When $1 Trillion Isn't $1 Trillion And A Warning From The Largest Asset Manager On Earth

by: The Heisenberg

- On Monday, BlackRock reported quarterly results and they served as a nice opportunity to pen a followup to one of my weekend posts.

- Outflows from the firm's equity products in Q2 underscore investor consternation with trade frictions.

- Meanwhile, one bank takes a closer look at a flashy buyback headline.

I spent a lot of time over the weekend talking about trade and buybacks and how the former is serving as a persistent source of angst and consternation for investors while the latter is arguably the most important source of support for U.S. stocks (SPY).

On the buyback front, the debate continues to rage about the social utility of corporations using their tax windfall to reward shareholders and inflate bottom lines, as the so-called "tyranny of quarterly capitalism" incentivizes management to prioritize shareholder returns.

That's clearly a contentious issue. As noted on Sunday, a Democratic sweep in November will almost surely mean more pressure on companies to spend on wage growth and capex. While most readers are probably well apprised of my political leanings, I'm not entirely sure it's within politicians' purview to try and dictate how private enterprise spends its free cash. The job of Congress is to legislate and there are ways of achieving the same end (i.e., incentivizing corporations to rethink how they allocate their cash) through legislation that don't involve politicians resorting to the kind of explicit, public exhortations of buybacks, which leave a bitter taste in the mouths of folks who might lean liberal on social issues, but would rather leave decisions about buybacks to the management teams with whom investors have entrusted their capital.

Anyway, that's my take on that and there's something for everyone (i.e., for both sides of the aisle) there.

Speaking of buybacks and people who are actively trying to push companies in the direction of eschewing myopia in favor of a long-term vision, you might recall that back in January, BlackRock's Larry Fink used his annual letter to effectively chide management teams on this issue. To wit, from that letter:

Companies have begun to devote greater attention to issues of long-term sustainability, but despite increased rhetorical commitment they have continued to engage in buybacks at a furious pace. While we certainly support returning excess capital to shareholders, we believe companies must balance those practices with investment in future growth.

To prosper over time, every company must not only deliver financial performance, but also show how it makes a positive contribution to society. Companies must benefit all of their stakeholders, including shareholders, employees, customers, and the communities in which they operate.

That was not well received in some circles, for obvious reasons, not the least of which is that it came across as something of a threat given how large BlackRock (BLK) is.

In the course of discussing buybacks over the weekend, I cited a recent JPMorgan note in which the bank's Nikolaos Panigirtzoglou took an in-depth look at repatriation following the tax cuts on the way to explaining how buybacks likely helped prop up the market in Q2:

Based on the average divisor change of four US equity indices, a proxy for the share count, we estimate that the net equity withdrawal by US companies overall including both financial and non-financial companies tripled in Q2 ($150bn) vs. Q1 ($50bn).

As it happens, Panigirtzoglou revisits this in his latest note (dated Friday) and in light of my weekend post, I wanted to highlight a couple of excerpts for readers here. JPMorgan makes a critical distinction between "values" and "volumes". To wit:

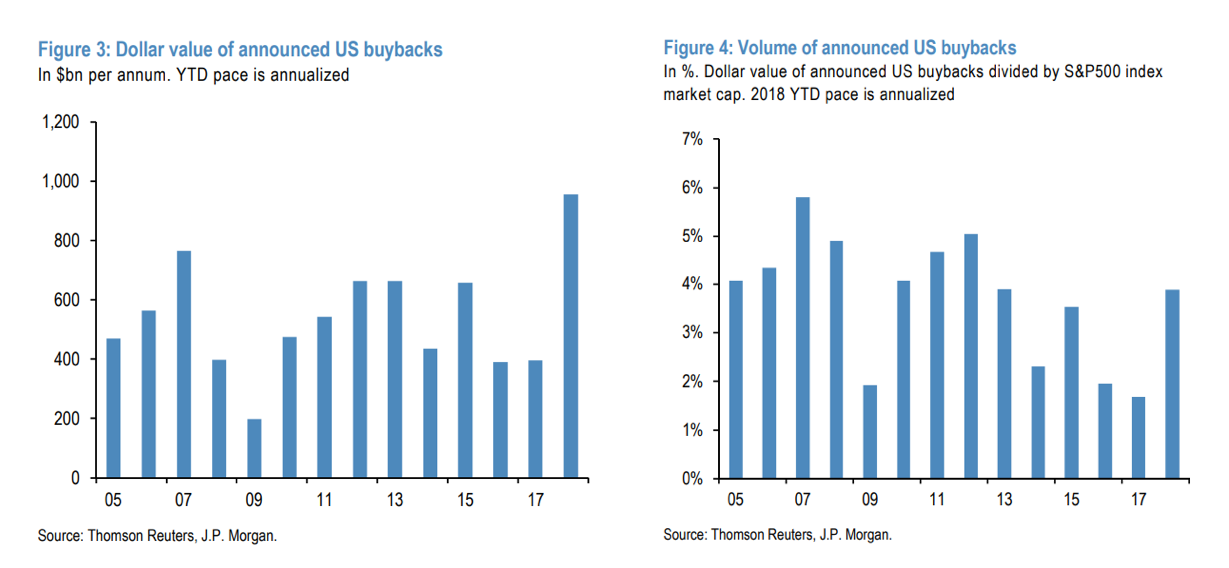

Announced US buybacks look set to approach one trillion dollars this year if one annualizes the YTD pace, the highest on record. But in volume terms, at 4% of the capitalization of the S&P 500 index, this year’s announced US buyback pace is lower than the 6% record high pace seen in 2007 and lower than the 5% post Lehman peak seen in 2012.

Panigirtzoglou goes on to again emphasize the distinction between "net actual buybacks" and the headlines numbers, where the former is estimated using share count reduction (i.e., taking into account shares issued as part of employee compensation packages). Here are the annualized numbers on that, both in dollar terms (left pane) and in volume terms (right pane):

Panigirtzoglou explains those visuals as follows:

If one looks at net actual US buybacks, this year’s annualized pace stands at just above $300bn which is lower that either 2015 or 2016 (Figure 5). In volume terms, the YTD pace of the share count reduction across major US equity indices is almost half of its 2015 high (Figure 6).

The implication there is that while the $1 trillion figure (the annualized dollar amount of announced buybacks using the YTD pace) is certainly a headline grabber, there's a ton of nuance under the surface. That nuance seems to suggest that the corporate bid, while voracious, might not be as strong a pillar of support for the market as the surface-level data would appear to tip.

I'm not sure that mitigates the type of criticism implicit in critiques of corporate cash usage (critiques like that delivered by Larry Fink earlier this year), but it does paint a more complete picture and is certainly more useful for investors looking to get an accurate read on how much support they can expect their equity portfolios to enjoy from the buyback bonanza.

You'll recall that the overarching point of the post linked here at the outset was to explore who the "marginal buyer of equities" would be in the event buybacks failed to support the market or if, for whatever reason (e.g., trade frictions dent global growth expectations), corporate earnings in the U.S. start to disappoint.

A big part of that discussion revolves around relatively subdued retail sentiment following the avalanche of inflows into equity funds that accompanied the January euphoria. Specifically, I cited another JPMorgan note by the same Nikolaos Panigirtzoglou, who last month observed a "sharp downshifting in equity and bond fund flows" since the first of the year.

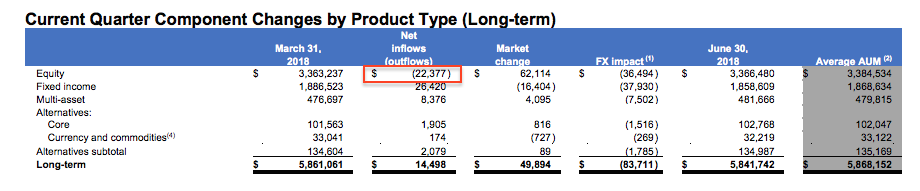

Well, BlackRock was out with its quarterly earnings on Monday and guess what? Inflows into iShares products were just $18 billion, the lowest since Q2 2016. More notable was the fact that investors look to have yanked more than $22 billion from the firm’s equity products during Q2:

(BlackRock)

(BlackRock)

In an interview with Bloomberg TV, the above-mentioned Larry Fink attributed this to consternation about trade and also to the fact that for the first time since 2008, "cash" is actually a viable option for some investors thanks to rising short rates in the U.S.

While I generally downplayed the "marginal buyer" question here over the weekend (citing the likelihood that buybacks and earnings growth would remain supportive in the U.S.), all of the above tells a bit of a different story or, at the very least, gives you some further perspective.

The buyback bid is optically huge, but the net effect might not live up to the billing. Meanwhile, BlackRock's results suggest that trade tensions are in fact weighing on sentiment.

You can take all of that for what it's worth, but I was delighted to take the opportunity to pen this short (by my standards) followup on Monday as BlackRock's earnings served as a poignant reminder that to the extent the "marginal buyer of equities" question does matter, the largest asset manager on the planet just saw $22 billion in net outflows from its equity funds in the space of three months.

0 comments:

Publicar un comentario