

“Before, market drivers were like gods in the sky — mysterious and often unfathomable. But with factors we can now understand what actually drives performance,” says Marko Kolanovic, head of quantitative research at JPMorgan.

Think of factors as the basic ingredients of a solid meal. By deconstructing and finding the healthiest components, fans say they can be reassembled into a better-balanced, tastier diet. In other words, a more diversified, robust and cheaper investment portfolio than one built with traditional, blunt asset classes like stocks and bonds.

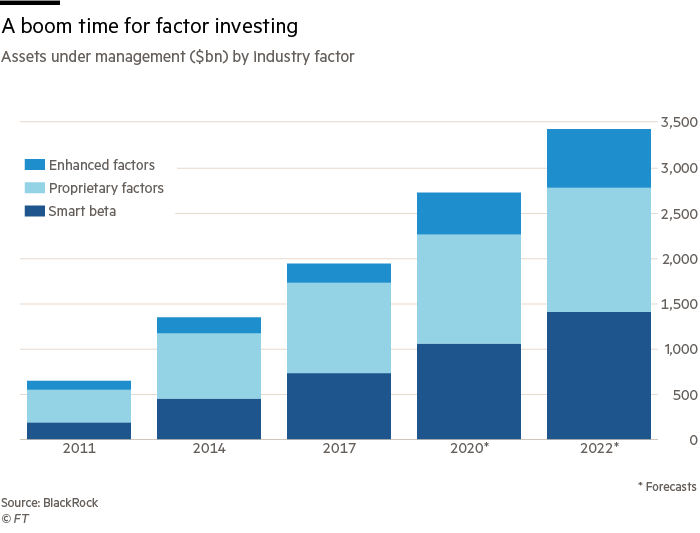

Recent results have been mixed, with many factor-focused funds — including AQR’s — suffering a mediocre or dismal 2018. But many pension funds, endowments and even retail investors are still embracing this new approach. BlackRock estimates that there are $1.9tn of assets in dedicated factor strategies, and predicts this will swell to $3.4tn by 2022.

Some have even gone so far as to call AQR the “Vanguard of hedge funds”, a reference to the passive investing group founded by Jack Bogle that has helped popularise cheap, index-tracking funds for the masses and unsettled the mutual fund industry in the process.

That may be a step too far to describe an investment group that still boasts plenty of expensive hedge fund strategies, some of which have also struggled in 2018. But it is “what we want to be. It’s aspirational,” Mr Asness admits. It is a description tacitly endorsed by Mr Bogle himself, who has said that among hedge funds AQR “is the one I hate the least”.

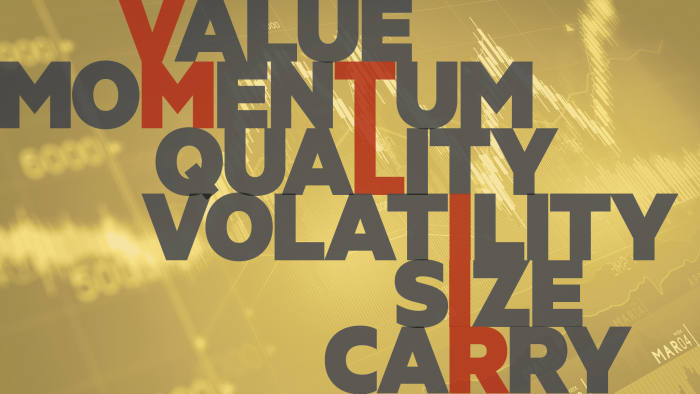

Defining factors

Value

Is the oldest and best-known factor, tracing its genesis to seminal work by Graham and Dodd in the 1930s and its popularity with Warren Buffett. It refers to the tendency for relatively cheap securities to outperform relatively expensive ones, as many investors wrongly prefer the glamour of racier “growth” stocks.

Momentum

Gets its mojo from the fact that assets with a positive trend tend to continue to do well, and those that are falling continue to slide. Most academics say the phenomenon is rooted in human psychology and how we initially underreact to news but overreact in the long run, or often sell winners too quickly and hang on to duds for far longer than is advisable.

Quality

Is powered by the fact that lower-risk, safer companies tend to do better than riskier, more indebted ones. The factor is often attributed to how investors systematically overpay for shakier stocks with seemingly better prospects, but underappreciate companies with boring but defensive business models.

Volatility

Is based on the observation that stolid stocks with typically muted movement actually tend to outperform more volatile ones over time, contrary to the view that investors should be compensated for the additional risk of buying more turbulent shares. The volatility factor indicates that investors can do better — and suffer less jarring movements — by buying steadier stocks.

Size

Captures the tendency of smaller stocks to do better than bigger ones in the longer run, possibly because they are less glamorous or risky. Since 1979 the Russell 200 index of “small-caps” has outperformed its big brother benchmark by almost 1 percentage point on average a year.

Carry

Is mostly specific to the bond market — albeit related to value — and refers to the tendency for higher-yielding assets to provide better returns than lower-yielding ones. In the equity world it reflects how companies with higher dividend yields tend to outperform their peers.

In 1992 Eugene Fama and Kenneth French, two professors at the University of Chicago Booth School of Business, published a paper that showed how investors could beat the stock market’s returns — the “beta” in finance jargon — by taking advantage of two simple factors: the tendency of small or cheap companies to outperform over time.

Factors are often called risk premia because they represent the extra compensation investors receive for taking on some specific risk. Many factors have been known for decades. Some pioneering “quant” investors influenced by academic research started to exploit factors in the 1970s. But the Fama-French paper was a bombshell, largely because Prof Fama is the father of the “efficient markets hypothesis”, which argues that investors cannot consistently beat the market.

“The king of EMH said that there were factors that had positive outperformance,” says Rob Arnott, head of Research Affiliates, a factor-focused investment group. “It blew people away.”

In 1989, Prof Fama took on a precocious PhD student as an assistant. Under his tutelage, Mr Asness wrote his thesis on a new factor, momentum, on how stocks that have gone up tend to continue to rise, and falling stocks tend to keep sliding. Given how it went against Prof Fama’s thesis it was “nerve-racking” telling him the dissertation, recalls Mr Asness. But Prof Fama says he was more upset that his protégé later chose the grubby world of investing over academia.

It worked out fine for Mr Asness. AQR is a privately held company, but according to filings by Affiliated Managers Group, which owns a minority stake, its revenues jumped 39 per cent to $1.3bn last year, and its net income rose over 50 per cent to $807m. For comparison, Man Group — the world’s biggest publicly listed hedge fund group — notched up revenues of $1bn and profits of $384m in 2017.

Jack Bogle (right), the Vanguard founder, called AQR, founded by Clifford Asness (left), the hedge fund 'I hate least' © Bloomberg

This has made its co-founders billionaires. Mr Asness is worth $3.6bn, and David Kabiller and John Liew both have an estimated $1.25bn, according to Forbes. A fourth co-founder, Robert Krail, retired for health reasons some years ago. Mr Liew and Mr Krail co-authored the 2001 paper with Mr Asness.

The rest of AQR’s quantitative analysts are not doing badly either. AQR spent $366.9m on compensation, benefits and other related staffing expenses last year, or more than $400,000 on average for its 914 employees (which includes 73 PhDs).

There are generally thought to be a “big five” in factors — size, value, momentum, volatility and quality. But over the years, academics have discovered scores more across different asset classes. While some of the research is well established, it is mainly in the past decade that interest has exploded.

Of the $1.9tn in factor strategies, BlackRock divides the industry into “proprietary factors” that typically reside in mutual fund structures ($1tn), “enhanced factors” in hedge fund vehicles ($209bn) and $729bn of “ smart beta” exchange traded funds, cheaper vehicles that tilt towards one or several investment factors.

Andrew Ang, head of factor investing at BlackRock, argues that the falling cost has been the primary catalyst. “Cars were invented in the late 1800s, but it wasn’t until Ford’s Model T that they took off. And it was because of cost,” he says. To describe the impact, he uses another metaphor: “Asset classes are like watching TV in black and white, while factors is like viewing it in colour.”

By in theory replicating what a lot of professional money managers do at a fraction of the cost, factor investing puts more pressure on fees. This is why Mr Asness thinks AQR can play the same disruptive role for hedge funds that Vanguard did for mutual funds.

“It is part of our business to be the Vanguard of hedge funds. It’s not all of our business, by any means. But to take some of the basics and say you should get this for lower fees,” he says.

“What [hedge funds] are doing as a group is good, but simple. And they’re kicking up a whole lot of dust around it.”

Eugene Fama accepting his Nobel Prize for economics in 2013 © AFP

Probably the first institutional investor to embrace factor investing was PKA, a $39bn Danish pension fund. In 2011 it started shifting its entire portfolio towards a more focused stream of risk premia, shrinking the number of asset managers it employs from 25 to just five. One of the managers it has kept working with is AQR, and Nils Ladefoged, the PKA executive who led the restructuring, is full of praise for the firm.

“They look at an asset and decompose it into various factors and think of the best way to harness them,” he says. “They are academic, but also conscious of the practical issues.”

PKA might have been one of the first investors to shift towards factors, but it was not the last. A State Street investor survey found that two-thirds now use factors to at least analyse their portfolios, and a third said it was their most important method. Indeed, factors are now an integral part of the industry.

Nonetheless, factor investing has plenty of detractors — even from its proponents. “It is aggressively oversold right now,” says Mr Arnott, another pioneer of the industry. “It shouldn’t be seen as a panacea. Factors can become materially expensive, and performance will mean-revert. Some factors have been performing better precisely because they’ve been getting inflows.”

Work done by Vincent Deluard, a strategist at INTL FCStone, illustrates this pitfall. In November 2016 he built a portfolio of S&P 500 stocks that failed to qualify for any of the five big US factor ETFs. But this “basket of deplorables” has since outperformed a basket of smart beta ETFs.

This is probably because many smart beta ETFs appear to be negatively correlated to interest rates, possibly because the data that academics crunch in their hunt for factors mostly only stretches back three decades — a period characterised by a secular decline in rates. Interest rates are now nudging higher, and this could be an Achilles heel for some factors.

“Investment managers will sell anything that can sell. Some of it is fine, but some of it is flimsy,” says Prof Fama. And even the ones that are robust will not always work. “A lot of people don’t know what they’re buying, but they’re buying a risk,” he adds. “If they’re willing to do so they will get a higher return over time. But there are long periods where by chance they just don’t turn up.”

That seems to be the case now, with many of the biggest factors simultaneously suffering a stinker in 2018 — hurting many big quant funds, including those managed by AQR. For example, its $4.8bn Style Premia Alternative Fund and $9.1bn Managed Futures Strategy Fund are down 7.4 per cent and 4.8 per cent this year. But the investment group is undeterred.

Mr Liew first met his future AQR co-founder at the University of Chicago, when another student pointed out Prof Fama’s assistant and whispered: “That guy [Asness] is ridiculously smart. He’s probably smarter than the professor. But the thing is, he knows it. He can be really insufferable at times.”

Mr Asness insists that his mentor is clearly the smarter one, but cheerfully admits that he does not always succeed in hiding his insufferableness. He also has a legendary temper, renowned smashing a series of computer monitors during a rough patch in the financial crisis. He said later that the reports were exaggerated: “It happened only three times, and on each occasion the computer screen deserved it.”

But Mr Asness uses his emotional reaction as an example of why factors endure in the long run. Many of the anomalies that factor investing exploit are deeply rooted in human psychology, which is why they are not weeded out over time. And as long as even quants can fall prey to these foibles, then factors will have a bright future, he argues.

“It’s a high pressure world. And when your factor is not working, it’s not an easy time,” he says. “But if we can’t keep emotion out of our own brains, it’s pretty good news for the factors, for the idea that investors aren’t perfectly rational is the reason these factors work. No matter what the times bring, we will stick to what we believe in and keep doing it.”

0 comments:

Publicar un comentario