The Italian challenge to the eurozone

In addition to feeble productivity growth, Italy has a large competitiveness handicap

Martin Wolf

The euro has been a failure. This does not mean it will not endure or that it would be better if it disappeared. The costs of a partial or complete break up are far too great. It means that the single currency has failed to deliver economic stability or a greater sense of a European identity. It has become a source of discord.

The story of Italy is revealing and, given its size, of crucial importance. This is not to blame the euro for the stagnation of Italian productivity and output since it joined the eurozone. These reflect domestic failings. Nevertheless, the fact that Italy is inside the eurozone makes its failings a matter of shared concern. It also destroys the link between politics and power. Not least, it turns what would otherwise have been brief exchange rate crises into long-running macroeconomic disasters.

All of this was predicted. In his excellent EuroTragedy, Princeton University’s Ashoka Mody cites a critique of the 1970 Werner Committee report, the first blueprint for a monetary union, by Nicholas Kaldor, a British economist of Hungarian origin. Kaldor argued there would need to be fiscal transfers. That would require a political union. But the conflicts created by the currency union would fester, making moves towards such a union more difficult. So it has proved: Andreas Kluth wrote in Handelsblatt Global this month: “A common currency was supposed to unite Europeans. Instead, it increasingly divides them.” He is right.

The decision to accept Italy as a founding member of the eurozone was made by former German chancellor Helmut Kohl, over the objections of his own officials and other governments. Prof Mody notes that Italy promised to bring its public debt ratio down from 120 per cent to 60 per cent by 2009. Instead it stabilised, before jumping to 130 per cent, after the eurozone crisis.

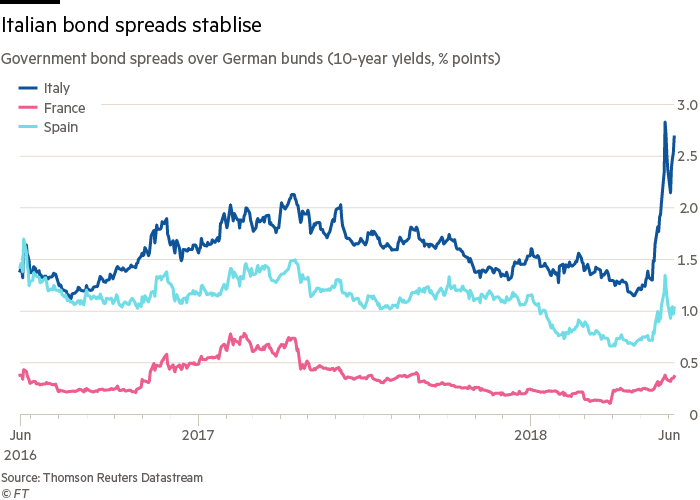

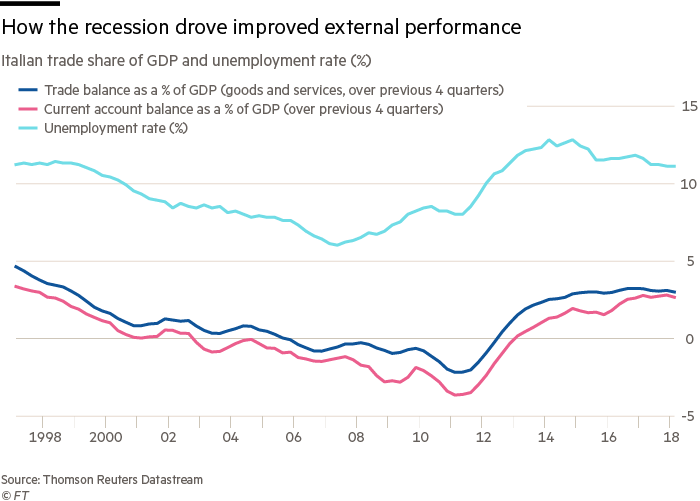

Not surprisingly, with this year’s real gross domestic product per head forecast by the IMF to be 8 per cent below its 2007 level and only 4 per cent above where it was in 1997, Italy elected populist parties to power. A combination of establishment and markets promptly neutralised their programme. Spreads vis a vis German Bunds have accordingly stabilised. (See charts.)

This might be a workable solution if a sustained return to prosperity were likely.

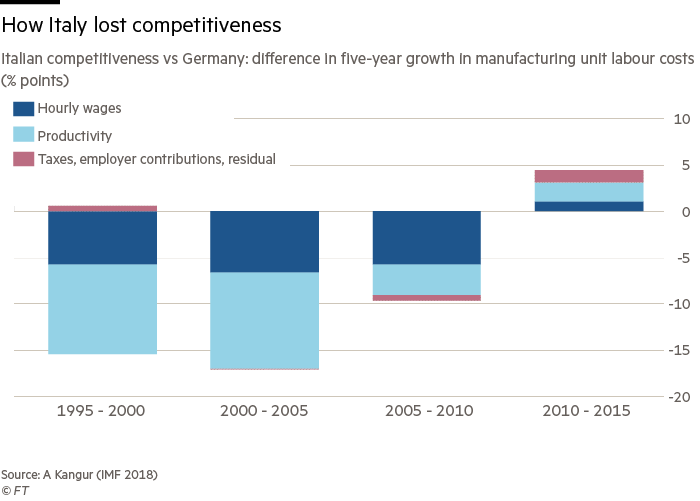

Unfortunately, in addition to feeble productivity growth, Italy suffers from a large competitiveness handicap, as shown by a recent IMF paper. This argues that Italy suffered a loss of competitiveness against Germany in excess of 40 per cent between 1995 and 2010.

The two initial problems for Italy, then, were the high level of public debt, which exposed it to financial market panic, and a huge prior loss of external competitiveness. Italy’s external balances are currently in surplus, largely because unemployment is so high. A strong expansion of internal demand is likely to generate unfinanceable external deficits. Northern European taxpayers fear they might have to pay for these. They will surely not do so.

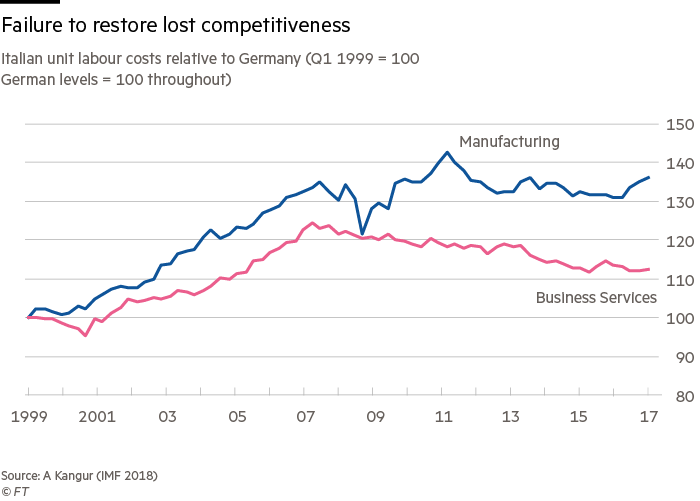

According to the IMF, “a real depreciation on the order of 10 per cent is estimated to be needed to realign Italy’s current account with fundamentals”. The recommended solution is an “internal devaluation”, via falling nominal wages and higher productivity. But Italy has not had much of either. Employment and investment have been slashed instead, with dire consequences. The fact that inflation has been so low in the eurozone as a whole has made the adjustments more difficult. Asymmetric adjustment is hard.

Outside the eurozone, the relevant adjustments would have occurred, as they did frequently before, through a currency depreciation. Yes, that would have been no long-run solution. But it would surely have been better than the social and political damage that has turned one of the most pro-EU countries into what is now one of the most sceptical. Nor is this over. The politics of Italy might not heal soon, or at all.

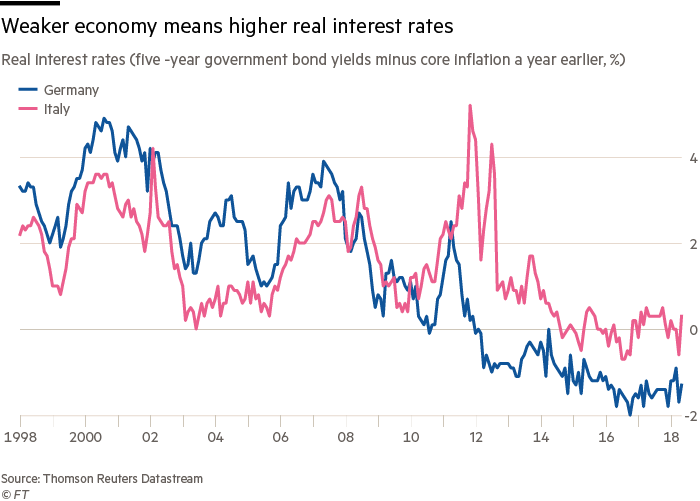

Part of the adjustment mechanism built into the currency union is the pro-cyclical impact of monetary policy: real interest rates are higher in countries forced through internal devaluations. The mechanism of adjustment in the eurozone is therefore essentially that of the 19th-century gold standard. Prolonged recessions are a feature, not a bug. They are how competitiveness adjusts to changing circumstances.

Neither a banking union, nor a capital market union, nor national fiscal flexibility can obviate these recessions, without persistent external support. Such mechanisms can only cushion economies against relatively transient changes, or shift losses abroad. Shifts in competitiveness require permanent changes in prices. These, in turn, follow recessions. The more rigid the economies and the bigger the adjustments, the more prolonged or deep the recessions. None of this is news. It was known by critics of the project before it began.

So what is to be done? A weak euro is a part of the answer. So is significantly higher inflation in surplus countries. But the European Central Bank is, for understandable reasons, unable, even under Mario Draghi, to pursue the hyper-aggressive monetary policies needed to generate real overheating in Germany or the Netherlands. Meanwhile, the latter see little reason to help.

Adjustment will always fall mainly on deficit countries. In the absence of sustained fiscal transfers, they have no alternative to reforms aimed at accelerating productivity growth and labour market flexibility. Spain has done that. Is it possible in Italy? If not, the bet on its entry into the eurozone could get worse.

Good fences make good neighbours. A currency of one’s own is a good fence. It is such a pity this was forgotten.

0 comments:

Publicar un comentario