The United States Is Even More Broke Than We Think

by: Ronald Surz

- The 2018 "official" U.S. debt figure of $34 trillion is 120% of GDP and projected to double as a percent of GDP within the next 20 years. It's big.

- If we add "off-the-books" net obligations like Social Security and Medicare, our all-in debt, or so-called "fiscal gap", rises to $110 trillion, or 390% of GDP. It's scary.

- Raising taxes and reducing benefits won't restore solvency. Something is going to break, and it won't be pretty.

- If we add "off-the-books" net obligations like Social Security and Medicare, our all-in debt, or so-called "fiscal gap", rises to $110 trillion, or 390% of GDP. It's scary.

- Raising taxes and reducing benefits won't restore solvency. Something is going to break, and it won't be pretty.

We're broke and no one seems to care. We're all aware that this country owes a lot of money, but no one cares because we're leading pretty good lives here. We have yet to feel the consequences of being broke, but that won't last long. Some things are already breaking, and an ultimate breakdown is on the way. 2018 is the first year when tax receipts won't pay for Social Security and Medicare benefits. We are spending down the corpus, and will have spent all of the Social Security Trust by 2034, while Medicare monies will only last until 2026. This might sound like we have time, but we don't, especially since nothing is being done to head off these catastrophes. It's full speed ahead into the reckoning. Furthermore, some large pension funds are broke, and are likely to renege on their promised benefits. In the following, we share some details on this bankruptcy, and offer some actions that might help, although they are unlikely.

The National Debt

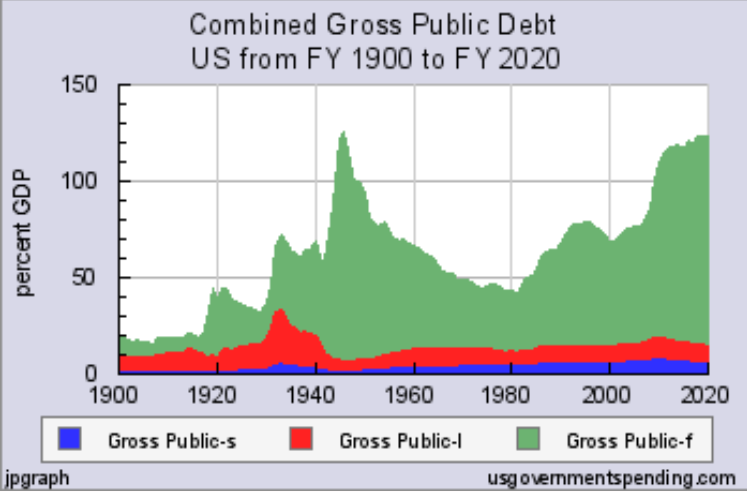

As shown in the following graph, the reported national debt of $34 trillion is currently 120% of GDP, a level only seen before in the wake of World War II. But unlike the last time, there are no signs that debt has peaked. We use a percentage of GDP to convey our ability to pay. If every dollar of output our country generates this year were used to pay our debt, it would not be enough. Of course we're not obligated to pay right away and therein lies our ho-hum attitude; we trust some miracle will solve the problem someday.

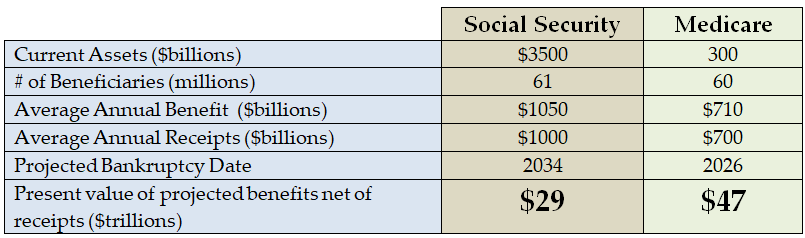

But that's not the whole story. We've made promises to older people that simply can't be kept unless the promises are changed (broken) and we burden today's young people with much higher taxes; the fixes are not pretty. As shown in the last row of the following table, the present value of the promise to pay Social Security benefits is $29 trillion more than projected receipts, and adding Medicare's $47 trillion promise brings our off-the-books liability to $76 trillion, more than twice the published liability. Our all-in national debt is an astronomical 390% of GDP.

What you should know about Social Security and Medicare

Source: Compiled by PPCA Inc. from various sources

What Can Congress Do?

Congress can address these problems by reducing spending or increasing taxes, or a combination of both, but the required magnitude is out of the question according to Professor Laurence Kotlikoff in his The US is dead broke and the tax bill does nothing to help matters, where he states:

Yes, Uncle Sam can avoid permanently raising all federal taxes by almost 60 percent.

But this means reneging on his spending promises. But even if he cuts all forms of spending (defense spending, entitlement spending, infrastructure spending, gassing up Air Force One, you name it), the needed permanent percentage cut is 47 percent!

A 60-percent permanent tax hike or a 47-percent permanent spending cut? These are our options the day after the ("magnificent" to some) tax bill was passed? How can things possibly be this bad?

Here's how: Successive Congresses and administrations have been systematically lying about our fiscal condition. They spent the past six decades accumulating massive liabilities that they kept off the books via clever use of language.

Congress has another choice that is equally ugly. It can print money, i.e. debase the currency.

This possibility has been the driving force behind the evolution of cryptocurrencies and other ways to replace the U.S. dollar standard. In other words, this country can renege on its promises at the expense of all savers holding dollars and dollar promises.

Time will tell what Congress decides, but in the meantime, we can prepare for what is likely to be very tough times.

What Can We Do?

Our best response is to not rely on Social Security and Medicare, and if we think debasing is a possibility, we should save in a "currency" other than the U.S. dollar. Saving more is part of the answer, and holding those savings in other forms of "money" is the rest. Those other forms include precious metals, real assets like real estate, and perhaps foreign and crypto currencies.

I say "perhaps" because foreign and cryptos can be volatile, and might not hold up in a U.S. hyperinflation.

I say "perhaps" because foreign and cryptos can be volatile, and might not hold up in a U.S. hyperinflation.

Those with defined benefit pension plans are more fortunate than those without because they have a presumed annual benefit from a viable company or union rather than the government.

But they too would suffer from debasing, plus some pension plans are broke, and the insurance behind them from the Pension Benefit Guarantee Corporation (PBGC) is on the brink of bankruptcy. When the PBGC was created in 1974, Jack Treynor, Pat Regan & Bill Priest wrote The Financial Reality of Pension Funding under ERISA, where they predicted the ultimate collapse of the PBGC because it was created to insure an uninsurable risk. It would appear that the day of collapse is at hand. As it stands now, healthy plans are paying most of the premiums and have to be thinking about terminating their plans because the premiums are not fair. The PBGC is going to break unless taxpayers pick up the slack, which is totally unfair.

But they too would suffer from debasing, plus some pension plans are broke, and the insurance behind them from the Pension Benefit Guarantee Corporation (PBGC) is on the brink of bankruptcy. When the PBGC was created in 1974, Jack Treynor, Pat Regan & Bill Priest wrote The Financial Reality of Pension Funding under ERISA, where they predicted the ultimate collapse of the PBGC because it was created to insure an uninsurable risk. It would appear that the day of collapse is at hand. As it stands now, healthy plans are paying most of the premiums and have to be thinking about terminating their plans because the premiums are not fair. The PBGC is going to break unless taxpayers pick up the slack, which is totally unfair.

Conclusión

We are broke and have decided to ignore it. The implied hope is that the repercussions will be in someone else's lifetime and that they won't be too painful. This is simply wishful thinking.

0 comments:

Publicar un comentario